Back

BackReceivables and Revenue: Financial Accounting Chapter 5 Study Guide

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Receivables and Revenue

Revenue Recognition under GAAP

Revenue recognition is a fundamental principle in financial accounting, governed by Generally Accepted Accounting Principles (GAAP). Revenue is recognized when it is earned, which occurs when goods are delivered or services are performed. The amount recorded is either the cash received or the fair market value of assets received in exchange.

Key Point 1: Revenue is recognized when control of goods or services is transferred to the customer.

Key Point 2: The five-step process for revenue recognition includes: identifying the contract, identifying performance obligations, determining the transaction price, allocating the price to obligations, and recognizing revenue when obligations are satisfied.

Example: Apple Inc. recognizes revenue for products when shipped (FOB shipping point) and for services over time as delivered.

Sales Returns and Allowances

Sales returns and allowances account for the possibility that customers may return goods or receive refunds. Companies with significant return experience estimate returns and record them as a contra-revenue account, ensuring proper matching of revenue and related returns in the same period.

Key Point 1: Sales Returns & Allowances is a contra-revenue account with a debit balance.

Key Point 2: Estimated returns are recorded at the time of sale, not when the actual return occurs.

Example: If Apple estimates 1% returns on $200 million sales, it records $2 million in Sales Returns & Allowances.

Sales Discounts

Sales discounts are incentives offered to customers for early payment. These are recorded in a contra-revenue account and reduce the reported sales revenue.

Key Point 1: Typical terms: 2/10, n/30 (2% discount if paid within 10 days, net due in 30 days).

Key Point 2: Sales Revenue on the income statement is reported net of discounts and returns.

Example: A $2,000 sale with a 2% discount results in $1,960 net revenue if paid within the discount period.

Accounts Receivable

Receivables are monetary claims against others and are classified as current assets. They arise from selling goods/services (accounts receivable) or lending money (notes receivable).

Key Point 1: Subsidiary ledgers track individual customer balances.

Key Point 2: Companies manage receivables by credit checks, monitoring payment habits, and separating cash handling from record-keeping.

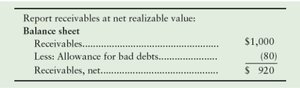

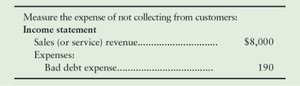

Allowance for Uncollectible Accounts

Not all receivables are collected. The allowance method estimates uncollectible accounts based on past experience, recording an expense and a contra-asset account to reduce accounts receivable to net realizable value (NRV).

Key Point 1: Net Realizable Value (NRV):

Key Point 2: The allowance is a reserve for estimated uncollectibles, not tied to specific customers until write-off.

Example: Apple Inc. reports accounts receivable net of allowance on its balance sheet.

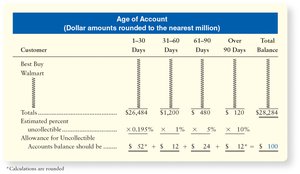

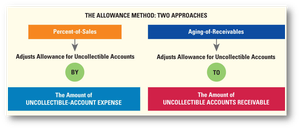

Estimating Uncollectibles: Percent-of-Sales and Aging Methods

There are two main methods for estimating uncollectible accounts:

Percent-of-Sales Method: Calculates expense as a percentage of sales (income statement approach).

Aging-of-Receivables Method: Analyzes receivables by age to estimate allowance (balance sheet approach).

Example: Apple uses an aging schedule to determine the required allowance for uncollectibles.

Writing Off Uncollectible Accounts

When a specific account is determined to be uncollectible, it is written off against the allowance. This does not affect the net realizable value of accounts receivable.

Key Point 1: Write-offs reduce both the allowance and accounts receivable.

Key Point 2: The net accounts receivable remains unchanged after write-off.

Direct Write-Off Method

This method records bad debt expense only when a specific account is deemed uncollectible. It is not GAAP-compliant except for immaterial amounts, as it may overstate assets and fails to match expenses with revenues.

Key Point 1: No allowance account is used.

Key Point 2: Expense is recognized in the period the account is written off.

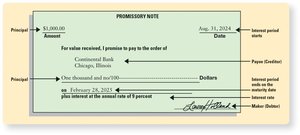

Notes Receivable and Interest Revenue

Notes receivable are formal promises to pay, usually with interest. The creditor records the note as an asset and recognizes interest revenue over time.

Key Point 1: Interest Formula:

Key Point 2: Maturity value is the sum of principal and interest.

Example: A promissory note for $1,000 at 9% annual interest, payable in 6 months.

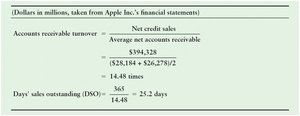

Liquidity Ratios

Liquidity ratios measure a company's ability to pay current liabilities. Three key ratios are:

Quick (Acid-Test) Ratio:

Accounts Receivable Turnover:

Days' Sales Outstanding (DSO):

Example: Apple Inc.'s quick ratio and AR turnover calculations.

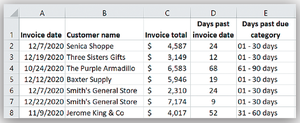

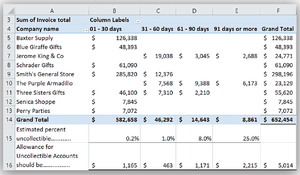

Aging Schedule and Pivot Tables

An aging schedule categorizes receivables by how long they have been outstanding, helping to estimate collectibility. Pivot tables in Excel can summarize large datasets for analysis.

Key Point 1: Older receivables are less likely to be collected.

Key Point 2: Pivot tables allow for efficient analysis of receivables by age and customer.

Example: Pinkettle Company uses an Excel pivot table to analyze unpaid invoices and estimate uncollectibles.

Additional info: The notes above expand on brief points with academic context, definitions, formulas, and examples to ensure completeness and clarity for exam preparation.