Back

BackMeasuring Business Income: The Adjusting Process in Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Measuring Business Income: The Adjusting Process

Introduction to the Adjusting Process

The adjusting process is a critical step in the accounting cycle, ensuring that revenues and expenses are properly recognized in the correct accounting period. This process is essential for accurate financial reporting and compliance with generally accepted accounting principles (GAAP).

The Accounting Cycle Overview

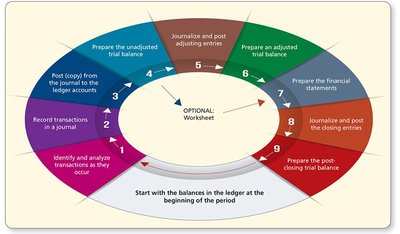

The accounting cycle is a series of steps followed during each accounting period to record and process financial transactions. The adjusting process is positioned after the initial recording and posting of transactions and before the preparation of financial statements.

Step 1: Identify and analyze transactions as they occur

Step 2: Record transactions in a journal

Step 3: Post from the journal to the ledger accounts

Step 4: Prepare the unadjusted trial balance

Step 5: Journalize and post adjusting entries

Step 6: Prepare an adjusted trial balance

Step 7: Prepare the financial statements

Step 8: Journalize and post the closing entries

Step 9: Prepare the post-closing trial balance

Fundamental Assumptions and Principles

Several key accounting principles guide the adjusting process:

Time Period Assumption: Financial information is reported at regular intervals (monthly, quarterly, annually).

Revenue Recognition Principle: Revenue is recognized when earned, not necessarily when cash is received.

Expense Recognition (Matching) Principle: Expenses are matched with the revenues they help generate in the same period.

Accrual Basis vs. Cash Basis Accounting

There are two main methods of accounting:

Accrual Basis: Records revenues when earned and expenses when incurred, regardless of cash flow.

Cash Basis: Records revenues and expenses only when cash is received or paid.

Accrual basis accounting provides a more accurate picture of a company's financial position and is required by GAAP.

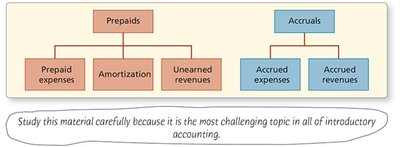

Types of Adjusting Entries

Adjusting entries are necessary to update account balances before preparing financial statements. They fall into two main categories:

Prepaids (Deferrals): Cash is paid or received before the related expense or revenue is recognized.

Accruals: Expenses or revenues are recognized before cash is paid or received.

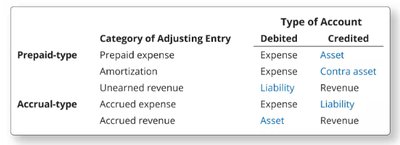

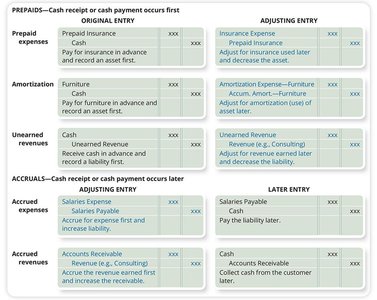

Summary Table: Categories of Adjusting Entries

Category | Debited | Credited |

|---|---|---|

Prepaid expense | Expense | Asset |

Amortization | Expense | Contra asset |

Unearned revenue | Liability | Revenue |

Accrued expense | Expense | Liability |

Accrued revenue | Asset | Revenue |

Prepaid Expenses

Prepaid expenses are payments made in advance for goods or services to be received in the future. These are initially recorded as assets and expensed over time as the benefits are consumed.

Examples: Prepaid rent, prepaid insurance, office supplies.

Journal Entry Example: On May 1, a company pays $3,600 for an annual insurance policy.

At month-end, an adjusting entry is made to recognize one month of insurance expense:

The remaining balance is still an asset, while the portion used is recognized as an expense.

Supplies and Supplies Expense

Supplies purchased are recorded as assets. At period-end, the amount used is transferred to supplies expense.

Example: $1,500 of supplies purchased; $1,000 remains at month-end, so $500 is expensed.

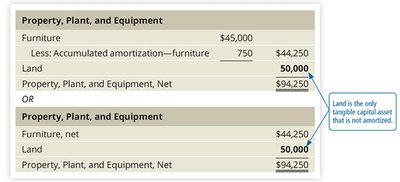

Amortization (Depreciation) of Long-Lived Assets

Amortization (or depreciation) allocates the cost of tangible and intangible assets over their useful lives, except for land, which is not amortized.

Example: Furniture purchased for $45,000 with a 5-year life. Monthly amortization is $750 ($45,000 / 5 years / 12 months).

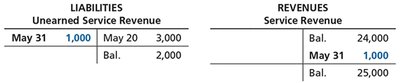

Unearned (Deferred) Revenues

Unearned revenues are payments received before services are performed or goods delivered. They are recorded as liabilities and recognized as revenue when earned.

Example: $3,000 received in advance for a 30-day project; $1,000 earned by month-end.

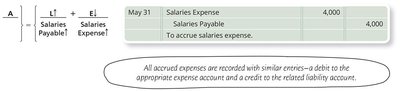

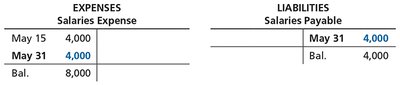

Accrued Expenses

Accrued expenses are costs incurred but not yet paid or recorded at period-end. They create a liability for the company.

Example: Salaries earned by employees but not yet paid at month-end.

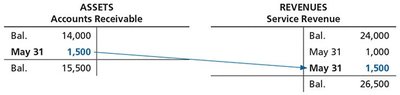

Accrued Revenues

Accrued revenues are revenues earned but not yet received or recorded at period-end. They are recognized by debiting a receivable and crediting a revenue account.

Example: Services provided but payment to be received in the next period.

Summary Table: Adjusting Entries

Category | Original Entry | Adjusting Entry | Later Entry |

|---|---|---|---|

Prepaid expenses | Prepaid Insurance / Cash | Insurance Expense / Prepaid Insurance | |

Amortization | Furniture / Cash | Amortization Expense / Accum. Amort.—Furniture | |

Unearned revenues | Cash / Unearned Revenue | Unearned Revenue / Service Revenue | |

Accrued expenses | Salaries Expense / Salaries Payable | Salaries Payable / Cash | |

Accrued revenues | Accounts Receivable / Service Revenue | Cash / Accounts Receivable |

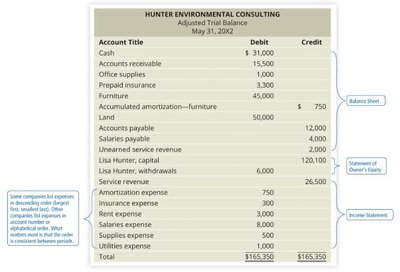

Adjusted Trial Balance

After all adjusting entries are posted, an adjusted trial balance is prepared to ensure total debits equal total credits. This forms the basis for preparing financial statements.

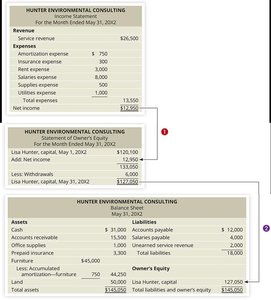

Preparation of Financial Statements

Financial statements are prepared in the following order:

Income Statement

Statement of Owner’s Equity

Balance Sheet

The net income from the income statement increases owner’s equity, which is then reported on the balance sheet.

Key Formulas

Straight-Line Amortization:

Expense Recognition (Matching):

Summary

The adjusting process ensures that all revenues and expenses are recognized in the correct period, in accordance with accrual accounting and GAAP.

Adjusting entries are essential for accurate financial statements and include prepaids, amortization, unearned revenues, accrued expenses, and accrued revenues.

The adjusted trial balance is the final step before preparing the financial statements, which are interrelated and provide a comprehensive view of the company’s financial position.