Back

BackBanks, Money, and the Federal Reserve System: Study Notes for Macroeconomics

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 14: Banks, Money, and the Federal Reserve System

14.1 What Is Money, and Why Do We Need It?

Money is a fundamental economic invention that facilitates exchange and specialization. Economists define money as any asset that is generally accepted in exchange for goods and services or for the payment of debts.

Definition of Money: An asset widely accepted as payment for goods, services, or debts.

Barter System: Before money, trade required a double coincidence of wants, making transactions inefficient.

Commodity Money: Goods with intrinsic value (e.g., gold, silver, animal skins) used as money.

The Four Primary Functions of Money:

Medium of Exchange: Accepted as payment for goods and services.

Unit of Account: Provides a standard measure of value.

Store of Value: Retains value over time, allowing deferred consumption.

Standard of Deferred Payment: Facilitates transactions over time with predictable value.

Characteristics of Good Money:

Acceptable to most people

Standardized quality

Durable

Valuable relative to weight

Divisible

Transition to Fiat Money: Modern economies use fiat money, which is currency authorized by a central bank and not backed by a physical commodity. Its value depends on public confidence.

Advantages and Disadvantages of Fiat Money:

Advantage: Flexibility for central banks to manage the money supply.

Disadvantage: Relies on public confidence; loss of trust can render it worthless.

Legal Tender and Cashless Society: Businesses are not required to accept cash for all transactions. The trend toward cashless payments has accelerated, especially during the Covid-19 pandemic.

14.2 How Is Money Measured in the United States Today?

Measuring the money supply is complex due to the variety of assets that can serve as money. The U.S. uses two main definitions:

M1: Currency in circulation, checking account deposits, and savings account deposits.

M2: Includes M1 plus small-denomination time deposits and noninstitutional money market fund shares.

Recent Data (September 2023):

M1: $18.1 trillion

M2: $20.8 trillion

About 13% of M1 is currency; 75% of U.S. paper currency is $100 bills.

Debit and Credit Cards:

Debit cards access checking accounts (the account is money, not the card).

Credit cards are not money; they represent short-term loans.

Digital Money and Cryptocurrencies: Digital payment systems (e.g., PayPal, Apple Pay) are increasingly trusted. Bitcoin is a decentralized digital currency, but is not currently included in official money supply measures.

14.3 The Role of Banks in the Economy

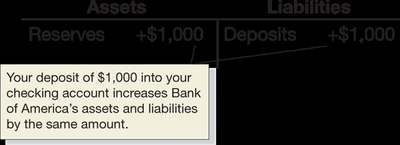

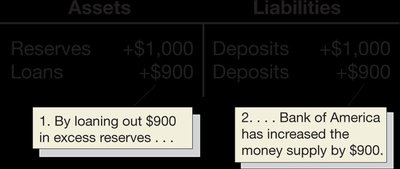

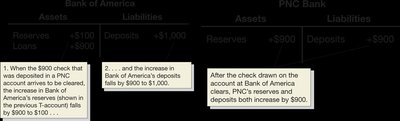

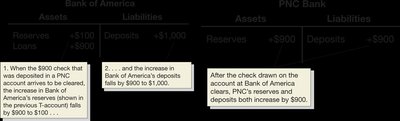

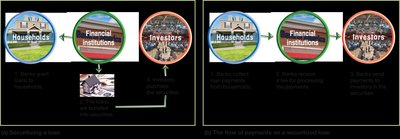

Banks are profit-seeking firms that play a critical role in the creation of money and the allocation of credit. They operate by accepting deposits and making loans, which expands the money supply.

Balance Sheet: Assets (reserves, loans, securities) and liabilities (deposits, borrowings, equity) must balance.

Reserves: Cash held in vaults or on deposit with the central bank. U.S. reserve requirements were eliminated in 2020.

Fractional Reserve Banking: Banks keep less than 100% of deposits as reserves, lending out the rest.

Economic Importance of Banks:

Reduce transaction costs through specialization and economies of scale.

Reduce information problems (asymmetric information) by evaluating borrower risk.

Money Creation Process: When banks lend out deposits, they create new money in the form of checking account balances. This process is illustrated by the money multiplier.

Money Multiplier: The ratio of the money supply to the monetary base. It fluctuates due to changes in bank reserves and public currency holdings.

14.4 The Federal Reserve System

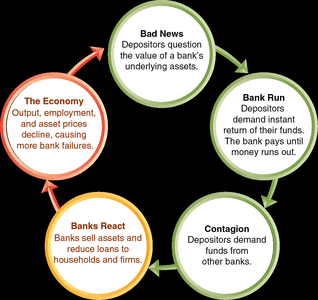

The Federal Reserve (the Fed) is the central bank of the United States. It was established to prevent bank panics and now manages monetary policy and regulates banks.

Bank Run: Many depositors withdraw funds simultaneously due to loss of confidence.

Bank Panic: Multiple banks experience runs at the same time.

Lender of Last Resort: The Fed provides emergency loans to prevent bank failures and panics.

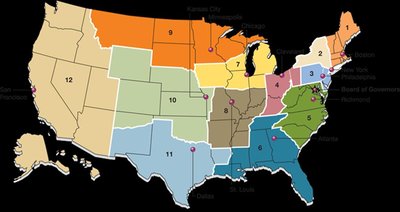

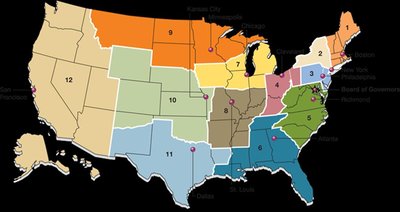

Structure of the Federal Reserve:

Board of Governors: Seven members appointed for 14-year terms; one serves as chair.

Federal Open Market Committee (FOMC): Twelve members (Board of Governors + regional bank presidents) manage open market operations and the money supply.

Monetary Policy: The Fed manages interest rates and the money supply to achieve macroeconomic objectives (e.g., stable prices, full employment).

Open Market Operations: Buying and selling Treasury securities to influence the money supply.

To increase the money supply: The Fed buys securities.

To decrease the money supply: The Fed sells securities.

Bank Regulation: Banks are regulated by the Fed, FDIC, and other agencies to ensure stability and liquidity. The FDIC insures deposits up to $250,000.

Moral Hazard: Protecting depositors can encourage risky behavior by banks. The FDIC resolves failed banks to minimize costs and discourage excessive risk-taking.

Shadow Banking System: Nonbank financial firms (investment banks, money market funds, hedge funds) provide credit and liquidity, increasing complexity and risk in the financial system.

Securitization: The process of transforming loans into tradable securities, increasing liquidity but also risk.

14.5 The Quantity Theory of Money

The quantity theory of money explains the relationship between the money supply and the price level. It is formalized by the quantity equation:

Quantity Equation:

M: Money supply

V: Velocity of money (average number of times each dollar is used in transactions)

P: Price level

Y: Real output (real GDP)

Rearranged:

Quantity Theory of Money: Assumes velocity is constant. The growth rate form:

If velocity is constant:

If money supply grows faster than real GDP, inflation occurs.

If money supply grows slower than real GDP, deflation occurs.

If money supply grows at the same rate as real GDP, price level is stable.

Empirical Evidence: Over the long run, higher money supply growth is associated with higher inflation, though velocity is not perfectly constant.

Hyperinflation

Extremely high inflation (over 50% per month) results from rapid money supply growth, often when governments finance spending by creating money. Examples include Zimbabwe (2000s) and Venezuela (2019).

Historical Example: German Hyperinflation (1922–1923)

After World War I, Germany financed reparations by expanding the money supply, leading to hyperinflation and the collapse of the German mark's value.