Back

BackCredit Markets and Financial Intermediation: Study Notes for Macroeconomics

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Credit Markets and Financial Intermediation

Introduction to Credit Markets

The credit market is a fundamental component of the macroeconomy, matching borrowers (demanders of credit) with savers (suppliers of credit). It determines the real interest rate, which is crucial for investment, consumption, and overall economic activity.

Debtors (Borrowers): Economic agents such as entrepreneurs, businesses, home buyers, and students who borrow funds.

Credit: The amount of loans that the debtor receives.

Interest Rate: The additional payment, above and beyond the principal, that a borrower makes on a loan.

Nominal and Real Interest Rates

Interest rates can be measured in nominal or real terms. The nominal interest rate is the annual cost of a loan without adjusting for inflation, while the real interest rate adjusts for changes in the price level.

Nominal Interest Rate (i): The stated annual cost of borrowing.

Real Interest Rate (r): The inflation-adjusted cost of borrowing, calculated as:

$ r = i - \pi $ where $i$ is the nominal interest rate and $\pi$ is the inflation rate.

Example: If you borrow $20,000 at a 5% nominal interest rate and inflation is 2%, the real interest rate is 3% and the total interest payment is $1,000.

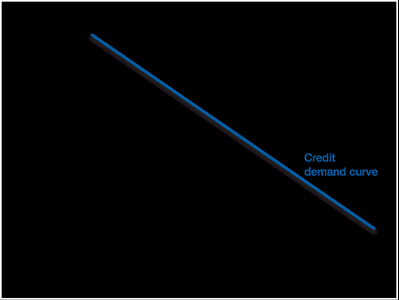

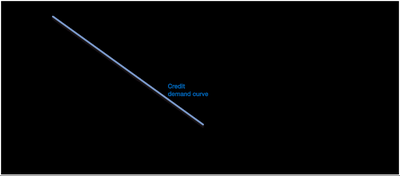

Credit Demand

The quantity of credit demanded is the amount of loans borrowers are willing to take at a given real interest rate. The credit demand curve shows the relationship between the real interest rate and the quantity of credit demanded.

Credit Demand Schedule: A table showing quantities demanded at various real interest rates.

Credit Demand Curve: A downward-sloping curve because higher real interest rates increase the cost of borrowing, reducing demand.

Steepness: Indicates sensitivity of borrowers to interest rate changes. A steep curve means demand is less sensitive; a flat curve means more sensitive.

Shifts in the Credit Demand Curve

The credit demand curve shifts due to changes in business opportunities, household preferences, or government policy.

Rightward Shift: More capital investment by firms, optimistic households, or increased government borrowing.

Leftward Shift: Households become cautious, government reduces deficit, or fewer business opportunities.

Credit Supply

The quantity of credit supplied is the amount of funds that savers are willing to lend at a given real interest rate. The credit supply curve shows the relationship between the real interest rate and the quantity of credit supplied.

Credit Supply Schedule: A table showing quantities supplied at various real interest rates.

Credit Supply Curve: An upward-sloping curve because higher real interest rates provide greater incentive to save.

Motives for Saving: Retirement, bequests, large purchases, starting a business, precautionary savings.

Shifts in the Credit Supply Curve

The credit supply curve shifts due to changes in household or firm saving motives.

Rightward Shift: Households save more, firms retain more earnings.

Leftward Shift: Households spend more, less precautionary saving.

Credit Market Equilibrium

The equilibrium in the credit market is where the credit supply and demand curves intersect, determining the equilibrium real interest rate ($r^*$) and quantity of credit ($Q^*$).

Effect of Government Deficit: An increase in government borrowing shifts the demand curve right, raising the real interest rate and quantity of credit.

Role of Credit Markets in Resource Allocation

Credit markets improve resource allocation by enabling savers to lend to borrowers, facilitating investment and economic growth. Without credit markets, savings would earn lower returns and investment would be limited.

Banks and Financial Intermediation

Financial Intermediaries

Banks and other financial institutions channel funds from savers to borrowers, playing a critical role in the credit market.

Types of Institutions: Banks, asset management companies, hedge funds, private equity, venture capital, shadow banking system.

Bank Balance Sheets

A bank's balance sheet records its assets and liabilities.

Assets: Bank reserves, cash equivalents, long-term investments.

Liabilities: Demand deposits, short-term borrowing, long-term debt, stockholders' equity.

Equation: $ \text{Total Assets} = \text{Total Liabilities} + \text{Stockholders' Equity} $

Functions of Banks

Banks perform three main functions as financial intermediaries:

Identify Profitable Lending Opportunities: Attracting borrowers and selecting the best loan applications.

Maturity Transformation: Transforming short-term liabilities (deposits) into long-term investments (loans).

Risk Management: Diversifying assets and transferring risk to stockholders and, ultimately, the government (via FDIC insurance).

Bank Risk and Insolvency

Banks face risks due to maturity transformation and asset illiquidity. If asset values fall below liabilities, banks become insolvent.

FDIC Insurance: Protects depositors up to $250,000 per account.

Bank Runs: Occur when many depositors withdraw funds simultaneously, forcing banks to sell assets at a loss.

Bank Failures in U.S. History

There have been four major waves of bank failures in the U.S., often associated with economic crises. The regulation of Systemically Important Financial Institutions (SIFIs) aims to reduce systemic risk.

Wave | Period | Number of Failures | Notes |

|---|---|---|---|

1 | 1919–1928 | 6,000 | Mainly rural banks |

2 | 1929–1939 | 9,000 | Great Depression |

3 | 1986–1995 | 3,000 | Savings & loan crisis |

4 | 2007–2009 | Several major institutions | Financial crisis |

Key Ideas

The credit market matches borrowers and savers, determining the real interest rate.

Banks and financial intermediaries identify lending opportunities, transform maturities, and manage risk.

Banks become insolvent when liabilities exceed assets, with depositors protected by FDIC insurance.