Back

BackChapter 11: Long-Run Economic Growth—Sources and Policies

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Long-Run Economic Growth: Sources and Policies

Introduction to Economic Growth

Economic growth refers to the sustained increase in a country's output of goods and services, typically measured as real GDP per capita. Understanding the sources and policies that drive long-run economic growth is essential for explaining differences in living standards across countries and over time.

Economic Growth Over Time and Around the World

Definition and Measurement of Economic Growth

Economic growth is the increase in real GDP per capita over time.

Growth rates are calculated as the percentage change in real GDP per capita from one period to another.

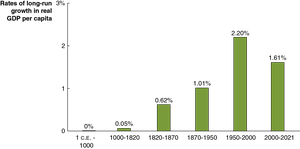

Most global economic growth has occurred in the last two centuries, especially since the Industrial Revolution.

The Industrial Revolution and Its Impact

The Industrial Revolution began in England around 1750, marking the shift from human and animal power to mechanical power in production.

This transition enabled sustained long-run economic growth in England and later in other countries.

Global Trends in Living Standards

Small differences in growth rates can lead to large differences in living standards over time.

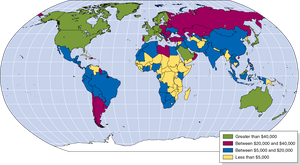

High-income countries have much higher real GDP per capita than developing countries, even after adjusting for cost-of-living differences.

Beyond Income: Other Measures of Well-Being

While income is a key indicator, improvements in health, education, and civil liberties also contribute to higher living standards.

Technological and knowledge advances can improve well-being even without significant income growth.

What Determines How Fast Economies Grow?

The Economic Growth Model

An economic growth model explains long-run growth in real GDP per capita by focusing on labor productivity, which is the amount of goods and services produced per worker or per hour worked.

Two main factors affect labor productivity:

The quantity of capital per hour worked

The level of technology

Sources of Technological Change

Better machinery and equipment (e.g., steam engine, computers)

Increases in human capital (education, training, experience)

Improved organization and management of production (e.g., just-in-time systems)

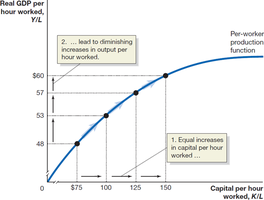

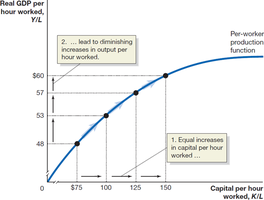

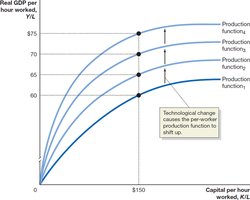

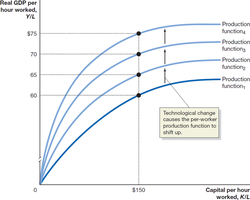

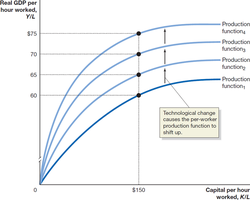

The Per-Worker Production Function

The per-worker production function shows the relationship between real GDP per hour worked and capital per hour worked, holding technology constant. The function exhibits diminishing returns: as capital increases, the additional output from each new unit of capital decreases.

The Role of Technological Change

Technological change shifts the per-worker production function upward, allowing more output per hour worked for any given amount of capital.

Unlike capital accumulation, technological change does not suffer from diminishing returns in the long run.

Case Study: The Soviet Union

The Soviet Union focused on increasing capital but lacked incentives for technological innovation, leading to slower long-term growth.

New Growth Theory

Developed by Paul Romer, this theory emphasizes that technological change results from economic incentives and market forces.

Knowledge capital (ideas, research, and development) is a public good—nonrival and nonexcludable—leading to increasing returns at the economy level.

Government’s Role in Fostering Growth

Protecting intellectual property (patents, copyrights)

Subsidizing research and development (R&D)

Subsidizing education

Creative Destruction

Joseph Schumpeter described economic growth as a process of creative destruction, where new products and technologies replace old ones, driving progress but also causing some firms to fail.

Entrepreneurs play a central role in this process by innovating and combining resources in new ways.

Economic Growth in the United States

Trends in U.S. Productivity Growth

Growth rates were modest before 1900, increased in the 20th century due to R&D, and fluctuated after the 1970s.

Information technology has been a major driver of productivity since the 1990s.

Debate exists over whether the U.S. is entering a period of slow growth (secular stagnation) or will return to faster growth.

Measurement Issues

Service output is harder to measure than goods output, possibly understating productivity growth.

Technological advances may increase consumer surplus not captured in GDP statistics.

Why Isn’t the Whole World Rich?

The Catch-Up Hypothesis

The economic growth model predicts that poorer countries should grow faster than richer ones, leading to convergence in living standards.

This is called catch-up or convergence.

Barriers to Catch-Up

Not all countries experience rapid growth due to:

Weak institutions (poor rule of law, corruption)

Wars and revolutions

Poor public education and health

Low rates of saving and investment

The Role of Globalization

Globalization—greater openness to trade and investment—has helped many countries grow faster.

Foreign direct investment (FDI) and foreign portfolio investment can supplement domestic investment and spur growth.

Growth Policies

Policies to Foster Economic Growth

Enhancing property rights and the rule of law

Improving health and education

Promoting technological change (including encouraging FDI)

Promoting savings and investment (e.g., through tax incentives)

Challenges for Developing Countries

Developing countries often face brain drain, where skilled workers emigrate to high-income countries.

Improved governance, political stability, and absence of violence are essential for sustained growth.

Debate: Is Economic Growth Always Good?

While growth is clearly beneficial for low-income countries, some argue that further growth in high-income countries may have negative effects (e.g., environmental harm, resource depletion, cultural loss).

These are normative debates, and economic analysis can inform but not resolve them.

Summary Table: Key Factors Affecting Economic Growth

Factor | Role in Growth | Policy Implications |

|---|---|---|

Capital Accumulation | Increases output per worker, but subject to diminishing returns | Encourage investment, savings, and efficient financial systems |

Technological Change | Shifts production function upward, not subject to diminishing returns | Support R&D, education, and intellectual property protection |

Institutions | Secure property rights, rule of law, and efficient markets | Reform legal systems, reduce corruption |

Globalization | Facilitates technology transfer and investment | Promote openness to trade and FDI |