Back

BackPlant Assets, Natural Resources, and Intangibles: Financial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Plant Assets, Natural Resources, and Intangibles

Overview

This chapter covers the accounting for plant assets, natural resources, and intangible assets, including their acquisition, depreciation, disposal, and the impact on financial statements. It also addresses related topics such as asset impairment, rate of return on assets, and the cash flow effects of long-lived asset transactions.

Accounting for the Cost of Plant Assets

Definition and Measurement

Plant assets are tangible long-lived assets used in the operations of a business. The cost of a plant asset is the sum of all costs incurred to bring the asset to its intended use.

Costs include: Purchase price, taxes, commissions, and other costs to make the asset ready for use.

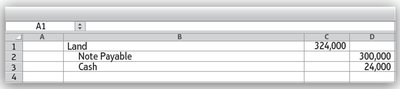

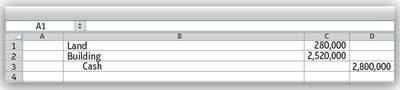

Land

Included in land cost: Purchase price, brokerage commission, survey fees, legal fees, back property taxes, grading and clearing, and removal of unwanted buildings.

Excluded from land cost: Fencing, paving, security systems, and lighting (these are land improvements and are depreciated separately).

Example: FedEx purchases land and incurs additional costs. The total cost is recorded as follows:

Buildings, Machinery, and Equipment

Constructing a building: Includes architectural fees, permits, contractor charges, materials, labor, overhead, and interest on borrowed funds.

Purchasing a building: Includes purchase price, brokerage commission, taxes, and renovation costs.

Equipment: Includes purchase price (less discounts), transportation, insurance in transit, taxes, commissions, installation, testing, and special platforms.

Land Improvements and Leasehold Improvements

Land improvements: Driveways, signs, fences, sprinkler systems, etc. (depreciated over useful life).

Leasehold improvements: Improvements to leased property, depreciated or amortized over the lease term.

Lump-Sum (Basket) Purchases

When multiple assets are purchased together, the total cost is allocated based on relative market values using the relative-sales-value method.

Capital Expenditures vs. Immediate Expenses

Definitions

Capital expenditures: Increase asset capacity or extend useful life; costs are capitalized (added to asset account).

Immediate expenses: Ordinary repairs and maintenance; expensed as incurred.

Example: Major engine overhaul is capitalized; oil change is expensed.

Leased Assets

Leased assets often appear on the balance sheet as both a right-to-use asset and a lease liability.

Details of lease accounting are covered in later chapters.

Depreciation of Plant Assets

Concept and Calculation

Depreciation is the allocation of a plant asset’s cost to expense over its useful life. Land is not depreciated.

Book Value: $\text{Book Value} = \text{Cost} - \text{Accumulated Depreciation}$

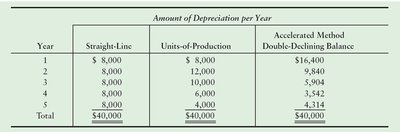

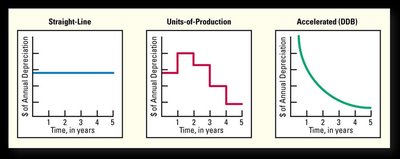

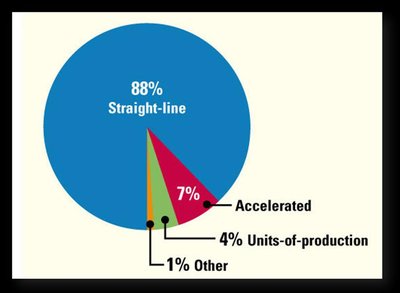

Depreciation Methods

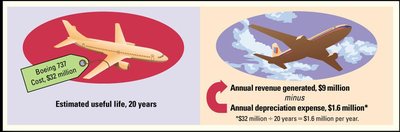

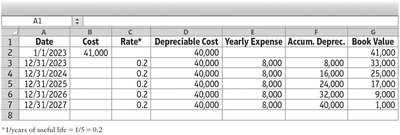

Straight-Line Method: Equal depreciation each year. $\text{Depreciation per year} = \frac{\text{Cost} - \text{Residual Value}}{\text{Useful Life (years)}}$

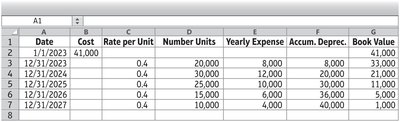

Units-of-Production Method: Depreciation based on usage. $\text{Depreciation per unit} = \frac{\text{Cost} - \text{Residual Value}}{\text{Total Estimated Units}}$

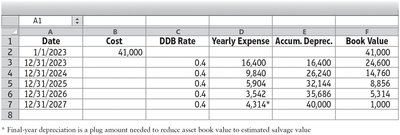

Double-Declining-Balance Method: Accelerated depreciation. $\text{DDB Rate} = 2 \times \frac{1}{\text{Useful Life (years)}}$

Examples and Schedules

Comparison of Methods

Other Depreciation Issues

Depreciation affects income taxes; accelerated methods provide faster tax deductions.

MACRS is used for tax purposes in the U.S.

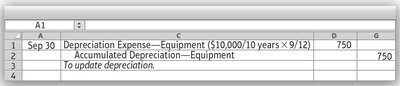

Partial-year depreciation is prorated based on the acquisition date.

Changes in useful life are treated as changes in accounting estimates.

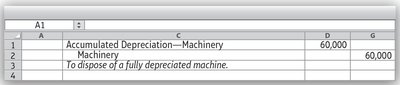

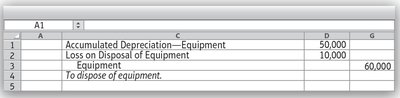

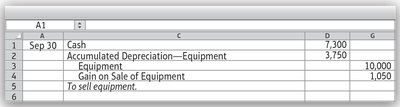

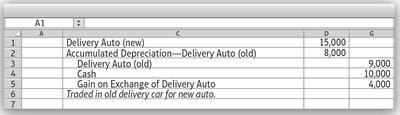

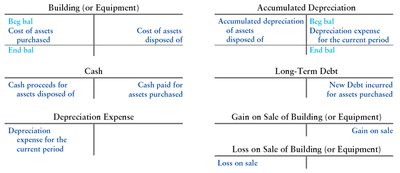

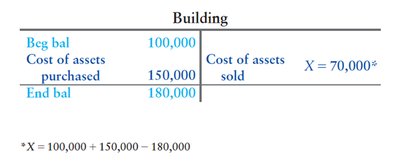

Disposal of Plant Assets

Process

Update depreciation to the date of disposal.

Remove asset and accumulated depreciation from the books.

Record any gain or loss on disposal.

T-Accounts for Analysis

GAAP vs. IFRS: Depreciation and Asset Reporting

U.S. GAAP uses historical cost and composite asset depreciation.

IFRS uses a component approach, depreciating each major part separately.

IFRS allows reversal of impairment losses in some cases; GAAP does not.

Natural Resources and Intangible Assets

Natural Resources

Examples: Oil, minerals, timber (wasting assets).

Depletion tracks the use of natural resources.

Intangible Assets

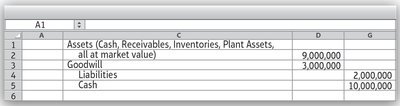

No physical form; carry special rights (patents, copyrights, trademarks, franchises, goodwill).

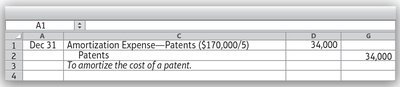

Finite life intangibles are amortized; indefinite life intangibles are tested for impairment.

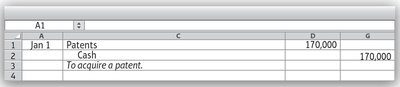

Patents

Goodwill

Goodwill is the excess paid over the fair value of net assets in a business acquisition.

Only recorded when purchased; tested for impairment, not amortized.

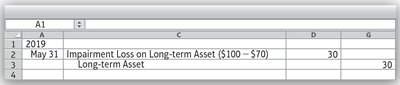

Asset Impairment

Definition and Process

Impairment occurs when expected future cash flows are less than the asset’s book value.

Impairment loss is recognized as: $\text{Impairment Loss} = \text{Net Book Value} - \text{Fair Value}$

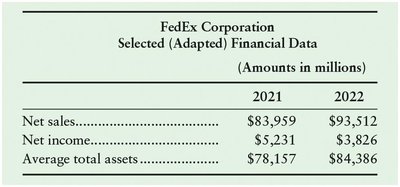

Rate of Return on Assets (ROA)

Calculation

ROA measures how efficiently assets generate net income.

$\text{ROA} = \frac{\text{Net Income}}{\text{Average Total Assets}}$

Average total assets = (Beginning total assets + Ending total assets) / 2

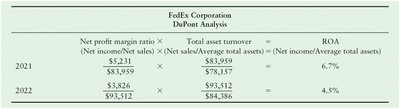

DuPont Analysis

Breaks ROA into net profit margin and total asset turnover:

$\text{ROA} = \text{Net Profit Margin Ratio} \times \text{Total Asset Turnover}$

Net Profit Margin Ratio = Net Income / Net Sales

Total Asset Turnover = Net Sales / Average Total Assets

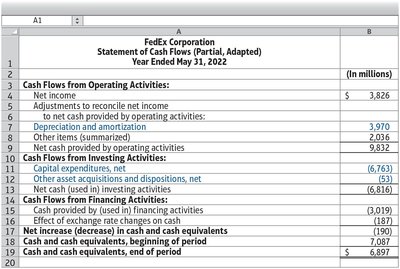

Cash Flow Impact of Long-Lived Asset Transactions

Statement of Cash Flows

Acquisitions and sales of long-lived assets are reported as investing activities.

Depreciation and amortization are added back to net income in operating activities (non-cash expenses).

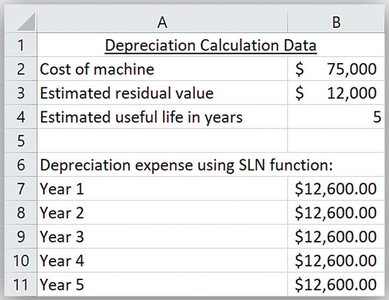

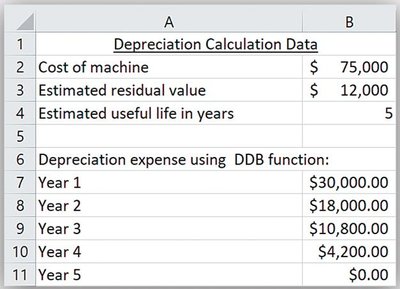

Depreciation Calculations Using Excel Functions

Excel Functions

SLN function: Calculates straight-line depreciation.

DDB function: Calculates double-declining-balance depreciation.