Back

BackChapter 8: Money, the Banking System, and the Money Market

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

What is Money?

Functions and Characteristics of Money

Money is any commodity or token that is generally accepted as a means of payment. It serves as a method for settling debts and facilitating transactions in an economy. Money fulfills three primary functions:

Medium of Exchange: An object accepted in exchange for goods and services, eliminating the inefficiencies of barter, which requires a double coincidence of wants.

Unit of Account: An agreed measure for stating the prices of goods and services, allowing for consistent valuation and comparison.

Store of Value: Money can be held and used for future transactions, retaining value over time.

In the United States, money consists of currency (notes and coins held by households and firms) and deposits at banks and other depository institutions, both of which can be used to make payments.

Official Measures of Money

M1: Currency and deposits available on demand (most liquid form).

M2: M1 plus small-denomination time deposits and retail money market mutual funds (less liquid than M1).

Liquidity refers to how easily an asset can be converted into a means of payment with little loss of value.

The Banking System

Structure and Roles

The banking system comprises private and public institutions that create money and manage the nation’s monetary and payments systems. Key components include:

Depository Institutions: Commercial banks, thrift institutions (e.g., savings & loan, credit unions), and money market mutual funds.

Central Bank (Federal Reserve System): The public authority that regulates depository institutions and conducts monetary policy.

Depository institutions allocate depositors’ funds into three types of assets:

Cash Assets: Notes, coins, and reserves at the Fed, plus loans to other banks.

Securities: U.S. Treasury bills, government bonds, and other securities.

Loans: Commitments of fixed amounts of money for agreed-upon periods.

The Federal Reserve System (The Fed)

Acts as banker to banks and the government.

Lender of last resort.

Sole issuer of bank notes.

Regulates depository institutions and conducts monetary policy to control the money supply and influence interest rates.

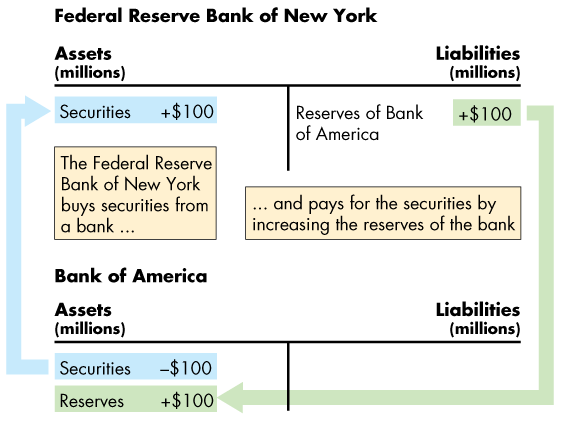

Monetary Base and Open Market Operations

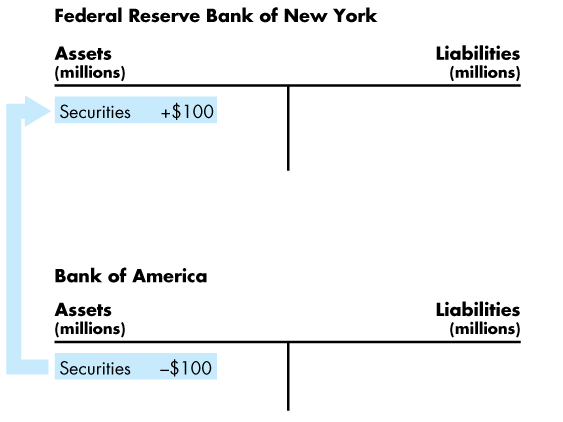

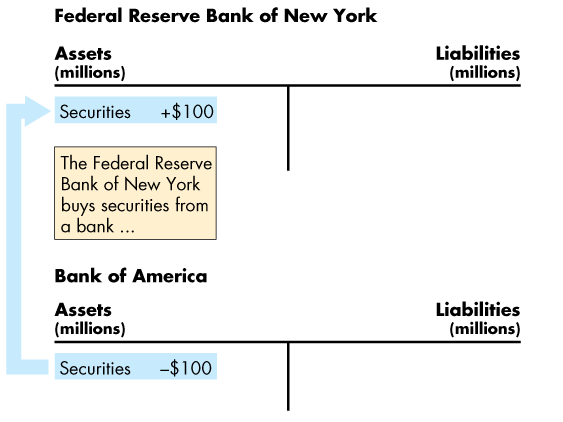

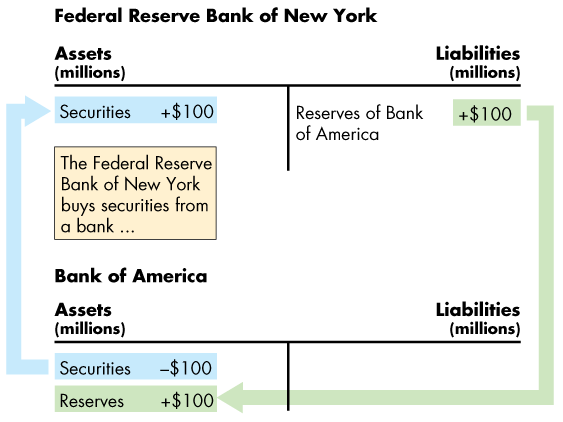

The monetary base is the sum of currency and reserves of depository institutions at the Fed. The Fed changes the monetary base through open market operations—the purchase or sale of securities in the open market.

Open Market Purchase: The Fed buys securities, paying with newly created reserves, increasing bank reserves.

Open Market Sale: The Fed sells securities, paid for with bank reserves, decreasing bank reserves.

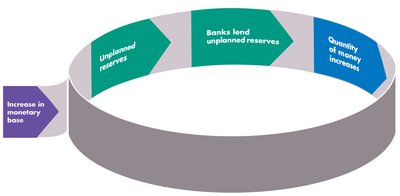

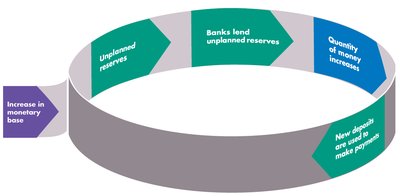

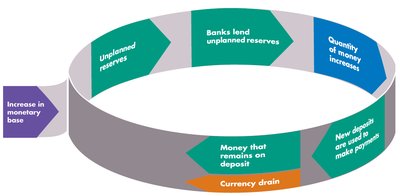

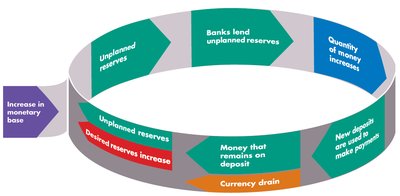

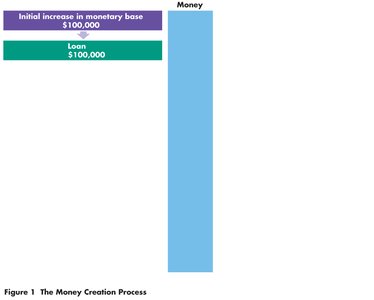

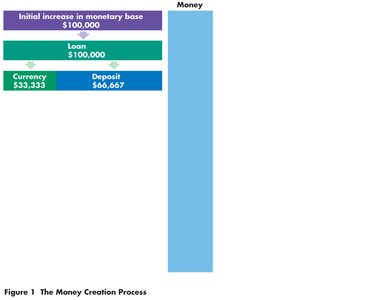

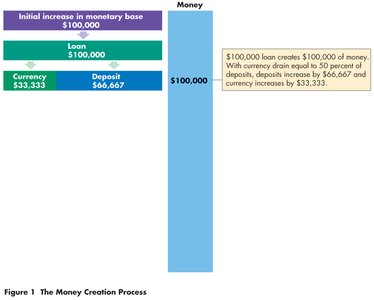

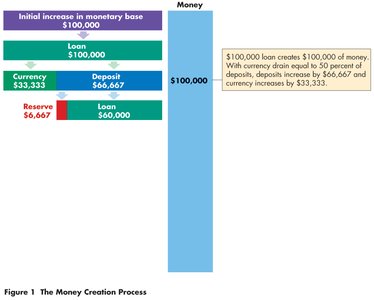

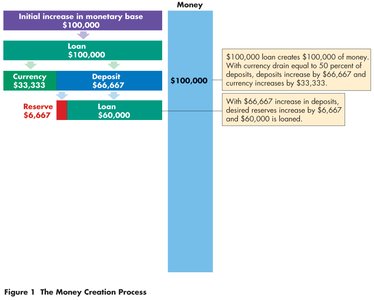

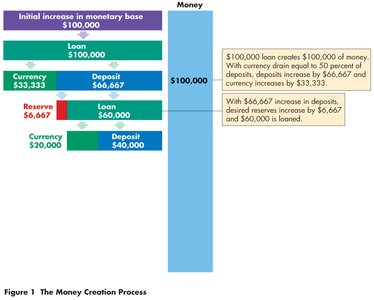

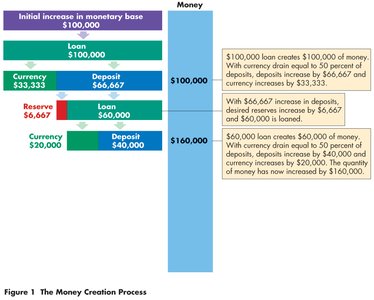

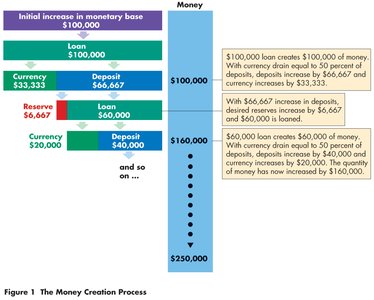

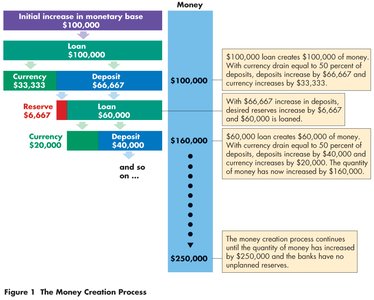

How Banks Create Money (Money Multiplier)

Deposit Creation and Constraints

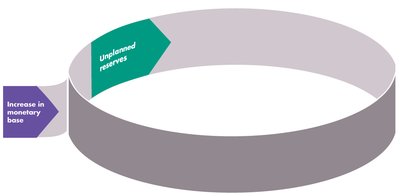

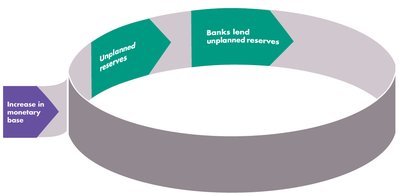

Banks create money by making loans, which generate new deposits. The amount of deposits banks can create is limited by:

The monetary base

Desired reserves (the reserve ratio banks wish to maintain)

Desired currency holding (the currency drain ratio)

The reserve ratio is the fraction of deposits held as reserves. The desired reserve ratio is set by banks, while unplanned reserves are actual reserves minus desired reserves. The currency drain ratio is the ratio of currency to deposits held by the public.

The Money Multiplier

When the monetary base increases, the quantity of money increases by more than the initial increase due to the money multiplier effect. The money multiplier is defined as:

where is the currency drain ratio and is the desired reserve ratio.

For example, if and :

Money Creation Process

The process of money creation involves a cycle of lending, deposit creation, and reserve management, continuing until all unplanned reserves are eliminated.

The Market for Money

Determinants of Money Holding

The quantity of money people plan to hold depends on:

The nominal interest rate (opportunity cost of holding money)

The price level (affects nominal but not real money demand)

Real GDP (higher GDP increases money demand)

Financial innovation (can reduce money demand by making it easier to switch to interest-bearing assets)

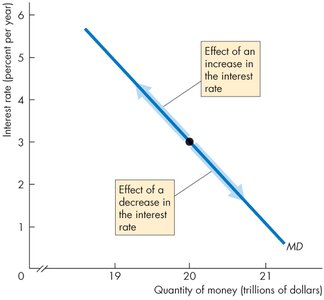

Demand for Money

The demand for money is the relationship between the quantity of real money demanded and the nominal interest rate, all else equal. There is an inverse relationship: as the interest rate rises, the quantity of money demanded falls.

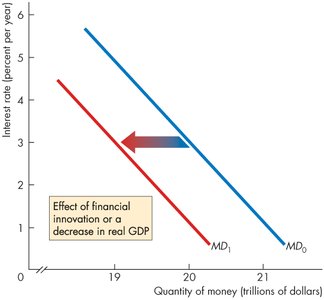

Shifts in the Demand for Money

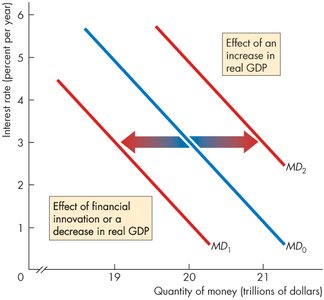

Factors such as changes in real GDP or financial innovation can shift the demand for money curve:

A decrease in real GDP or financial innovation shifts the demand curve leftward.

An increase in real GDP shifts the demand curve rightward.

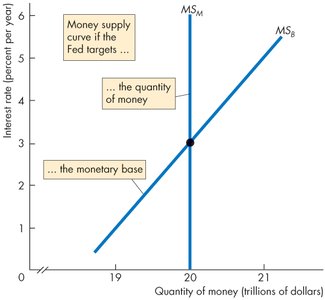

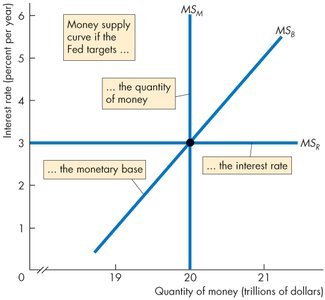

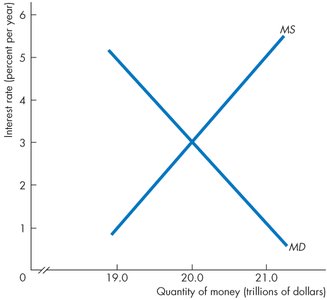

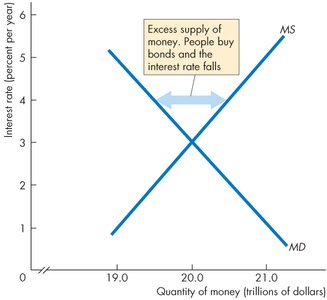

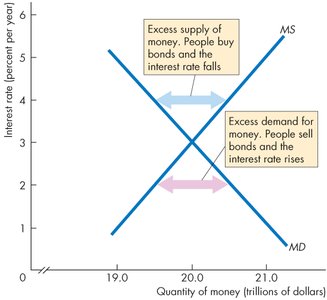

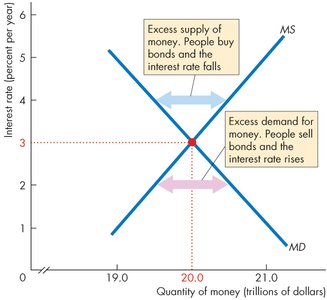

Money Market Equilibrium

Equilibrium in the money market occurs when the quantity of money demanded equals the quantity supplied. The adjustment process differs in the short run and long run, depending on the Fed’s monetary policy regime.

The Quantity Theory of Money

Long-Run Relationship Between Money and Prices

The quantity theory of money states that, in the long run, an increase in the quantity of money leads to an equal percentage increase in the price level. This theory is based on the velocity of circulation and the equation of exchange:

where is velocity, is the price level, is real GDP, and is the quantity of money. The equation of exchange is:

If does not influence or , then changes in directly affect in the long run.

Growth Rate Formulation

Expressing the equation of exchange in growth rates:

Rearranged:

In the long run, the rate of velocity change is approximately zero, so: