Back

BackPlant Assets, Natural Resources, and Intangibles: Financial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Plant Assets, Natural Resources, and Intangibles

Overview

This chapter covers the accounting treatment for long-term assets used in business operations, including property, plant, and equipment (PP&E), natural resources, and intangible assets. These assets are essential for generating future revenues and require specialized accounting methods to reflect their usage, value, and impact on financial statements.

Accounting for the Cost of Plant Assets

Plant assets are recorded at the total cost incurred to bring them to their intended use. This includes purchase price, taxes, commissions, and other necessary expenditures.

Land: Includes purchase price, brokerage commission, survey fees, legal fees, back property taxes, grading, clearing, and removal of unwanted buildings. Excludes fencing, paving, security systems, and lighting (these are land improvements).

Buildings: Construction costs include architectural fees, permits, contractor charges, materials, labor, overhead, and interest on borrowed funds. Purchase costs include price, commissions, taxes, and renovation expenses.

Equipment: Includes purchase price (net of discounts), transportation, insurance in transit, taxes, commissions, installation, testing, and special platforms.

Land Improvements: Driveways, signs, fences, sprinkler systems, and similar items. These are depreciated over their useful lives.

Leasehold Improvements: Improvements to leased property, depreciated or amortized over the lease term.

Lump-Sum (Basket) Purchases: When multiple assets are purchased together, costs are allocated based on relative market values using the relative-sales-value method.

Capital Expenditures vs. Immediate Expenses

Expenditures on plant assets are classified as either capital expenditures (added to asset accounts) or immediate expenses (recorded as expenses).

Capital Expenditures: Increase asset capacity or extend useful life; capitalized on the balance sheet.

Immediate Expenses: Do not increase capacity or useful life; expensed immediately (e.g., repairs and maintenance).

Small, immaterial costs are usually expensed. Errors can occur if costs are misclassified.

Leased Assets

Leasing allows businesses to use assets without large upfront payments. Most leases result in both a "right to use asset" and a liability for future payments on the balance sheet.

Depreciation of Plant Assets

Depreciation allocates the cost of plant assets to expense over their useful lives, reflecting wear, obsolescence, and loss of value. Land is not depreciated.

Book Value: Asset cost minus accumulated depreciation (a contra asset account).

Depreciable Cost: Asset cost minus estimated residual (salvage) value.

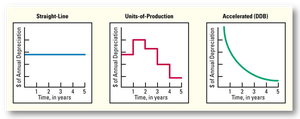

Depreciation Methods

Three main methods are used to calculate depreciation:

Straight-Line Method: Equal depreciation expense each period. Formula:

Units-of-Production Method: Depreciation based on asset usage. Formula:

Double-Declining-Balance Method: Accelerated depreciation; higher expense in early years. Formula:

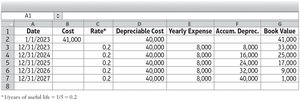

Straight-Line Depreciation Example

Date | Cost | Rate* | Depreciable Cost | Yearly Expense | Accum. Deprec. | Book Value |

|---|---|---|---|---|---|---|

1/1/2023 | 41,000 | 0.2 | 40,000 | 8,000 | 8,000 | 33,000 |

12/31/2024 | 41,000 | 0.2 | 40,000 | 8,000 | 16,000 | 25,000 |

12/31/2025 | 41,000 | 0.2 | 40,000 | 8,000 | 24,000 | 17,000 |

12/31/2026 | 41,000 | 0.2 | 40,000 | 8,000 | 32,000 | 9,000 |

12/31/2027 | 41,000 | 0.2 | 40,000 | 8,000 | 40,000 | 1,000 |

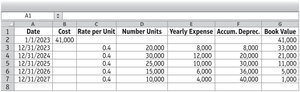

Units-of-Production Depreciation Example

Date | Cost | Rate per Unit | Number Units | Yearly Expense | Accum. Deprec. | Book Value |

|---|---|---|---|---|---|---|

1/1/2023 | 41,000 | 0.4 | 20,000 | 8,000 | 8,000 | 33,000 |

12/31/2024 | 41,000 | 0.4 | 30,000 | 12,000 | 20,000 | 21,000 |

12/31/2025 | 41,000 | 0.4 | 25,000 | 10,000 | 30,000 | 11,000 |

12/31/2026 | 41,000 | 0.4 | 15,000 | 6,000 | 36,000 | 5,000 |

12/31/2027 | 41,000 | 0.4 | 10,000 | 4,000 | 40,000 | 1,000 |

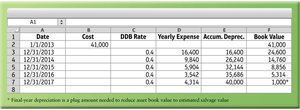

Double-Declining-Balance Depreciation Example

Date | Cost | DDB Rate | Yearly Expense | Accum. Deprec. | Book Value |

|---|---|---|---|---|---|

1/1/2013 | 41,000 | 0.4 | 16,400 | 16,400 | 24,600 |

12/31/2014 | 41,000 | 0.4 | 9,840 | 26,240 | 14,760 |

12/31/2015 | 41,000 | 0.4 | 5,904 | 32,144 | 8,856 |

12/31/2016 | 41,000 | 0.4 | 3,542 | 35,686 | 5,314 |

12/31/2017 | 41,000 | 0.4 | 4,314 | 40,000 | 1,000 |

Depreciation Patterns Comparison

Each method results in different annual expense patterns, but the total depreciable cost is the same.

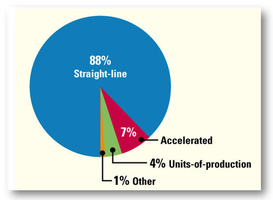

Depreciation Methods Usage

Most companies use the straight-line method for financial reporting.

Other Issues in Accounting for Plant Assets

Depreciation affects income taxes; accelerated methods provide faster tax deductions.

Fully depreciated assets can still be used but are not depreciated further.

Disposal of assets requires bringing depreciation up to date and recognizing gains or losses.

Accounting for Natural Resources

Natural resources (e.g., oil, timber) are depleted over time. Depletion is calculated similarly to units-of-production depreciation.

Depletion Rate:

As resources are extracted, they move from inventory to cost of goods sold.

Accounting for Intangible Assets

Intangible assets lack physical form but carry special rights (patents, copyrights, trademarks, franchises, goodwill).

Finite Lives: Amortized over useful life.

Indefinite Lives: Not amortized; tested annually for impairment.

Goodwill: Only recorded when purchased; not amortized, but tested for impairment.

R&D Costs: Expensed as incurred under U.S. GAAP.

Asset Impairment

Assets are tested annually for impairment. If expected future cash flows are less than the asset's net book value, the asset is impaired and its carrying value is reduced to fair value.

Rate of Return on Assets (ROA)

ROA measures how efficiently assets generate net income. Formula:

ESG Factors and Asset Accounting

Environmental, social, and governance (ESG) factors can affect the useful life and value of plant assets, natural resources, and intangibles. For example, stricter regulations or changing societal values may reduce asset values or useful lives.

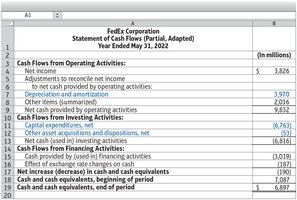

Cash Flow Impact of Long-Lived Asset Transactions

Long-lived asset transactions affect the statement of cash flows:

Acquisitions: Investing activities (cash outflow).

Sales: Investing activities (cash inflow).

Depreciation/Amortization: Operating activities (added back to net income).

Calculating Depreciation Using Excel Functions

Excel functions can automate depreciation calculations:

SLN: Calculates straight-line depreciation.

DDB: Calculates double-declining-balance depreciation.

Example: For an asset costing $75,000, with a residual value of $12,000 and a useful life of 5 years, use SLN and DDB functions to generate depreciation schedules.