Back

BackRecording Business Transactions: Principles of Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Recording Business Transactions

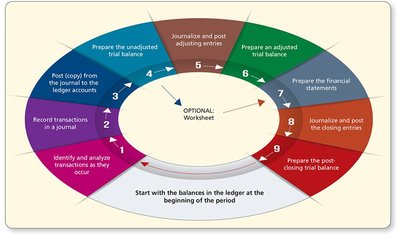

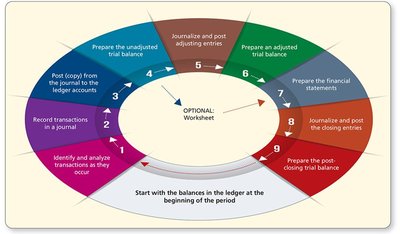

The Accounting Cycle

The accounting cycle is a systematic process used to record and summarize business transactions for a specific period. It ensures that all financial events are accurately captured and reported in the financial statements.

Step 1: Identify and analyze transactions as they occur

Step 2: Record transactions in a journal

Step 3: Post from the journal to the ledger accounts

Step 4: Prepare the unadjusted trial balance

Step 5: Journalize and post adjusting entries

Step 6: Prepare an adjusted trial balance

Step 7: Prepare the financial statements

Step 8: Journalize and post the closing entries

Step 9: Prepare the post-closing trial balance

Key Accounting Terms

Understanding the terminology is essential for recording business transactions:

Transaction: An event that affects the financial position of an entity and can be reliably measured.

Journal: A chronological record of all transactions.

Ledger: A collection of accounts showing the changes and balances for each account.

Chart of Accounts: A list of all accounts used by the entity, organized by type and number.

Transaction Analysis

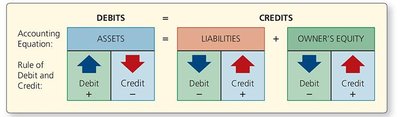

The Accounting Equation

All business transactions are analyzed using the accounting equation:

Assets = Liabilities + Owner’s Equity

Each transaction affects at least two accounts, maintaining the balance of the equation.

Rules of Debit and Credit

The rules of debit and credit determine how increases and decreases are recorded in each account type:

Assets: Increase with debits, decrease with credits

Liabilities: Increase with credits, decrease with debits

Owner’s Equity: Increase with credits, decrease with debits

These rules extend to revenues and expenses:

Revenues: Increase with credits

Expenses: Increase with debits

Withdrawals: Increase with debits

Normal Balance of Accounts

The normal balance is the side (debit or credit) where increases are recorded:

Assets, Expenses, Withdrawals: Debit

Liabilities, Revenues, Capital: Credit

Mnemonic: All Elephants Will Love Rowdy Children (Assets, Expenses, Withdrawals = Debit; Liabilities, Revenues, Capital = Credit)

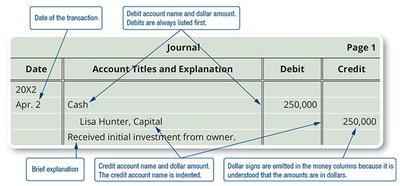

Recording Transactions in the Journal

Journalizing Transactions

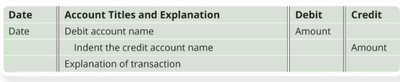

Journalizing is the process of recording transactions in the journal. Each entry includes:

Date of the transaction

Account titles and explanation

Debit and credit amounts

A brief explanation

Date | Account Titles and Explanation | Debit | Credit |

|---|---|---|---|

Apr. 2 | Cash Lisa Hunter, Capital Received initial investment from owner. | 250,000 | 250,000 |

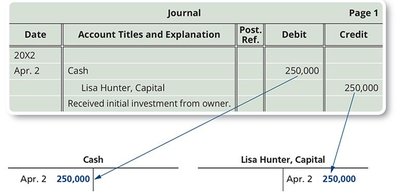

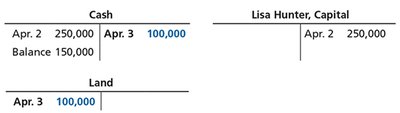

Posting to the Ledger

Ledger Accounts and T-Accounts

After journalizing, amounts are posted to the ledger, which tracks all transactions for each account. T-Accounts are informal tools to visualize the effect of transactions.

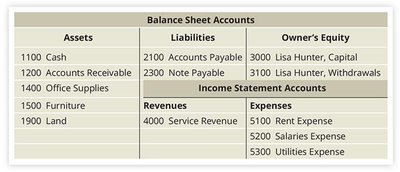

Chart of Accounts

Structure and Numbering

The chart of accounts organizes all accounts used by the entity. Accounts are numbered and grouped by type:

1xxx: Assets

2xxx: Liabilities

3xxx: Owner’s Equity

4xxx: Revenues

5xxx: Expenses

Trial Balance

Preparing the Unadjusted Trial Balance

The trial balance is a summary of all ledger accounts and their balances, used to verify that total debits equal total credits.

Presented in the order: Assets, Liabilities, Owner’s Equity, Revenues, Expenses

Used to detect errors before preparing financial statements

Summary of Recording Business Transactions

Key Points

Transactions are analyzed and recorded using the accounting equation and rules of debit and credit.

Journal entries are posted to the ledger, which tracks account balances.

The trial balance ensures the records are in balance before financial statements are prepared.

Examples and Applications

Sample Journal Entry and Posting

Example: Owner invests $250,000 cash in the business.

Journal Entry: Debit Cash $250,000; Credit Capital $250,000

Ledger Posting: Cash account shows debit; Capital account shows credit

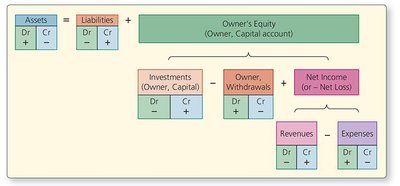

Expanded Accounting Equation

The expanded accounting equation incorporates investments, withdrawals, revenues, and expenses:

Formulas and Equations

Basic Accounting Equation:

Expanded Accounting Equation:

Additional info:

Source documents (e.g., invoices, deposit slips, cheques) provide evidence for transactions and are essential for analysis.

Posting references help trace amounts between the journal and ledger.

Double-entry accounting ensures every transaction affects at least two accounts, maintaining the balance of the accounting equation.