Back

BackCountercyclical Macroeconomic Policy: Concepts, Tools, and Applications

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Countercyclical Macroeconomic Policy

The Role of Countercyclical Policies in Economic Fluctuations

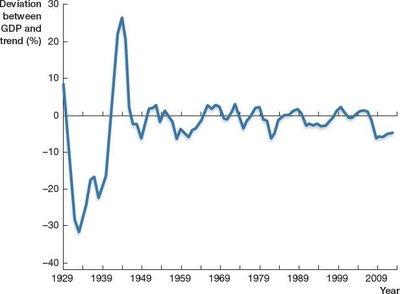

Countercyclical policies are designed to reduce the intensity of economic fluctuations, smoothing the growth rates of employment, GDP, and prices. These policies are implemented to address the short-run ups and downs of the business cycle, including recessions and expansions.

Expansionary policy aims to reduce the severity of recessions by shifting labor demand to the right and increasing economic activity (GDP). It is intended to "heat up" the economy.

Contractionary policy is used to slow down the economy when it grows too fast, or "overheats," often to control inflation or prevent unsustainable booms.

Policymakers may use contractionary policy to reduce inflation by slowing the growth rate of the money supply or to preemptively cool off the economy to avoid extreme contractions.

Additional info: The graph above illustrates the deviation of U.S. real GDP from its trend line, highlighting periods of recession and expansion.

Countercyclical Monetary Policy

Tools and Transmission Mechanism

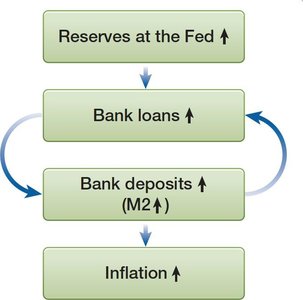

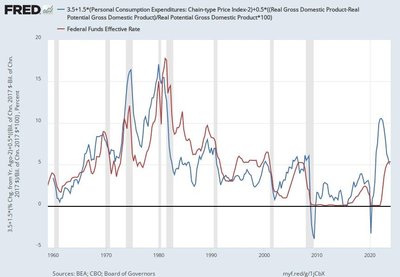

Countercyclical monetary policy is conducted by the central bank (the Federal Reserve in the U.S.). The primary tool is the control of the federal funds rate, which influences market interest rates and overall financial conditions, ultimately affecting employment and inflation.

The Federal Open Market Committee (FOMC) sets the target range for the federal funds rate.

The Fed influences this rate through Interest on Reserve Balances and Open Market Operations.

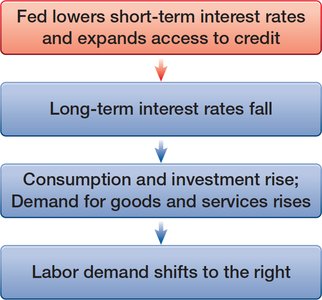

Expansionary monetary policy lowers short-term interest rates to stimulate economic activity, while contractionary policy raises rates to slow the economy.

Additional info: The diagram shows how changes in the policy rate affect market conditions, spending decisions, and progress toward maximum employment and stable prices.

Expansionary Monetary Policy

Lowering the federal funds rate reduces other interest rates, encouraging borrowing and investment.

This increases demand for goods and services, shifting labor demand to the right and raising output and employment.

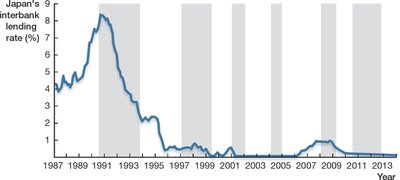

Zero Lower Bound and Liquidity Trap

When the policy rate approaches zero, traditional monetary policy becomes less effective—a situation known as the "liquidity trap." Japan experienced this from 1990 to 2010, with near-zero interest rates and persistent deflation.

Expected real interest rate = Nominal interest rate – Expected inflation rate

When inflation is negative (deflation), even a zero nominal rate can result in a positive real rate, discouraging investment.

Lender of Last Resort and Quantitative Easing

The central bank can act as a lender of last resort during financial crises, providing liquidity to banks to prevent panic.

Quantitative easing involves the Fed buying long-term bonds, increasing reserves and lowering long-term interest rates, which stimulates investment and spending.

The Taylor Rule

The Taylor Rule provides a guideline for setting the federal funds rate based on inflation and the output gap:

where

The rule suggests raising the federal funds rate by 1.5 percentage points for each 1% increase in inflation, and by 0.5 percentage points for each 1% increase in the output gap.

Countercyclical Fiscal Policy

Types and Mechanisms

Countercyclical fiscal policy is enacted by the legislative and executive branches of government. It involves changes in government expenditures and taxes to influence the growth rate of real GDP.

Expansionary fiscal policy increases government spending and/or reduces taxes to stimulate economic growth.

Contractionary fiscal policy decreases government spending and/or increases taxes to slow economic growth.

Automatic stabilizers (e.g., tax system, unemployment insurance) automatically offset economic fluctuations without new legislation.

Discretionary fiscal policy involves deliberate actions, such as the American Recovery and Reinvestment Act (2009) and the CARES Act (2020).

Government Expenditure Multiplier

The government expenditure multiplier measures the change in GDP resulting from a $1 change in government expenditures:

Multiplier values can range from below 1 (due to crowding out) to as high as 3 (in deep recessions).

Crowding out occurs when increased government spending raises interest rates, reducing private investment.

Government Taxation Multiplier

The government taxation multiplier measures the change in GDP resulting from a $1 decrease in taxes:

Multiplier values depend on consumption levels and expectations of future taxes (Ricardian Equivalence).

Policy Effectiveness and Limitations

The effectiveness of fiscal policy depends on the state of the economy, the size of the multiplier, and the presence of policy lags or waste.

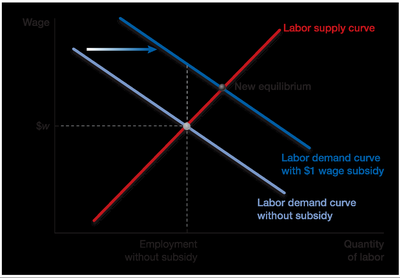

Fiscal policies targeted at the labor market include unemployment insurance and wage subsidies.

Policies That Blur the Line Between Fiscal and Monetary Policy

Some policies combine elements of both fiscal and monetary policy. Examples include the Troubled Asset Relief Program (TARP) and Federal Reserve lending facilities during crises, which provide credit to stabilize financial markets and support economic activity.

Key Ideas

Countercyclical policies aim to smooth economic fluctuations and stabilize employment, GDP, and prices.

Monetary policy manipulates bank reserves and interest rates; fiscal policy adjusts government spending and taxes.

Expansionary policies stimulate the economy; contractionary policies slow it down to control inflation or prevent overheating.