Back

BackRecording Business Transactions: The Accounting Cycle and Double-Entry System

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Recording Business Transactions

Key Accounting Terms

Understanding the terminology used in accounting is essential for accurately recording business transactions. The accounting cycle involves several key components:

Account: A record for each asset, liability, equity, revenue, or expense item. For example, a Cash account tracks all cash transactions.

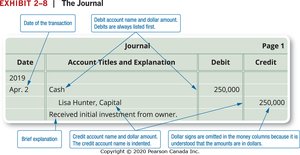

Journal: The chronological record of all transactions. Each transaction is first entered here.

Ledger: A collection of all accounts, where journal entries are posted to individual accounts.

Trial Balance: A summary listing all ledger accounts and their balances, used to check the accuracy of the records.

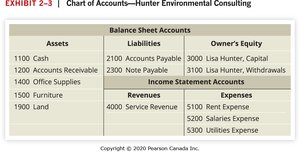

Chart of Accounts

The chart of accounts is a structured list of all accounts used by an entity, organized by type and assigned unique numbers. This facilitates efficient tracking and reporting.

Assets: Begin with 1 (e.g., 1100 Cash)

Liabilities: Begin with 2 (e.g., 2100 Accounts Payable)

Owner’s Equity: Begin with 3 (e.g., 3100 Withdrawals)

Revenues: Begin with 4 (e.g., 4000 Service Revenue)

Expenses: Begin with 5 (e.g., 5100 Rent Expense)

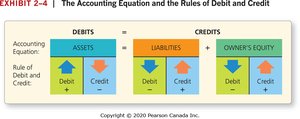

Rules of Debit and Credit

Accounting uses the double-entry system, where every transaction affects at least two accounts. The rules of debit and credit depend on the type of account:

Assets: Increase with debits, decrease with credits

Liabilities: Increase with credits, decrease with debits

Owner’s Equity: Increase with credits, decrease with debits

T-Account: A visual tool to represent the effects of transactions. Debits are on the left, credits on the right. Not part of formal records, but useful for analysis.

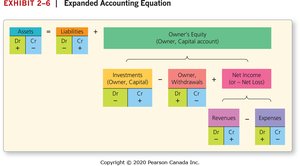

Expanded Accounting Equation

The accounting equation forms the foundation of double-entry accounting:

Basic Equation:

Expanded Equation:

Normal Balance of Accounts

The normal balance is the side (debit or credit) where increases are recorded for each account type:

Assets, Withdrawals, Expenses: Debit

Liabilities, Owner’s Equity, Revenues: Credit

A helpful acronym: DR. AWE (Debits for Assets, Withdrawals, Expenses).

Analyzing and Recording Transactions

Transactions are identified from source documents (e.g., invoices, cheques, deposit slips). The process of journalizing includes:

Identify the transaction from source documents

Analyze which accounts are affected and whether they increase or decrease

Apply the rules of debit and credit

Verify the accounting equation remains balanced

Record the journal entry with an explanation

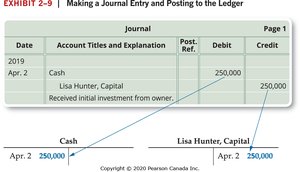

Journal Entries and Posting to the Ledger

Journal entries include the date, account titles, debit and credit amounts, and a brief explanation. Posting is the process of transferring these entries to the ledger, which tracks all transactions for each account.

Preparing and Using a Trial Balance

The trial balance is a summary of all ledger accounts and their balances, listed in the order: assets, liabilities, owner’s equity, revenues, and expenses. It checks whether total debits equal total credits, ensuring the records are balanced.

Do not confuse the trial balance with the balance sheet.

Useful for detecting errors in recording or posting.

Correcting Trial Balance Errors

Common steps to correct errors include:

Search for missing accounts

Check the journal for the amount of the difference

Divide the difference by 2 to identify mixed debit/credit errors

Divide the difference by 9 to detect slide or transposition errors

Example

If the trial balance is out of balance by $610, dividing by 9 gives 67.78, which may indicate a transposition error (e.g., $16 instead of $61).

Additional info: The notes above expand on brief points from the original slides, providing definitions, examples, and formulas for clarity and completeness.