Back

BackEconomic Growth and Development: Key Concepts and Theories

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Economic Growth & Development

Defining Economic Growth

Economic growth refers to the increase in per capita real GDP, typically measured by its rate of change per year. This concept is central to understanding how economies expand and improve living standards over time.

Per Capita Real GDP: The total value of goods and services produced in a country, adjusted for inflation, divided by the population.

Growth Rate: The annual percentage increase in real GDP per capita.

Rule of 72: The number of years required for a variable to double is approximately 72 divided by its annual growth rate.

Example: If a country's GDP grows at 4% per year, it will double in about 18 years ().

Historical Trends in Economic Growth

Examining historical data helps us understand the factors influencing economic growth and the impact of major events.

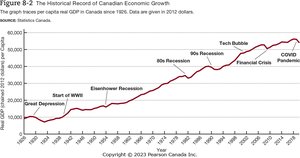

Canada's Economic Growth: Over the past century, Canada has experienced steady growth in per capita real GDP, with notable fluctuations during events such as the Great Depression, World War II, and recent recessions.

International Comparisons of Economic Growth

Countries differ significantly in their real GDP per capita and growth rates. Factors such as resource endowment, productivity, and institutional quality contribute to these differences.

High-Income Countries: Examples include Canada, the United States, and Germany, which have high real GDP per capita.

Developing Countries: Many nations in Africa, Asia, and Latin America have lower real GDP per capita but may experience higher growth rates as they catch up.

Determinants of Economic Growth

Economic growth can result from two main sources: an increase in resources or improvements in productivity.

More Resources: Expanding the labor force, capital stock, or natural resources.

Better Productivity: Enhancing the efficiency with which resources are used, often through technological progress or improved human capital.

Labor Productivity: Total domestic output (real GDP) divided by the number of workers or labor hours.

Measuring Economic Growth

Growth accounting decomposes GDP growth into contributions from labor, capital, and multifactor productivity (MFP).

Growth Accounting Equation:

Solow Residual: The portion of GDP growth not explained by labor or capital growth, attributed to technological progress.

Theories of Economic Growth

Several theories explain the sources and sustainability of economic growth:

Classical Growth Theory: Emphasizes the role of savings and capital accumulation. Saving is necessary for long-term growth, but excessive saving can reduce short-term demand (the paradox of thrift).

Neoclassical Growth Theory: Focuses on technology as an exogenous driver of growth. The aggregate production function is: where L is labor, K is capital, and H is human capital. Diminishing returns to labor and capital imply that long-term growth depends on technological progress.

New Growth Theory: Treats technology as an endogenous factor, influenced by incentives for research, innovation, and knowledge creation. Human capital and ideas are central to sustained growth.

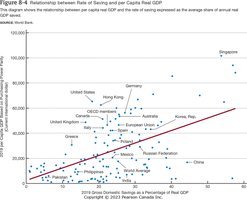

Savings and Economic Growth

The relationship between savings rates and per capita real GDP is crucial for understanding long-term growth prospects.

Net Borrowers vs. Net Lenders: Countries that save more can invest more, leading to higher future consumption.

Empirical Evidence: Higher savings rates are generally associated with higher per capita real GDP.

Role of Technology and Human Capital

Technological progress and human capital investment are key drivers of productivity and economic growth.

Research and Development (R&D): Innovation is encouraged by patents and intellectual property rights, which provide incentives for inventors.

Positive Externalities: R&D benefits not only the innovating country but also others through technology diffusion.

Human Capital: Education and training enhance labor productivity and foster innovation.

The Role of Government in Economic Growth

Governments can promote growth by ensuring macroeconomic stability, protecting property rights, and fostering competition and openness.

Credibility: Stable legal and political systems encourage investment.

Openness: Open economies benefit from larger markets, foreign investment, and technology transfer.

Efficient Public Spending: Effective use of public funds supports infrastructure, education, and health.

International Economic Development

Development economics focuses on the challenges faced by developing countries, including poverty, population growth, and the transition through different stages of economic development.

Poverty Rates: Vary widely across regions, with significant progress in some countries (e.g., China, India) and persistent challenges in others (e.g., Sub-Saharan Africa).

Population Growth: Historically, rapid population growth was seen as a barrier to development (Malthusian hypothesis), but technological advances have outpaced resource constraints.

Demographic Transition: As incomes rise, birth rates tend to fall due to higher opportunity costs, lower infant mortality, and reduced reliance on children for old-age support.

Stages of Economic Development: Economies typically progress from agricultural to manufacturing and then to service-based structures.

Summary Table: Key Growth Theories

Theory | Main Driver | Role of Technology | Policy Implications |

|---|---|---|---|

Classical | Savings & Capital | Exogenous | Encourage savings, limit deficits |

Neoclassical | Technology, Labor, Capital | Exogenous | Promote investment, education |

New Growth | Knowledge & Innovation | Endogenous | Support R&D, human capital |

Additional info: The notes above integrate foundational macroeconomic concepts from the provided materials and expand with academic context for clarity and completeness.