Back

BackInventory and Cost of Goods Sold: Financial Accounting Study Guide

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Inventory and Cost of Goods Sold

Introduction

This chapter explores the accounting for inventory and cost of goods sold (COGS), a fundamental topic for merchandisers and manufacturers. Understanding inventory accounting is essential for accurate financial reporting, management decision-making, and compliance with U.S. GAAP and IFRS.

Accounting for Inventory

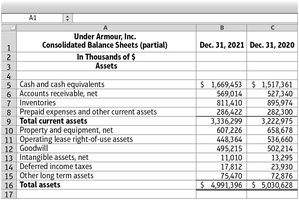

Inventory consists of goods purchased for resale, distinct from supplies or equipment used internally. Inventory is classified as an asset because it provides future economic benefit through eventual sale.

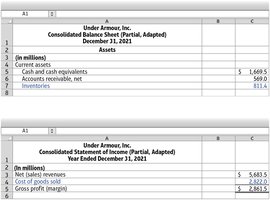

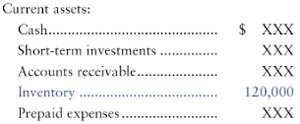

Inventory on the Balance Sheet: Represents the cost of goods still on hand.

Cost of Goods Sold (COGS) on the Income Statement: Represents the cost of inventory that has been sold.

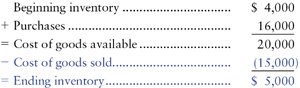

Inventory Equation:

Sales Price vs. Cost: Sales revenue is based on the sale price; COGS is based on the cost.

Gross Profit: The excess of sales revenue over COGS;

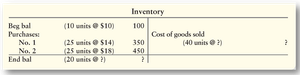

Determining Inventory Units

Inventory units are tracked through accounting records and verified by physical counts. Special considerations include consigned goods and goods in transit:

Consigned Goods: Inventory on consignment is included in the seller's records.

Goods in Transit: Ownership depends on shipping terms (FOB Shipping Point vs. FOB Destination).

Cost per Unit of Inventory

Inventory costs fluctuate throughout the year, raising questions about which costs are assigned to ending inventory and COGS.

Inventory Systems

Perpetual Inventory System: Maintains a real-time record of inventory; used for all types of goods.

Periodic Inventory System: Used for inexpensive goods; inventory is counted at least once a year.

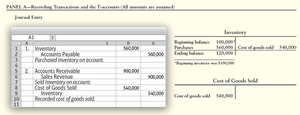

Recording Inventory Transactions

Purchases: Debit Inventory; Credit Cash or Accounts Payable.

Sales: Debit Cash/Accounts Receivable; Credit Sales Revenue. Also, Debit COGS; Credit Inventory.

Freight In: Transportation cost paid by buyer; part of inventory cost.

Freight Out: Selling cost; not part of inventory cost.

Purchase Returns/Allowances: Reduce inventory cost.

Purchase Discounts: Earned by paying quickly; reduce inventory cost.

Inventory Costing Methods

The method chosen affects profits, taxes, and financial ratios. Four main methods are used:

Specific Identification: Used for unique items; assigns actual cost to each unit.

Average-Cost (Weighted-Average): Assigns average cost to all units.

FIFO (First-In, First-Out): First costs in are first costs out; ending inventory reflects most recent costs.

LIFO (Last-In, First-Out): Last costs in are first costs out; ending inventory reflects oldest costs.

Income Effects of Inventory Methods

FIFO: When costs are rising, FIFO results in higher net income and higher taxes.

LIFO: When costs are rising, LIFO results in lower net income and lower taxes.

Average-Cost: Smooths out price fluctuations.

LIFO Liquidation: Occurs when inventory levels fall below previous periods, causing older costs to be included in COGS.

International Perspective: IFRS does not permit LIFO; U.S. GAAP does.

U.S. GAAP for Inventory

Disclosure: Financial statements must provide enough information for decision-making.

Representational Faithfulness: Inventory methods and material transactions must be properly disclosed.

Consistency: Use comparable methods from period to period.

Lower-of-Cost-or-Market (LCM) Rule

Inventory must be reported at the lower of its historical cost or market value (net realizable value). If market value drops below cost, inventory is written down.

U.S. GAAP: Write-downs cannot be reversed.

IFRS: Some write-downs can be reversed.

ESG and Inventory Valuation

Environmental, social, and governance (ESG) factors can affect inventory valuation by influencing demand and market value.

Gross Profit Percentage, Inventory Turnover, and Days Inventory Outstanding (DIO)

These ratios are key indicators of merchandising efficiency and profitability.

Gross Profit Percentage:

Inventory Turnover:

Days Inventory Outstanding (DIO):

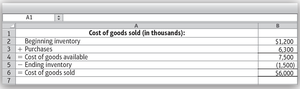

Cost-of-Goods-Sold Model for Management Decisions

Managers use the COGS model to determine inventory needs and estimate ending inventory, especially in periodic systems.

COGS Model:

Budgeted Purchases: Rearranged to solve for purchases needed.

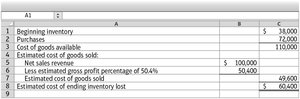

Gross Profit Method: Used to estimate ending inventory after events like fire or theft.

Analyzing Inventory Records Using Excel

Inventory records are often analyzed using Excel functions such as XLOOKUP to match identifiers (SKU, UPC, serial numbers) with transaction data for management and reporting purposes.

Summary Table: Inventory Costing Methods

Method | Application | Effect on COGS | Effect on Ending Inventory |

|---|---|---|---|

Specific Identification | Unique items | Actual cost per unit | Actual cost per unit |

Average-Cost | Homogeneous items | Average cost | Average cost |

FIFO | Any inventory | Oldest costs | Newest costs |

LIFO | Any inventory (U.S. only) | Newest costs | Oldest costs |

Key Formulas