Back

BackEconomic Growth: Measurement, Sources, Theories, and Policy

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Economic Growth

Introduction to Economic Growth

Economic growth refers to the sustained expansion of a nation's production possibilities, measured as the increase in real GDP over a given period. Understanding economic growth is crucial for analyzing why some nations are rich while others remain poor, and for formulating policies to improve living standards.

9.1 The Basics of Economic Growth

Measuring Economic Growth

Economic Growth Rate: The annual percentage change in real GDP, indicating how quickly an economy is expanding.

Formula:

Example Calculation: If real GDP increases from trillion to trillion:

Growth of Real GDP Per Person

Real GDP per Person: Real GDP divided by the population; a key indicator of the standard of living.

Formula:

Growth Rate of Real GDP per Person:

Example: If real GDP per person rises from to :

Population Growth and Standard of Living

Population Growth Rate:

Relationship: Real GDP per person grows only if real GDP grows faster than the population.

Key Equation:

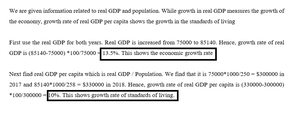

Table: Real GDP and Population Data

Year | Real GDP | Population | Real GDP per capita |

|---|---|---|---|

2017 | 75,000 | 250 | 300 |

2018 | 90,090 | 273 | 330 |

The Magic of Sustained Growth: The Rule of 70

Rule of 70: The number of years it takes for a variable to double is approximately $70$ divided by the annual percentage growth rate.

Formula:

Example: At a 3% growth rate, GDP doubles in about years; at 2%, it doubles in $35$ years.

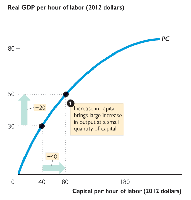

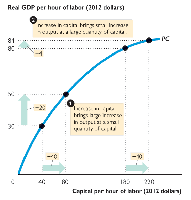

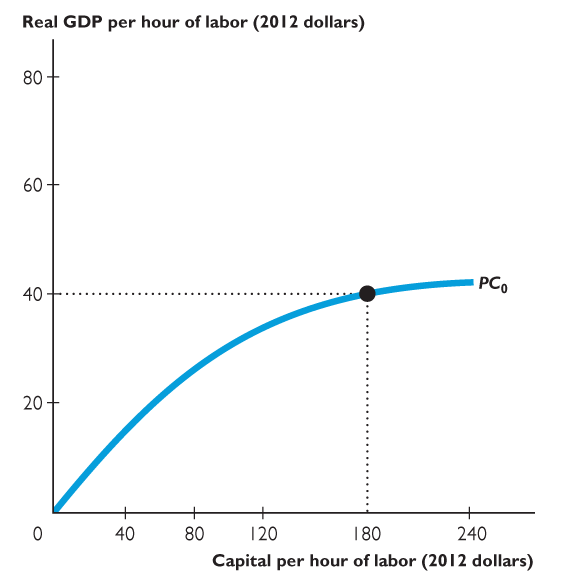

9.2 Labor Productivity Growth

Definition and Importance

Labor productivity is the quantity of real GDP produced by one hour of labor. Growth in labor productivity is the foundation for rising living standards.

Formula:

Example: If real GDP is billion and aggregate hours are $200\frac{8,000}{200} = 40$ dollars per hour.

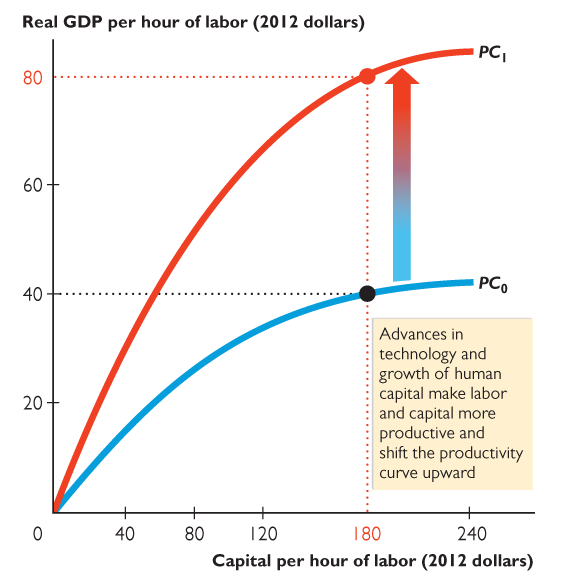

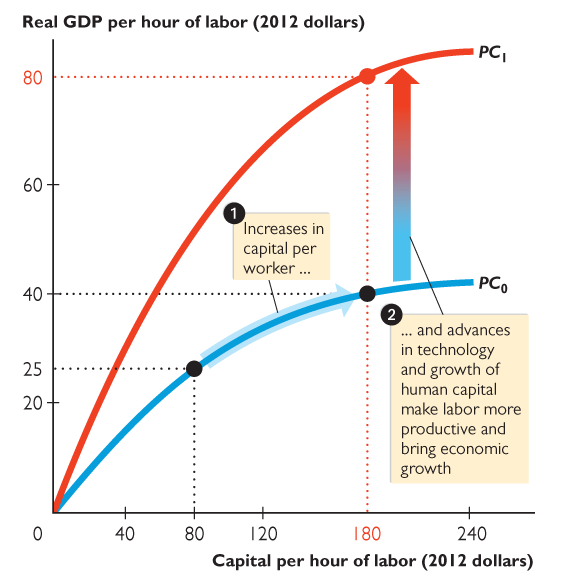

Sources of Labor Productivity Growth

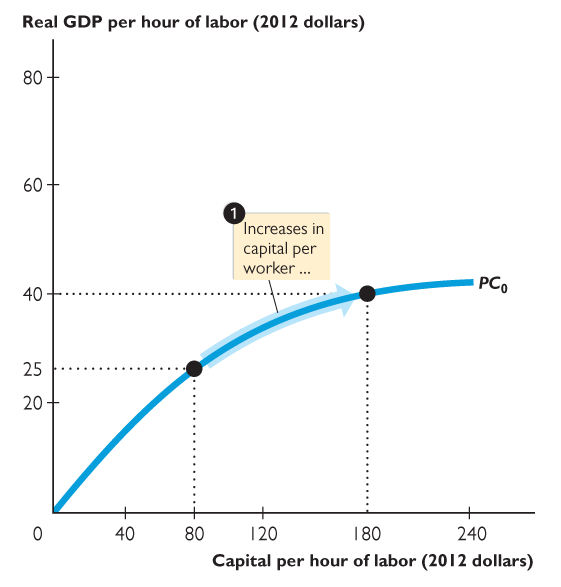

Physical Capital: Saving and investment increase capital per worker, raising productivity, but with diminishing returns.

Human Capital: Accumulated skills and knowledge from education, training, job experience, and health.

Technological Advances: New technologies and innovations that improve production methods.

Law of Diminishing Returns

As the quantity of capital increases, each additional unit of capital adds less to output than the previous unit.

Impact of Human Capital and Technology

Advances in technology and growth in human capital shift the productivity curve upward, allowing for higher output at the same level of capital.

Summary Table: Sources of Real GDP Growth

Source | Factors |

|---|---|

Quantity of Labor Growth | Population growth, labor force participation rate, average hours per worker |

Labor Productivity Growth | Physical capital growth, human capital growth, technological advances |

9.3 Economic Growth Theories: Old and New

Classical (Malthusian) Growth Theory

Key Idea: Population growth will eventually outpace resource growth, causing real GDP per person to fall back to subsistence levels.

Implication: Economic growth is temporary; prosperity leads to population growth, which erodes gains.

New Growth Theory

Key Idea: Human wants are unlimited, driving perpetual innovation and economic growth.

Mechanisms:

Human capital grows by choice (education, training).

Discoveries and innovations result from purposeful activity.

Competition erodes profits, incentivizing continual innovation.

Discoveries can be used by many people simultaneously.

Result: Continuous improvement in living standards.

Economic Growth and Income Distribution

Kuznets Hypothesis: Market forces in dynamic economies can reduce inequality as more low-income entrepreneurs succeed.

Krugman’s View: Policy changes (taxes, unions, wage controls) explain shifts in income distribution.

Piketty’s Theory: When the return on capital (r) exceeds the growth rate of the economy (g), wealth concentrates among the rich.

9.4 Achieving Faster Growth

Preconditions for Economic Growth

Economic Freedom: The ability to make personal choices, protection of private property, and free markets are essential for growth.

Property Rights: Secure property rights encourage investment and innovation.

Policies to Promote Growth

Create incentive mechanisms (protect property, reward innovation)

Encourage saving (to finance investment)

Support research and development (public funding for basic research)

Promote international trade (to maximize gains from specialization)

Improve education (raise human capital)

Limits of Policy

While governments cannot instantly increase growth rates, well-designed policies can nudge growth upward, yielding significant long-term benefits.

Why Are Some Nations Rich and Others Poor?

Key Factors

Political stability

Protection of property rights

Limited government intervention in markets

Sustained economic growth over decades

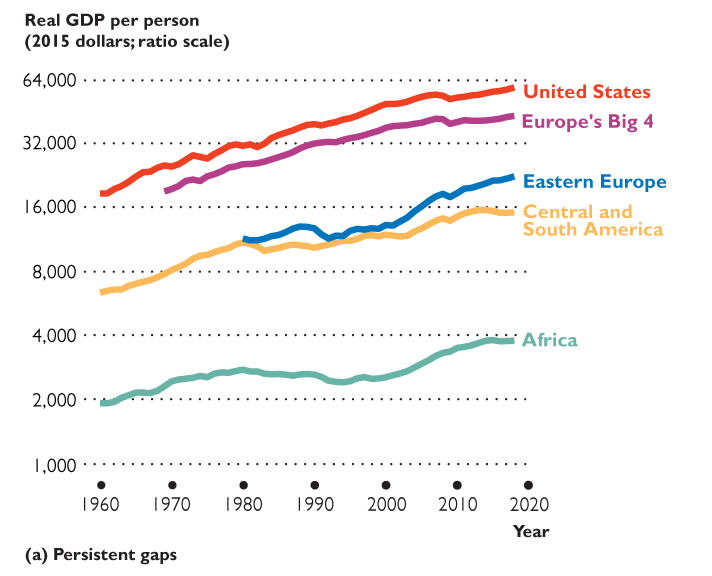

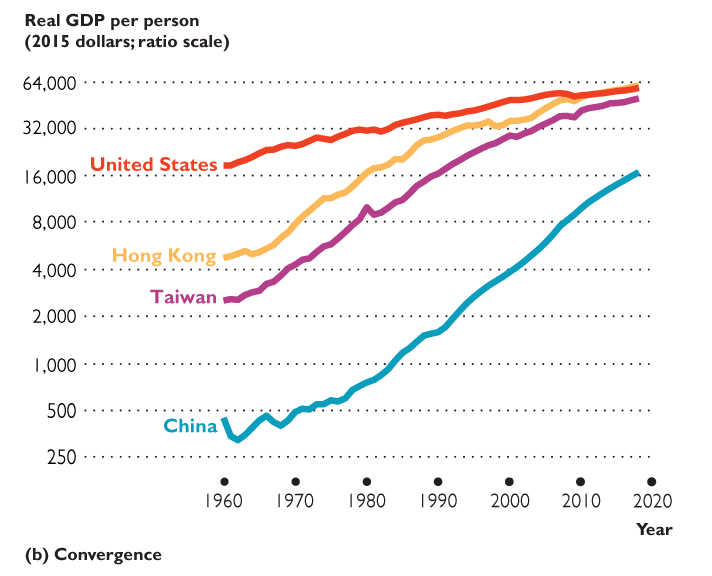

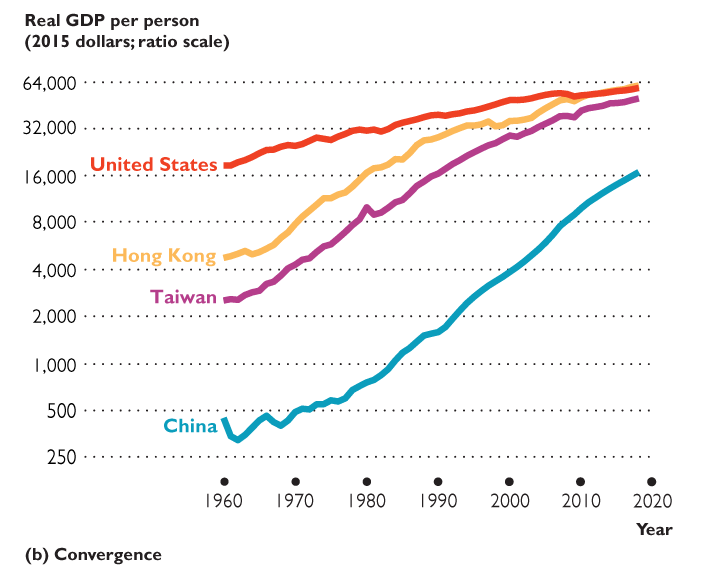

Persistent Gaps and Convergence

Some regions have experienced persistent gaps in real GDP per person, while others (notably some Asian economies) have converged toward the income levels of the richest nations.

Additional info: The images included above directly illustrate the concepts of persistent income gaps and convergence, as well as the productivity curves discussed in the labor productivity section. All equations are provided in LaTeX format as required.