Back

BackPlant Assets, Natural Resources, and Intangibles: Financial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Plant Assets, Natural Resources, and Intangibles

Overview

This chapter covers the accounting for plant assets, natural resources, and intangible assets, including their acquisition, depreciation, disposal, and the impact on financial statements. It also addresses related topics such as asset impairment, rate of return on assets, and the cash flow effects of long-lived asset transactions.

Accounting for the Cost of Plant Assets

Definition and Measurement

Plant assets are tangible long-lived assets used in the operations of a business. The cost of a plant asset is the sum of all expenditures necessary to acquire the asset and prepare it for its intended use.

Cost includes: Purchase price, taxes, commissions, and other costs to make the asset ready for use.

Land

Included in cost: Purchase price, brokerage commission, survey fees, legal fees, back property taxes, grading and clearing, removal of unwanted buildings.

Excluded from cost: Fencing, paving, security systems, lighting (these are land improvements and are depreciated separately).

Buildings, Machinery, and Equipment

Constructed buildings: Architectural fees, permits, contractor charges, materials, labor, overhead, interest during construction.

Purchased buildings: Purchase price, commissions, taxes, repairs, and renovations.

Equipment: Purchase price (less discounts), transportation, insurance in transit, taxes, installation, testing, special platforms.

Land Improvements and Leasehold Improvements

Land improvements: Driveways, signs, fences, sprinkler systems, etc. (depreciated over useful life).

Leasehold improvements: Improvements to leased property, depreciated or amortized over the lease term.

Lump-Sum (Basket) Purchases

When multiple assets are purchased together for a single price, the total cost is allocated based on relative market values using the relative-sales-value method.

Capital Expenditures vs. Immediate Expenses

Definitions

Capital expenditures: Increase asset capacity or extend useful life; costs are capitalized (added to asset account).

Immediate expenses: Ordinary repairs and maintenance; expensed as incurred.

Extraordinary repairs and improvements are capitalized, while routine maintenance is expensed.

Leased Assets

Leased assets often appear on the balance sheet as both a right-to-use asset and a lease liability, depending on the lease type.

Depreciation of Plant Assets

Concepts and Calculation

Depreciation is the allocation of the cost of a plant asset to expense over its useful life. Land is not depreciated.

Book Value:

Depreciation is based on: Cost, estimated useful life, and estimated residual value.

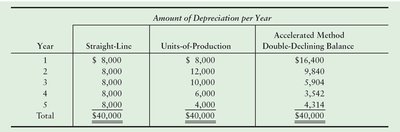

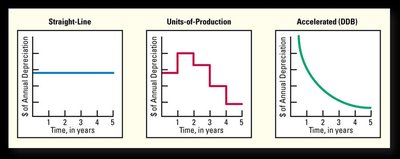

Depreciation Methods

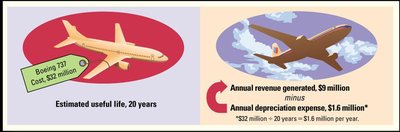

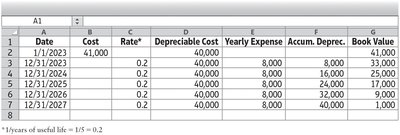

Straight-Line Method: Equal expense each year.

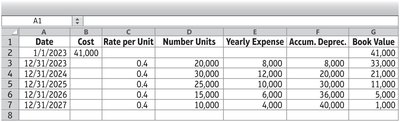

Units-of-Production Method: Expense based on usage.

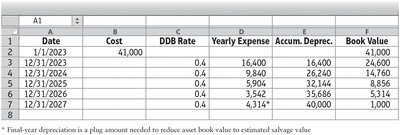

Double-Declining-Balance Method: Accelerated method, higher expense in early years.

Comparison of Methods

Straight-line is best for assets generating even revenue; units-of-production for assets that wear out with use; DDB for assets generating more revenue early in life.

Other Depreciation Issues

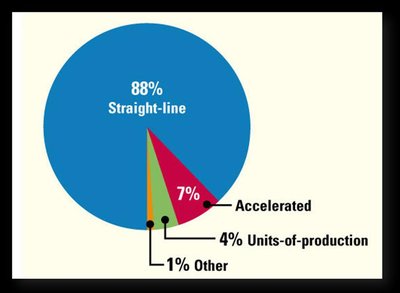

Tax purposes: Accelerated methods (e.g., MACRS) often used for tax benefits.

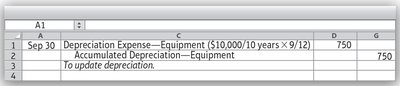

Partial-year depreciation: Prorate expense for assets acquired during the year.

Change in estimate: Adjust depreciation prospectively if useful life or residual value changes.

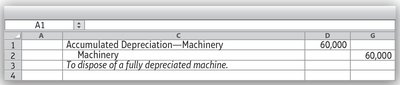

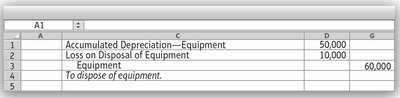

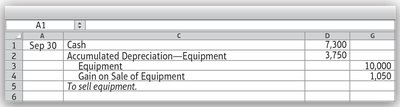

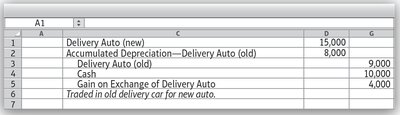

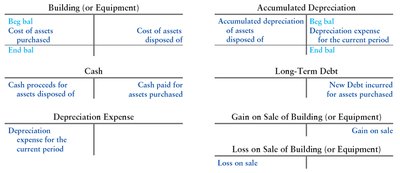

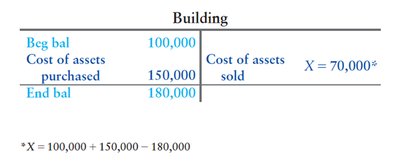

Disposal of Plant Assets

Process

Before disposal, update depreciation to the date of disposal. Remove asset and accumulated depreciation from the books. Record any gain or loss.

T-Accounts for Analysis

GAAP vs. IFRS: Depreciation

GAAP: Uses historical cost, depreciates composite assets.

IFRS: Uses component approach, depreciates each part separately, allows reversal of impairment losses in some cases.

Natural Resources and Intangible Assets

Natural Resources

Natural resources (e.g., oil, timber) are depleted over time. Depletion expense is calculated similarly to units-of-production depreciation.

Intangible Assets

Intangibles: Long-term assets with no physical form (patents, copyrights, trademarks, franchises, goodwill).

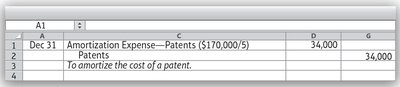

Finite life: Amortized over useful life.

Indefinite life: Not amortized; tested for impairment annually.

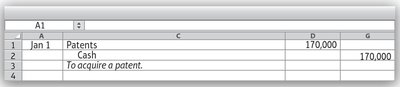

Patents

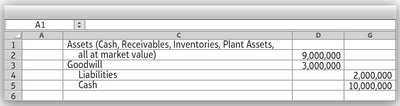

Goodwill

Goodwill is recorded only when a business is purchased for more than the fair value of its net assets.

Research and Development (R&D) Costs

U.S. GAAP: R&D costs are expensed as incurred.

IFRS: Research costs expensed; development costs capitalized if certain criteria are met.

Asset Impairment

Definition and Process

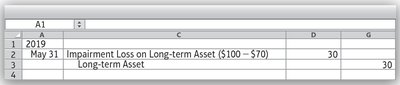

An asset is impaired if its expected future cash flows are less than its book value. The carrying value is written down to fair value, and an impairment loss is recognized.

Impairment loss:

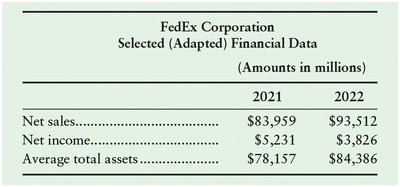

Rate of Return on Assets (ROA)

Calculation

ROA:

Average Total Assets:

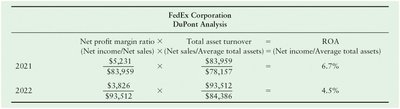

DuPont Analysis

ROA = Net Profit Margin Ratio × Total Asset Turnover

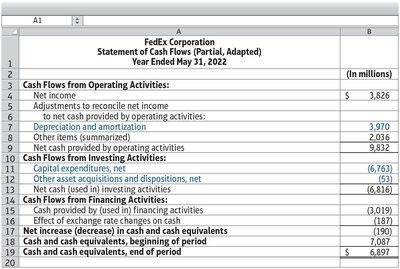

Cash Flow Impact of Long-Lived Asset Transactions

Statement of Cash Flows

Acquisitions: Investing activities (cash outflow)

Sales: Investing activities (cash inflow)

Depreciation/Amortization: Operating activities (added back to net income)

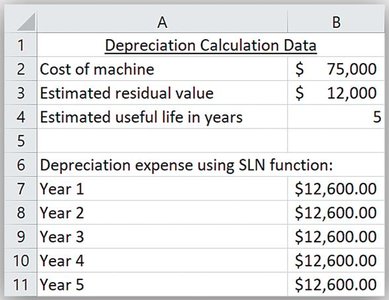

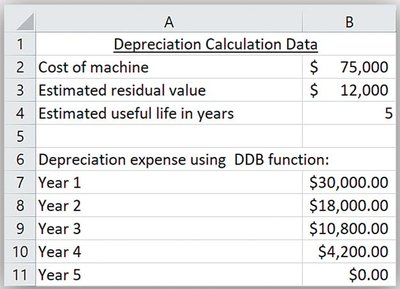

Depreciation Calculations Using Excel Functions

Excel Functions

SLN function: Calculates straight-line depreciation.

DDB function: Calculates double-declining-balance depreciation.