Back

BackRecording Business Transactions: Foundations of Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 2: Recording Business Transactions

Introduction

This chapter introduces the fundamental process of recording business transactions in financial accounting. It covers the structure of accounts, the double-entry system, the use of journals and ledgers, and the preparation of a trial balance. Mastery of these concepts is essential for accurate financial reporting and analysis.

Accounts and the Accounting Equation

What Is an Account?

An account is a detailed record of all increases and decreases that have occurred in a specific asset, liability, or equity item during a period. Accounts are organized according to the accounting equation:

Assets: Resources owned by the business (e.g., cash, accounts receivable, land).

Liabilities: Obligations owed to outsiders (e.g., accounts payable, notes payable).

Equity: Owner's claims on the business (e.g., common stock, retained earnings).

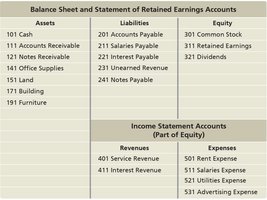

Chart of Accounts

A chart of accounts is a systematic listing of all accounts used by a business, organized by type. The ledger is the record that holds all these accounts and their balances.

Debits, Credits, and Double-Entry Accounting

Double-Entry Accounting System

The double-entry accounting system ensures that every transaction affects at least two accounts, maintaining the balance of the accounting equation. Each transaction is recorded with equal debits and credits.

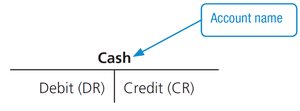

The T-Account

A T-account is a simplified representation of an account, showing debits on the left and credits on the right.

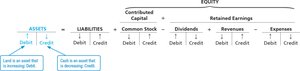

Rules of Debits and Credits

The rules for recording increases and decreases depend on the account type:

Assets: Increase with debits, decrease with credits.

Liabilities: Increase with credits, decrease with debits.

Equity: Increase with credits, decrease with debits.

Normal Account Balances

The normal balance of an account is the side (debit or credit) that increases the account. For example, asset accounts normally have a debit balance, while liability and equity accounts normally have a credit balance.

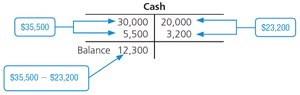

Determining Account Balances

The balance of a T-account is found by subtracting the smaller side from the larger side. The result is the ending balance, which appears on the side with the larger total.

Journalizing and Posting Transactions

Source Documents

Transactions are supported by source documents such as invoices, checks, and receipts. These documents provide evidence for recording transactions.

Steps in Journalizing and Posting

Identify the accounts and their types (asset, liability, equity).

Determine if each account increases or decreases and apply debit/credit rules.

Record the transaction in the journal (chronological record).

Post the journal entry to the ledger (individual accounts).

Ensure the accounting equation remains balanced.

Example: Stockholder Contribution

On November 1, a business receives $30,000 cash from an owner in exchange for common stock. The journal entry is:

Debit Cash $30,000

Credit Common Stock $30,000

Example: Purchase of Land for Cash

On November 2, the business pays $20,000 cash for land. The journal entry is:

Debit Land $20,000

Credit Cash $20,000

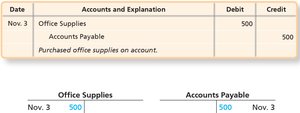

Example: Purchase of Office Supplies on Account

On November 3, the business buys $500 of office supplies on account. The journal entry is:

Debit Office Supplies $500

Credit Accounts Payable $500

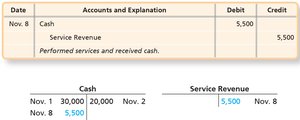

Example: Earning Service Revenue for Cash

On November 8, the business earns $5,500 in service revenue and receives cash. The journal entry is:

Debit Cash $5,500

Credit Service Revenue $5,500

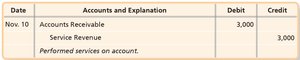

Example: Earning Service Revenue on Account

On November 10, the business earns $3,000 in service revenue on account. The journal entry is:

Debit Accounts Receivable $3,000

Credit Service Revenue $3,000

Trial Balance and Financial Statements

What Is a Trial Balance?

A trial balance is a list of all ledger accounts and their balances at a specific point in time. It is used to verify that total debits equal total credits before preparing financial statements.

Correcting Trial Balance Errors

If total debits do not equal total credits, check for missing accounts or errors in addition.

Divide the difference by 2 to check for double posting.

Divide the difference by 9 to check for transposition errors.

Note: Even if debits equal credits, errors may still exist (e.g., wrong accounts used).

Evaluating Business Performance: The Debt Ratio

Debt Ratio

The debt ratio measures the proportion of assets financed by debt. It is calculated as:

A higher debt ratio indicates greater financial risk.

It helps assess a company's ability to pay its debts and overall financial health.

Summary Table: Key Account Types

Account Type | Normal Balance | Increases By | Decreases By |

|---|---|---|---|

Assets | Debit | Debit | Credit |

Liabilities | Credit | Credit | Debit |

Equity | Credit | Credit | Debit |

Revenue | Credit | Credit | Debit |

Expenses | Debit | Debit | Credit |

Dividends | Debit | Debit | Credit |

Additional info: This summary includes expanded academic context and examples to ensure the notes are self-contained and suitable for exam preparation.