Back

BackEconomic Growth: Principles, Measurement, and Theories

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Economic Growth

Definition and Measurement

Economic growth refers to the sustained expansion of real Gross Domestic Product (GDP) over time. It is a central concept in macroeconomics, reflecting improvements in a nation's standard of living and productive capacity.

Economic Growth Rate: The annual percentage change in real GDP, calculated as:

Per Capita Real GDP: Real GDP divided by the population, indicating average economic output per person.

Per Capita Real GDP Growth Rate: Measures how much faster real GDP grows compared to population growth.

Example: If Real GDP in 2022 is $25.46 trillion and in 2021 is $22.99 trillion, the growth rate is 10.74%. If population grows from 332.6 million to 334.1 million, per capita GDP also increases.

Short-Run vs. Long-Run Growth

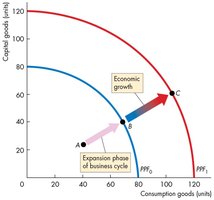

Economic growth can be observed in two contexts: the short-run return to potential GDP during the business cycle, and the long-run increase in potential GDP due to improvements in resources and technology.

Expansion Phase: The economy returns to full employment, moving from a point inside the production possibilities frontier (PPF) to the frontier itself.

Long-Run Growth: The PPF shifts outward, representing an increase in potential GDP.

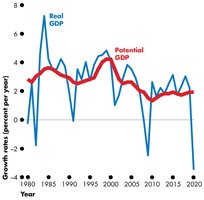

Real GDP vs. Potential GDP

Real GDP fluctuates more than potential GDP due to the business cycle. Potential GDP grows steadily, driven by productivity, capital investment, and technological progress.

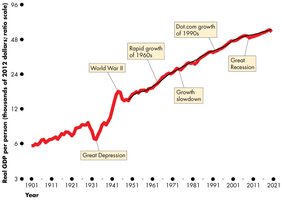

Long-Term Trends in Economic Growth

Over the past century, real GDP per person has generally increased, with notable periods of rapid growth and slowdowns due to historical events such as wars, depressions, and technological booms.

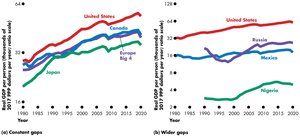

International Comparisons

Economic growth rates and levels of GDP per person vary significantly across countries and regions. Developed economies tend to have higher and more stable growth, while developing economies may experience wider gaps and more volatility.

The Rule of 70

The Rule of 70 is a simple way to estimate how long it takes for a variable to double, given a constant growth rate.

Formula:

Example: An investment growing at 7% doubles in 10 years; at 10%, it doubles in 7 years.

Determinants of Potential GDP

Factors of Production

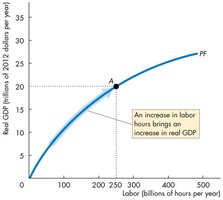

Potential GDP is determined by the economy's available resources: labor, capital, land, and entrepreneurial ability. In the short run, labor is the most variable input.

Aggregate Production Function: Shows the relationship between labor employed and real GDP produced, holding other factors constant.

Diminishing Marginal Returns: As more labor is employed, the additional output from each extra worker decreases.

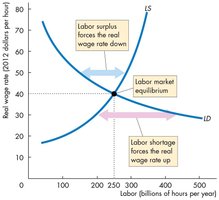

Labor Market Dynamics

The labor market determines the equilibrium real wage and quantity of labor employed. Surpluses and shortages adjust the wage rate toward equilibrium.

Labor Demand: Downward sloping due to diminishing marginal returns.

Labor Supply: Upward sloping as higher wages attract more workers.

Growth in Potential GDP

Potential GDP increases when the supply of labor rises, either through higher employment-to-population ratios or population growth. This leads to lower real wages and higher labor demand, increasing real GDP.

Labor Productivity

Labor productivity, defined as real GDP per aggregate labor hour, is a key driver of economic growth. Increases in productivity raise potential GDP, real GDP, and real GDP per capita.

Sources of Productivity Growth:

Increased physical capital (machines, infrastructure)

Increased human capital (education, skills)

Technological improvement

Theories of Economic Growth

Classical Growth Theory

Developed during the Industrial Revolution, this theory (associated with Thomas Malthus) posits that productivity gains are temporary, as population growth eventually outpaces resource growth, leading to stagnation or decline in living standards.

Key Points:

Productivity increases are short-lived.

Population growth absorbs gains, leading to diminishing returns and potential famine.

Neoclassical Growth Theory

Emerging in the 1950s, this theory emphasizes the role of technological change in driving long-term growth. However, it assumes that economic growth does not influence the rate of technological progress, which is seen as exogenous (determined outside the model).

Key Points:

Technological change is the main driver of growth.

Without ongoing technological advances, growth slows due to diminishing returns to capital.

As incomes rise, birth rates fall, moderating population growth.

New Growth Theory

This modern theory argues that economic growth results from intentional choices by individuals and firms seeking profit. Knowledge and innovation are central, and knowledge is a public good that does not suffer from diminishing returns.

Key Points:

Profit motive drives technological innovation.

Knowledge spillovers benefit the entire economy.

Growth can continue indefinitely if innovation persists.

Policy Implications for Growth

Policies that enhance growth include:

Increasing the capital/labor ratio

Stimulating saving and investment

Encouraging technological change and basic research

Investing in education and human capital

Promoting international trade to exploit comparative advantage

Summary Table: Theories of Economic Growth

Theory | Main Driver | Role of Technology | Population Effect |

|---|---|---|---|

Classical | Resources, Population | Limited, short-lived | Growth absorbs gains, leads to stagnation |

Neoclassical | Technology (exogenous) | Essential, but not influenced by economy | Moderates as incomes rise |

New Growth | Innovation, Knowledge | Endogenous, driven by profit motive | Not a limiting factor |

Additional info: The notes above expand on the provided content with definitions, formulas, and examples for clarity and completeness.