Back

BackValuation of Inventories: A Cost-Basis Approach (Intermediate Accounting, Chapter 7)

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Valuation of Inventories: A Cost-Basis Approach

Inventory Classification and Types

Inventory is a key asset for companies, representing items held for sale or used in production. The classification of inventory depends on the type of company:

Merchandising Company: Maintains one inventory account for goods purchased ready for sale.

Manufacturing Company: Maintains three inventory accounts: Raw Materials, Work in Process, and Finished Goods.

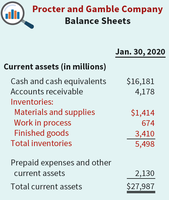

Example: The balance sheet of Procter and Gamble Company (Jan. 30, 2020) shows inventory classified as materials and supplies, work in process, and finished goods.

Goods and Costs Included in Inventory

Determining which goods and costs are included in inventory is essential for accurate financial reporting. Companies recognize inventory and accounts payable when they control the asset, often determined by the passage of title.

Goods Included: Inventory includes goods owned by the company, even if not physically present (e.g., goods in transit).

Consigned Goods: Goods out on consignment remain the property of the consignor; the consignee does not record them as inventory.

Costs Included: Inventory costs include all expenditures directly connected with bringing goods to the buyer’s place of business and converting them to a salable condition (Product Costs). Period Costs are indirect and not included in inventory.

Example: The distinction between FOB shipping point and FOB destination affects when ownership and inventory recognition occur.

Inventory Cost Flow Assumptions

Companies adopt cost flow assumptions to allocate costs to inventory and cost of goods sold. The chosen method does not need to match the physical flow of goods, but should best reflect periodic income.

Specific Identification: Matches actual costs to actual items sold; used for costly, easily distinguishable items. May allow income manipulation.

FIFO (First-In, First-Out): Assumes earliest goods purchased are sold first. Ending inventory reflects current costs, but may result in higher taxes.

LIFO (Last-In, First-Out): Assumes latest goods purchased are sold first. Matches current costs to revenue, but may lower income and current assets.

Average Cost: Prices inventory based on average cost of all goods available. Not subject to income manipulation.

Formula: The basic formula for cost of goods sold is:

Special Issues Related to LIFO

LIFO presents unique challenges and considerations:

LIFO Reserve: The difference between inventory reported under LIFO and another method (e.g., FIFO) for internal reporting. Companies must disclose the LIFO reserve or replacement cost.

LIFO Liquidation: Selling older, low-cost inventory can increase net income and taxes, distorting financial results.

Dollar-Value LIFO: Measures inventory changes in dollar value, not physical quantity, protecting LIFO layers from erosion.

Example: Dollar-Value LIFO calculation involves adjusting inventory for price changes to determine real increases in inventory quantity.

Summary Table: Inventory Classification (Manufacturing Company)

Inventory Type | Description | Example (Procter & Gamble) |

|---|---|---|

Raw Materials | Items to be used in production | $1,414 million |

Work in Process | Goods partially completed | $674 million |

Finished Goods | Completed goods ready for sale | $3,410 million |

Total Inventories | Sum of all inventory types | $5,498 million |

Key Learning Objectives

Compute goods and costs included in inventory.

Understand periodic vs. perpetual inventory systems.

Distinguish between beginning inventory, purchases, cost of goods available for sale, cost of goods sold, and ending inventory.

Compute ending inventory and cost of goods sold under specific identification, FIFO, LIFO, Dollar-Value LIFO, and Average Cost methods.