Back

BackChapter 11: Long-Run Economic Growth—Sources and Policies

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Long-Run Economic Growth: Sources and Policies

Introduction

Long-run economic growth is a central topic in macroeconomics, focusing on the sustained increase in real GDP per capita and the factors that drive improvements in living standards. This chapter explores the historical trends, determinants, and policies that influence economic growth, as well as the challenges faced by different countries.

Economic Growth Over Time and Around the World

Defining Economic Growth

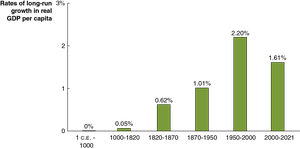

Economic growth refers to the increase in real GDP per capita over time, which is a key indicator of rising living standards. Most global economic growth has occurred in the last two centuries, largely due to technological advancements and industrialization.

Real GDP per capita: The value of goods and services produced per person, adjusted for inflation.

Growth rate calculation:

Global trends: The Industrial Revolution marked a turning point, leading to sustained increases in real GDP per capita.

The Industrial Revolution

The Industrial Revolution began in England around 1750, introducing mechanical power to production and enabling long-run economic growth. Prior to this, production relied on human and animal power, limiting output.

Key factors: Property rights, credible government, and independent courts incentivized investment and entrepreneurship.

Variation in Living Standards

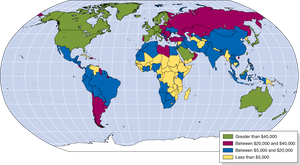

Differences in real GDP per capita are significant across countries, even after adjusting for cost-of-living. High-income countries have much higher living standards than developing countries.

Newly industrializing countries: Examples include Singapore, South Korea, and Taiwan.

Health and education: Improvements in these areas can raise living standards even without significant income growth.

What Determines How Fast Economies Grow?

Economic Growth Model

The economic growth model explains long-run growth rates in real GDP per capita, focusing on labor productivity, capital, and technology.

Labor productivity: Quantity of goods and services produced by one worker or one hour of work.

Key factors: Quantity of capital per hour worked and level of technology.

Technological change: Positive or negative change in a firm’s ability to produce output with given inputs.

Sources of Technological Change

Better machinery and equipment: Innovations like steam engines, computers, and electric generators.

Increases in human capital: Accumulated knowledge and skills from education and training.

Better organization and management: Examples include just-in-time production systems.

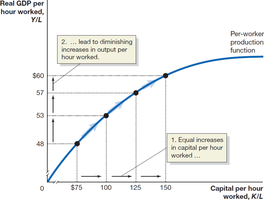

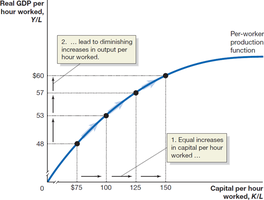

The Per-Worker Production Function

The per-worker production function shows the relationship between real GDP per hour worked and capital per hour worked, holding technology constant. Initial increases in capital are highly effective, but subsequent increases yield diminishing returns.

Diminishing returns: Each additional unit of capital adds less to output than the previous unit.

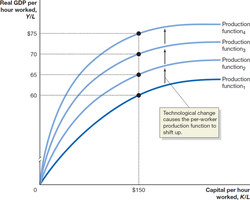

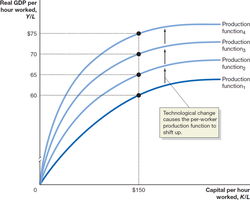

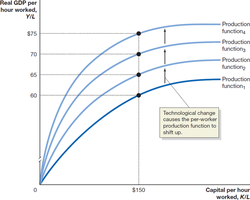

Technological Change and Output

Technological change shifts the production function upward, allowing higher output per hour worked without increasing capital. This is especially important for countries with already high capital stocks.

Example: Improved pizza ovens or assembly-line production increase productivity.

New Growth Theory

Solow and Romer Models

Robert Solow’s model attributes technological change to chance discoveries, while Paul Romer’s new growth theory emphasizes economic incentives and the accumulation of knowledge capital.

Knowledge capital: Nonrival and nonexcludable, leading to increasing returns at the economy level.

Physical capital: Rival and excludable, subject to diminishing returns.

Government’s Role

Protecting intellectual property: Patents and copyrights incentivize research and development.

Subsidizing R&D and education: Direct research, tax incentives, and education subsidies foster innovation and productivity.

Creative Destruction

Joseph Schumpeter’s model highlights the role of entrepreneurs in economic growth, where new products and technologies replace old ones, driving creative destruction.

Example: Automobiles replaced horse-drawn carriages, transforming industries.

Economic Growth in the United States

Productivity Growth Fluctuations

The United States has experienced varying growth rates in real GDP per hour worked, influenced by capital accumulation and technological change. Growth rates were high until the mid-1970s, then slowed, with a resurgence in the mid-1990s.

Measurement issues: Service output is harder to measure, potentially understating productivity growth.

Information technology: IT and AI have driven recent productivity improvements.

Secular stagnation: Some economists predict continued low growth due to demographic and investment trends.

Why Isn’t the Whole World Rich?

Economic Catch-Up

The economic growth model predicts that poor countries should grow faster than rich countries, due to greater benefits from additional capital and available technology. This is known as the catch-up hypothesis.

Catch-up: Poor countries' GDP per capita grows faster, converging with rich countries.

Barriers to Catch-Up

Weak institutions: Lack of rule of law and property rights discourages entrepreneurship.

Wars and revolutions: Instability hinders investment and growth.

Poor education and health: Low productivity results from inadequate public services.

Low savings and investment: Undeveloped financial systems perpetuate low growth.

Globalization

Globalization, or increased openness to trade and investment, has helped many countries escape the cycle of low savings and investment.

Foreign direct investment (FDI): Firms build or purchase facilities abroad.

Foreign portfolio investment: Individuals or firms buy foreign stocks or bonds.

Growth Policies

Government Policies for Growth

Effective policies to foster economic growth include enhancing property rights, improving health and education, promoting technological change, and encouraging savings and investment.

Property rights and rule of law: Independent courts and reduced corruption are essential.

Health and education: Investments yield increasing returns and prevent brain drain.

Technological change: Encouraged through FDI and R&D subsidies.

Savings and investment: Tax incentives and secure financial systems promote capital formation.

Debate on Economic Growth

While economic growth is generally seen as beneficial, especially for low-income countries, some argue that further growth in high-income countries may have negative effects, such as environmental degradation and cultural loss. Economic analysis can inform but not resolve these normative debates.

Summary Table: Key Factors Affecting Economic Growth

Factor | Effect on Growth | Example/Application |

|---|---|---|

Capital Accumulation | Increases productivity, but subject to diminishing returns | Investment in machinery, infrastructure |

Technological Change | Shifts production function upward, increases output | IT, AI, process innovations |

Human Capital | Improves labor productivity | Education, training |

Institutions | Secure property rights, rule of law encourage investment | Independent courts, anti-corruption reforms |

Globalization | Facilitates capital inflows, technology transfer | FDI, trade openness |