Back

BackChapter 14: Monetary Policy – Objectives, Instruments, and Transmission

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Monetary Policy Objectives

The Fed’s Dual Mandate

The Federal Reserve (the Fed) is the central bank of the United States, and its monetary policy objectives are defined by the Federal Reserve Act. The Fed’s dual mandate consists of two primary goals:

Stable Prices: Maintaining low and stable inflation.

Full Employment: Achieving the highest level of employment possible without causing inflation.

To achieve these goals, the Fed uses various measures and frameworks to monitor economic conditions and guide its policy decisions.

Operational “Stable Prices” Goal

The Fed monitors inflation using two main indices:

Consumer Price Index (CPI)

Personal Consumption Expenditure Price Index (PCEPI)

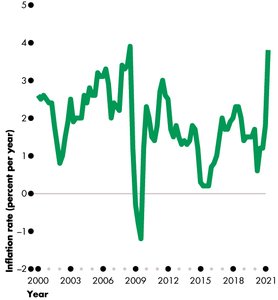

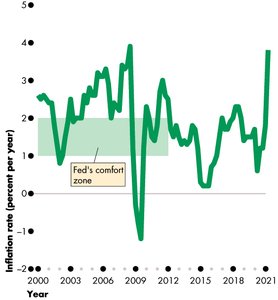

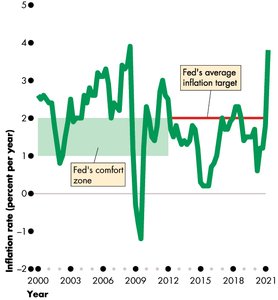

The Fed’s operational guide is the core PCEPI, which excludes volatile food and fuel prices. The core inflation rate is the rate of increase in the core PCEPI and is considered less volatile than the CPI inflation rate, providing a better measure of underlying inflation trends.

Trends in Core Inflation: Before 2012, the Fed’s comfort zone for inflation was between 1% and 2% per year. Since 2012, the Fed has targeted an average inflation rate of 2%.

Operational “Maximum Employment” Goal

The Fed also monitors the business cycle by tracking the output gap—the difference between real GDP and potential GDP, expressed as a percentage. A positive output gap (inflationary gap) signals rising inflation, while a negative output gap (recessionary gap) indicates unemployment above the natural rate. The Fed aims to minimize the output gap to maintain economic stability.

Monetary Policy Instruments

The Monetary Policy Instrument

The Fed uses instruments it can directly control or closely target. These include:

Quantity of Bank Reserves: The sum of vault cash held by banks and their reserve balances at the Fed.

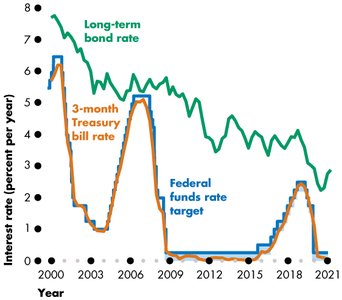

Short-Term Interest Rates: The Fed can set or influence three key rates:

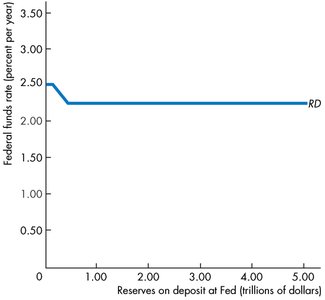

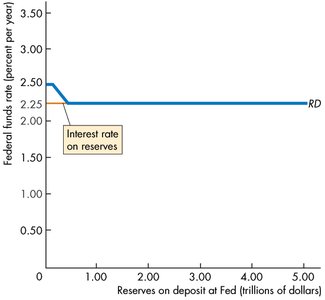

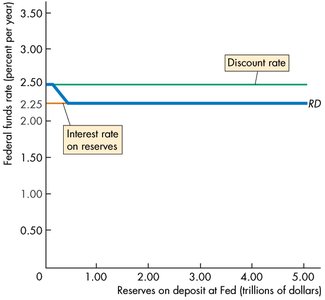

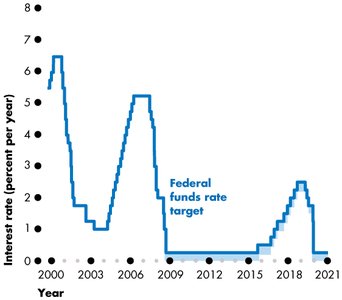

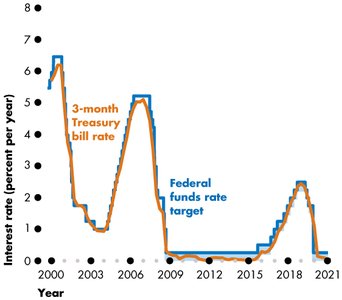

Federal Funds Rate: The interest rate on overnight loans of reserves among banks. The FOMC sets a target range for this rate.

Discount Rate: The rate at which the Fed lends to banks.

Interest on Reserves Rate: The rate the Fed pays banks on reserves held at the Fed.

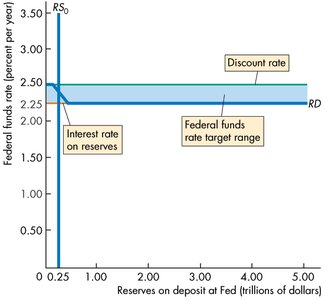

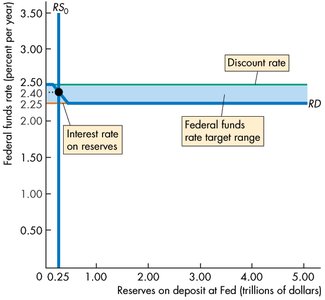

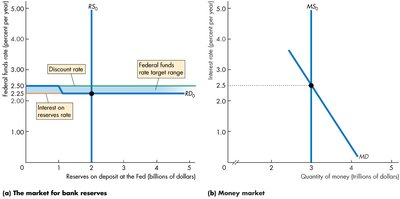

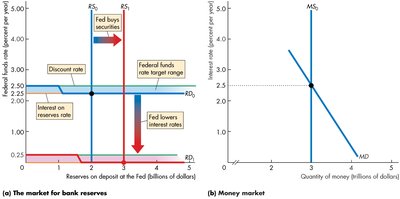

The Fed conducts open market operations to change the quantity of reserves:

Open Market Purchase: The Fed buys U.S. Treasury securities, increasing reserves (sometimes called "Quantitative Easing" if large).

Open Market Sale: The Fed sells U.S. Treasury securities, decreasing reserves (sometimes called "Quantitative Tightening" if large).

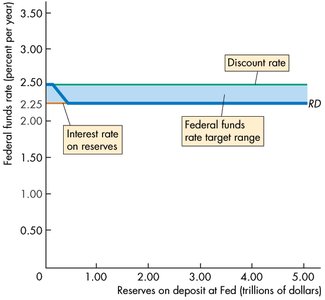

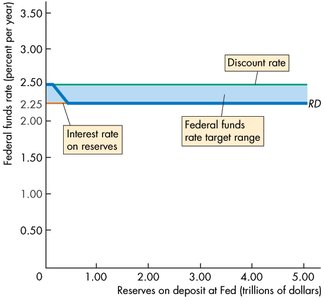

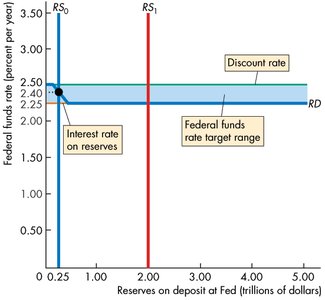

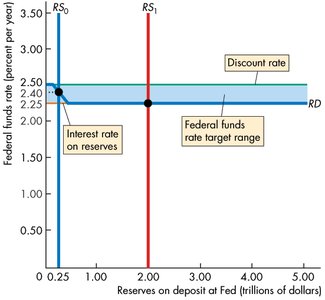

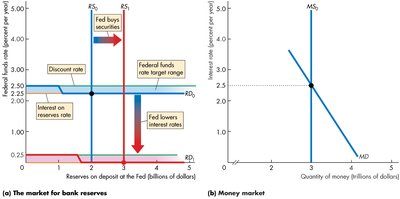

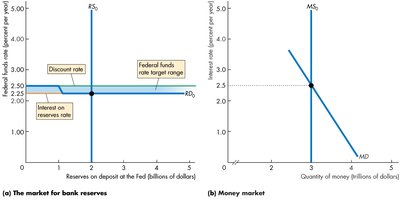

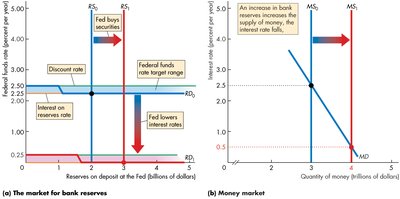

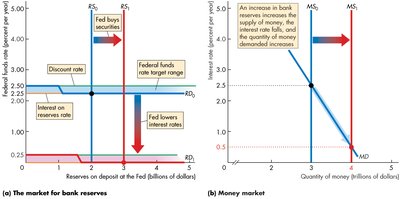

The Corridor System

The Fed uses a corridor system to manage the federal funds rate. The corridor is defined by the discount rate (upper bound) and the interest on reserves rate (lower bound). The federal funds rate typically moves within this corridor, and the Fed uses open market operations to adjust the supply of reserves and hit its target rate.

In normal times, the Fed sets the federal funds rate at the center of the corridor by adjusting the supply of reserves. Recently, the target has sometimes been at the bottom of the corridor, requiring the Fed to increase the supply of reserves.

Monetary Policy Transmission

How Monetary Policy Affects the Economy

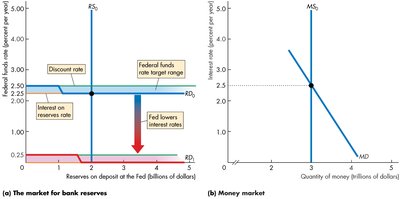

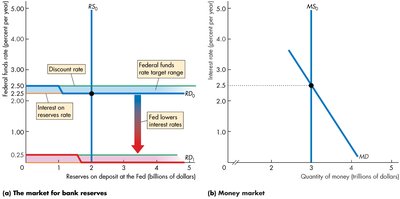

When the Fed lowers the discount rate, the interest rate on reserves, or the federal funds rate, it typically buys securities in the open market. This process is known as monetary policy transmission and involves several steps:

Other short-term interest rates fall.

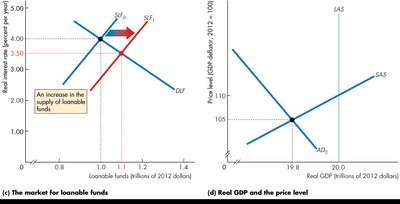

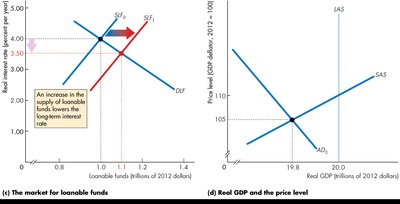

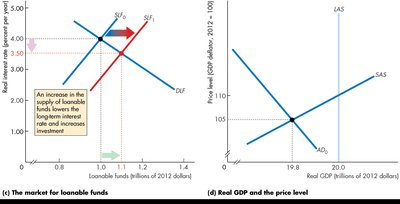

The Fed engages in quantitative easing (open market purchase), increasing reserves and the supply of loanable funds.

The long-term real interest rate falls.

Consumption expenditure, investment, and net exports increase.

Aggregate demand increases.

Real GDP growth and the inflation rate increase.

Money and Bank Loans

An increase in bank reserves increases the supply of money, causing short-term interest rates to fall. This, in turn, increases the quantity of money and bank loans available in the economy.

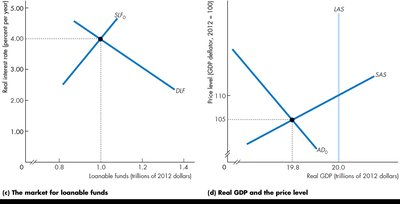

The Long-Term Real Interest Rate and Loanable Funds

The equilibrium in the market for loanable funds determines the long-term real interest rate, which is calculated as:

A lower real interest rate encourages investment and increases aggregate planned expenditure, moving real GDP toward potential GDP.

Aggregate Expenditure and Real GDP

Changes in the federal funds rate ripple through the economy, affecting three components of aggregate expenditure:

Consumption expenditure

Investment

Net exports

As these components increase, aggregate demand rises, leading to higher real GDP and inflation.

Monetary Policy in Reverse: Fighting Inflation

When inflation is too high and the output gap is positive, the Fed raises the federal funds rate target, sells securities in the open market, and the process works in reverse:

Reserves decrease, reducing the supply of money.

Short-term interest rates rise.

The supply of loanable funds decreases, raising the real interest rate and reducing investment.

Aggregate planned expenditure and real GDP decrease, closing the inflationary gap.

Loose Links and Long and Variable Lags

The transmission of monetary policy is complex and subject to long and variable lags. Long-term interest rates, which influence spending plans, are only loosely linked to the federal funds rate. The response of expenditure plans to changes in the real interest rate depends on many unpredictable factors.

Policy Strategies and Clarity

Inflation Rate Targeting

Inflation rate targeting is a strategy where the central bank publicly commits to achieving an explicit inflation target and explains how its policy actions will achieve that target. This approach, used by several central banks since the mid-1990s, helps avoid serious inflation and persistent deflation.

Taylor Rule

The Taylor rule is a formula for setting the federal funds rate based on the inflation rate and the output gap:

Where:

FFR: Federal funds rate

INF: Inflation rate

GAP: Output gap (all in percentages)

The Taylor rule provides a systematic way to adjust monetary policy in response to changing economic conditions.