Back

BackChapter 11: Long-Run Economic Growth—Sources and Policies

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Long-Run Economic Growth: Sources and Policies

Introduction

Long-run economic growth is a central topic in macroeconomics, focusing on the sustained increase in real GDP per capita and the factors that drive improvements in living standards. This chapter explores the historical patterns of growth, the determinants of productivity, and the role of government policies in fostering economic development.

11.1 Economic Growth Over Time and Around the World

Defining Economic Growth and Global Trends

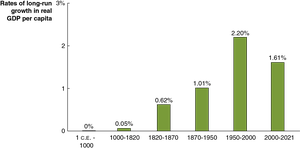

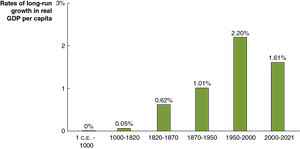

Economic growth refers to the increase in real GDP per capita over time. Most global economic growth has occurred in the last two centuries, with the Industrial Revolution marking a turning point for sustained increases in living standards.

Economic Growth Rate: The percentage change in real GDP per capita from one period to another.

Industrial Revolution: The application of mechanical power to production, beginning in England around 1750, which enabled long-run growth.

Global Divergence: Small differences in growth rates can lead to large differences in living standards over decades.

Example: Over 50 years, a 1.61% growth rate results in a 122% increase in real GDP per capita, while a 2.20% rate leads to a 197% increase.

The Industrial Revolution and Its Origins

The Industrial Revolution began in England due to institutional changes, such as the Glorious Revolution, which established property rights and an independent court system. These changes incentivized investment and entrepreneurship.

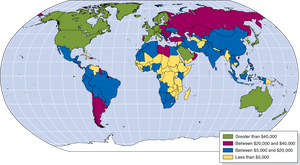

Variation in Living Standards

High-income countries (e.g., Western Europe, US, Japan) have much higher real GDP per capita than developing countries. Newly industrializing countries like Singapore and South Korea have transitioned to higher income levels.

Beyond Income: Other Measures of Well-Being

While income is a key indicator, improvements in health, education, and civil liberties also contribute to living standards. Technological and knowledge advances can improve well-being even without significant income growth.

11.2 What Determines How Fast Economies Grow?

Economic Growth Model and Labor Productivity

An economic growth model explains long-run growth rates in real GDP per capita. The key determinant is labor productivity: the quantity of goods and services produced by one worker or one hour of work.

Capital per Hour Worked: More capital (machinery, equipment) increases productivity.

Technological Change: Improvements in the ability to produce output with given inputs.

Sources of Technological Change

Better Machinery and Equipment: Innovations like steam engines and computers.

Increases in Human Capital: Education and training enhance worker skills.

Better Organization and Management: Improved production methods, such as just-in-time systems.

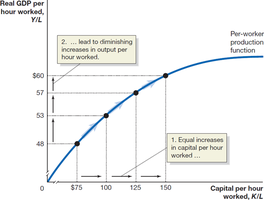

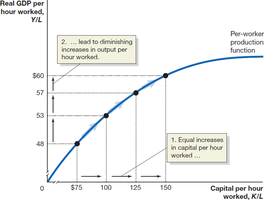

The Per-Worker Production Function

The per-worker production function shows the relationship between real GDP per hour worked and capital per hour worked, holding technology constant. Initial increases in capital are highly effective, but subsequent increases yield diminishing returns.

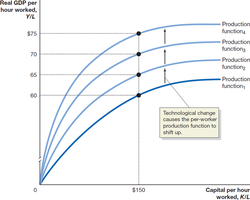

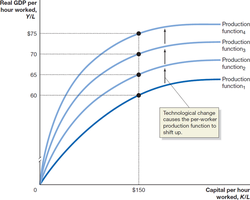

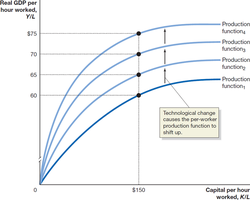

Technological Change and Output

Technological change shifts the production function upward, allowing higher output per hour worked without increasing capital. Unlike capital, technological change does not suffer from diminishing returns.

Example: Soviet Union's Economic Failure

The Soviet Union focused on capital accumulation but neglected technological change due to lack of competition and incentives. This led to slowing growth rates despite initial productivity gains.

New Growth Theory

Developed by Paul Romer, new growth theory emphasizes that technological change is driven by economic incentives and market forces. Knowledge capital is a key determinant, with increasing returns at the economy level.

Physical Capital: Rival and excludable (private good), subject to diminishing returns.

Knowledge Capital: Nonrival and nonexcludable (public good), leads to increasing returns.

Government's Role in Knowledge Capital

Protecting Intellectual Property: Patents and copyrights incentivize innovation.

Subsidizing R&D and Education: Direct research, tax incentives, and education subsidies foster technological progress.

Creative Destruction

Joseph Schumpeter's concept of creative destruction describes how new products and technologies replace old ones, driving economic growth. Entrepreneurs are central to this process, combining factors of production in innovative ways.

11.3 Economic Growth in the United States

Fluctuations in Productivity Growth

U.S. productivity growth has varied over time, with high rates during periods of technological innovation and investment. Growth slowed in the mid-1970s but picked up in the 1990s due to information technology.

Measurement Issues

Recent productivity growth may be understated due to difficulties in measuring service output and consumer surplus from technological advances.

Role of Information Technology

IT has driven productivity improvements, but debate exists over whether future growth will remain high or slow down.

Secular Stagnation vs. Return to Growth

Some economists predict continued low growth due to demographic and capital trends, while others expect investment and global demand to spur faster growth.

11.4 Why Isn’t the Whole World Rich?

Economic Catch-Up and Its Limitations

The economic growth model predicts that poor countries should grow faster than rich ones, leading to convergence in living standards. However, this catch-up has not occurred universally.

Catch-Up: Poor countries grow faster and converge to rich countries' income levels.

Barriers to Catch-Up

Weak Institutions: Lack of property rights and rule of law discourages entrepreneurship.

Wars and Revolutions: Instability hinders investment and growth.

Poor Public Education and Health: Reduces worker productivity.

Low Rates of Saving and Investment: Vicious cycle of underdevelopment.

Benefits of Globalization

Globalization, through foreign direct and portfolio investment, helps countries escape low savings and investment cycles, fostering higher growth rates.

11.5 Growth Policies

Government Policies to Foster Growth

Enhancing Property Rights and Rule of Law: Independent courts and anti-corruption measures encourage investment.

Improving Health and Education: Increases productivity and prevents brain drain.

Promoting Technological Change: Encouraging R&D and foreign investment.

Promoting Savings and Investment: Tax incentives and secure financial systems.

Case Studies

China vs. Mexico: China's transition to a market economy and strong institutions led to rapid growth, while Mexico's weak rule of law hindered progress.

Sub-Saharan Africa: Recent FDI in manufacturing and services is promising, but improved governance is essential for sustained growth.

Debate: Is Economic Growth Always Good?

While growth is beneficial for low-income countries, concerns exist about environmental impacts, resource depletion, and cultural changes in high-income countries. Economic analysis informs but does not resolve these normative debates.

Key Terms and Concepts

Real GDP per capita: Real gross domestic product divided by population.

Labor productivity: Output per worker or per hour worked.

Technological change: Improvements in production methods.

Human capital: Skills and knowledge acquired by workers.

Catch-up: Convergence of poor countries to rich countries' income levels.

Creative destruction: Replacement of old products and firms by new innovations.

Globalization: Increased openness to foreign trade and investment.

Key Equations

Growth Rate Formula:

Per-Worker Production Function:

Where is real GDP, is labor, is capital, and is the production function.

Additional info: Some images and tables referenced in the original material were not included due to lack of direct relevance or clarity. All key concepts and models have been expanded for academic completeness.