Back

BackReceivables and Revenue: Recognition, Management, and Analysis

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Receivables and Revenue

Revenue Recognition under GAAP

Revenue recognition is a fundamental principle in financial accounting, governed by Generally Accepted Accounting Principles (GAAP). Revenue is recognized when it is earned, which typically occurs when goods are delivered or services are performed. The amount recorded is either the cash received or the fair market value of assets received in exchange.

Contract: An agreement between two parties that creates enforceable rights or performance obligations.

Five-Step Model:

Identify the contract(s).

Identify the performance obligation(s).

Determine the transaction price.

Allocate the transaction price to the performance obligations.

Recognize revenue when the entity satisfies the obligations.

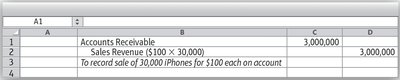

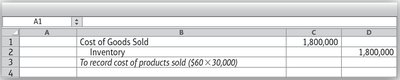

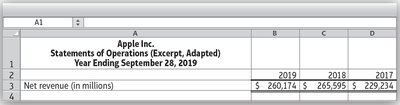

Example: Apple Inc. recognizes revenue when control of products is transferred to customers, typically when products are shipped. For services, revenue is recognized over time as services are delivered.

Shipping Terms

Shipping terms affect the timing of revenue recognition:

FOB Shipping Point: Ownership changes hands and revenue is recognized when goods leave the shipping dock.

FOB Destination: Ownership changes hands and revenue is recognized at the point of delivery to the customer.

Speeding Up Cash Flow from Sales

Businesses employ strategies to accelerate cash flow from sales:

Sales discounts for early payment

Charging interest after a certain period

Effective credit and collection procedures

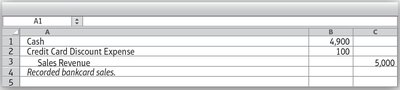

Emphasizing credit card or bankcard sales

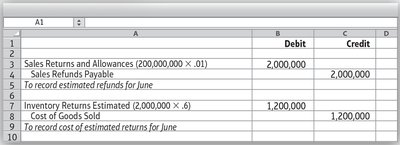

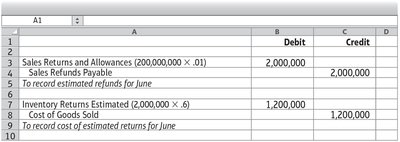

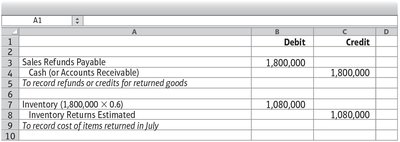

Sales Returns and Allowances

Sales returns and allowances account for customer rights to return unsatisfactory or damaged goods. A credit memo authorizes a credit to the customer’s account receivable.

Estimation: Companies estimate returns based on historical experience and adjust inventory and sales accordingly.

Example: If Apple expects 1% of sales to be returned, it records estimated refunds and inventory returns at month-end.

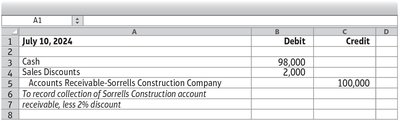

Sales Discounts

Sales discounts incentivize early payment by customers. A common term is 2/10, n/30, meaning a 2% discount is offered if payment is made within 10 days; otherwise, the full amount is due in 30 days.

Example: Ace Hardware offers 2/10, n/30 on sales. If a customer pays within 10 days, the discount is applied.

Disclosure of Net Revenues

Sales revenue is typically disclosed at the net amount on the income statement, after subtracting sales discounts and returns.

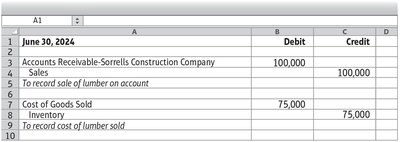

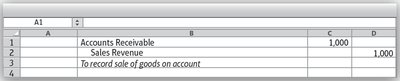

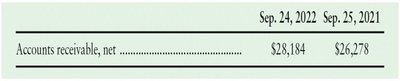

Accounts Receivable

Receivables are monetary claims against others and are classified as current assets. They are acquired by selling goods/services (accounts receivable) or lending money (notes receivable).

Managing Receivables: Companies manage the risk of non-collection by running credit checks, extending credit only to creditworthy customers, separating cash handling and record-keeping, monitoring payment habits, and sending reminders.

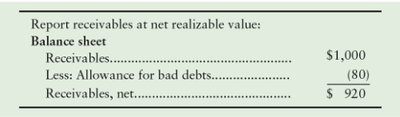

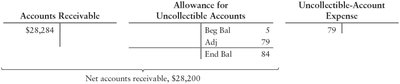

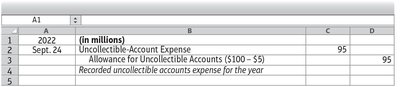

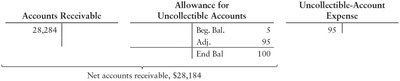

Allowance for Uncollectible Accounts

Companies rarely collect all receivables. The allowance method is used to estimate and record uncollectible accounts expense, based on past collection experience. The allowance for uncollectible accounts is a contra account to accounts receivable.

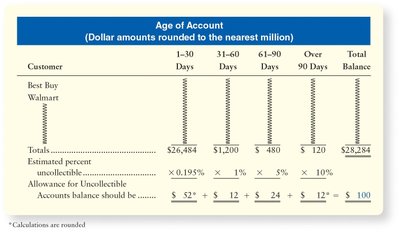

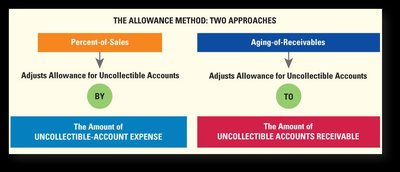

Estimating Uncollectibles: Percent-of-Sales and Aging-of-Receivables Methods

There are two main methods for estimating uncollectible accounts:

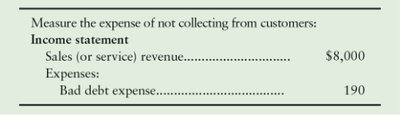

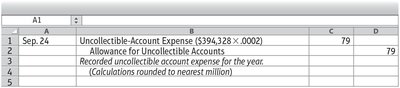

Percent-of-Sales Method: Computes uncollectible-account expense as a percent of revenue (income statement approach).

Aging-of-Receivables Method: Analyzes specific accounts based on how long they have been outstanding (balance sheet approach).

Writing Off Uncollectible Accounts

When specific accounts are determined to be uncollectible, they are written off against the allowance for uncollectible accounts.

Direct Write-Off Method

The direct write-off method records expense when a specific customer’s account proves to be uncollectible. This method is less preferable and not GAAP-compliant, as it may overstate assets and fails to match expenses with related revenue.

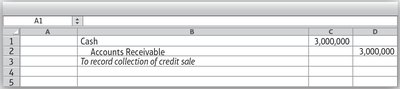

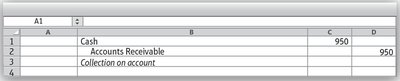

Computing Cash Collections from Customers

Receivables typically involve five items: beginning balance, sales revenue, write-offs, collections, and ending balance. If all items except collections are known, collections can be computed by solving for X.

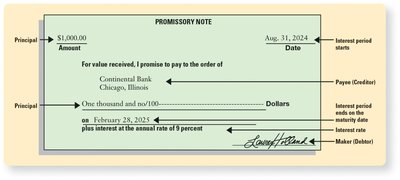

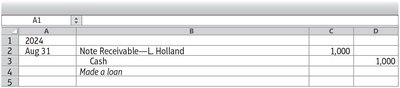

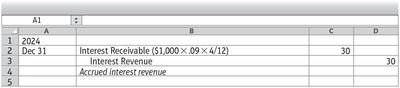

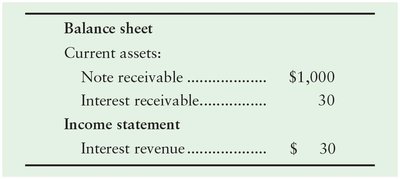

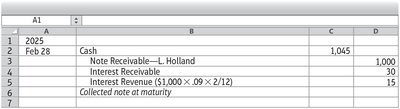

Notes Receivable and Interest Revenue

Notes receivable arise when money is lent and formalized with a promissory note. The creditor (lender) is owed money, while the debtor (borrower) owes money. Interest is the cost of borrowing, stated as an annual percentage rate.

Maturity Date: The date the debtor must pay the note.

Maturity Value: The sum of principal and interest.

Principal: The amount borrowed.

Term: The length of time from signing to payment.

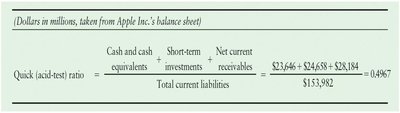

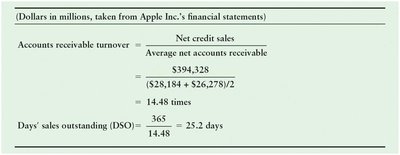

Liquidity Ratios

Liquidity ratios help evaluate a company’s ability to pay current liabilities.

Quick (Acid-Test) Ratio: A higher ratio indicates easier payment of current liabilities. The benchmark is 1:1.

Accounts Receivable Turnover: Shows how many times per year a company collects its average accounts receivable. A higher number is better.

Days' Sales Outstanding (DSO): A lower DSO indicates faster cash collection.

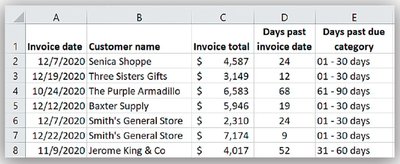

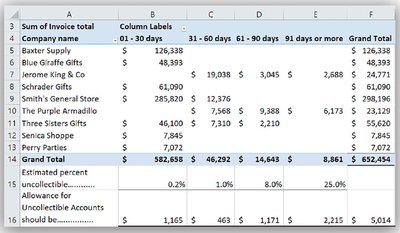

Analyzing Receivables Collectibility Using an Aging Schedule and Excel Pivot Table

An aging schedule categorizes receivables based on how long they have been outstanding, helping to estimate uncollectible accounts. Excel pivot tables can summarize large data sets, allowing for focused analysis of receivables collectibility.

Example: Pinkettle Company summarizes its accounts receivable in a pivot table, categorizing invoices by age and estimating uncollectible amounts.

Summary Table: Allowance Methods

Method | Basis | Approach |

|---|---|---|

Percent-of-Sales | Revenue | Income Statement |

Aging-of-Receivables | Outstanding Receivables | Balance Sheet |

Key Formulas

Quick Ratio:

Accounts Receivable Turnover:

Days' Sales Outstanding (DSO):

Additional info:

All journal entries and tables are based on textbook examples and real company data (e.g., Apple Inc.).

Images included are directly relevant to the explanation of each paragraph and reinforce key accounting concepts.