Back

BackExchange Rates and the Foreign Exchange Market: An Asset Approach

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Exchange Rates and the Foreign Exchange Market

Definitions and Quotation of Exchange Rates

Exchange rates are fundamental to international economics, allowing the comparison of prices and costs across countries. They are quoted as either foreign currency per unit of domestic currency or domestic currency per unit of foreign currency.

Exchange Rate: The price at which one currency can be exchanged for another.

Quotation Methods: For example, USD/JPY means how many yen can be exchanged for one dollar.

Application: Exchange rates enable the pricing of goods and services in a common currency, facilitating international trade.

Example: If a Nissan costs ¥2,500,000, the equivalent price in dollars depends on the current exchange rate.

Exchange Rate Tables and Interpretation

Exchange rate tables report mid-market rates for multiple currencies, showing the units of local currency per unit of base currency (e.g., USD, EUR, GBP). The 'Closing Mid' is the midpoint between bid and ask prices at market close, and 'Day’s Change' shows the daily change in the quote.

Interpretation: If 'local currency per USD' rises, the local currency depreciates against the USD; if it falls, it appreciates.

Example: If 1 USD = 1.3327 CAD today (up from yesterday), the Canadian dollar has depreciated against the USD.

Standard Currency Codes

International markets use three-letter codes to identify currencies (e.g., USD for US dollar, EUR for euro, JPY for Japanese yen).

Purpose: Standardization facilitates global trading and reporting.

Cross-Rate Calculations

Cross-rates allow calculation of exchange rates between two currencies using their rates with a third currency. For example, to find the CAD/EUR rate, multiply CAD/USD by USD/EUR.

Formula:

Example: If CAD/USD = 1.3020 and USD/EUR = 1.1701, then CAD/EUR = 1.5235.

Depreciation and Appreciation of Currencies

Depreciation

Depreciation is a decrease in the value of a currency relative to another currency.

Effect: The depreciated currency buys fewer units of foreign currency.

Example: If $1/€ increases to $1.20/€, the dollar has depreciated against the euro.

Impact: Imports become more expensive, exports become cheaper.

Appreciation

Appreciation is an increase in the value of a currency relative to another currency.

Effect: The appreciated currency buys more units of foreign currency.

Example: If $1/€ decreases to $0.90/€, the dollar has appreciated against the euro.

Impact: Imports become cheaper, exports become more expensive.

Relative Price Effects

Depreciation: Raises the price of imports, lowers the price of exports.

Appreciation: Lowers the price of imports, raises the price of exports.

Exchange Rate and Relative Prices Table

Table 14.2 shows how changes in the $/£ exchange rate affect the relative price of American jeans and British sweaters.

Example: As $/£ increases, the relative price (pairs of jeans per sweater) rises.

Real Exchange Rate

Definition and Calculation

The real exchange rate adjusts the nominal exchange rate for differences in price levels between countries, reflecting the relative purchasing power.

Formula:

Example: For GBP/EUR,

Change in Real Exchange Rate

Movements in nominal exchange rates and price levels affect the real exchange rate and thus the real purchasing power.

Formula:

Example: If GBP/EUR rises by 10%, Eurozone price level rises by 5%, UK price level rises by 2%, real exchange rate increases by about 13%.

Foreign Exchange Markets

Structure and Participants

The FX market is where currencies and related assets are traded. It is dominated by commercial banks, financial institutions, businesses, central banks, governments, and retail accounts.

Market Size: Daily turnover exceeds US$9.6 trillion (BIS, 2025).

Instruments: FX swaps (~42%), spot (~31%), forwards (~19%), options (~7%).

Participants: Commercial banks, non-bank financial institutions, businesses, central banks, governments, sovereign wealth funds, leveraged and retail accounts.

Market Integration and Arbitrage

Technological advances have integrated FX markets globally, eliminating significant differences in exchange rates across locations. Arbitrage opportunities are quickly exploited.

Arbitrage: Buying currency where it is cheaper and selling where it is more expensive for profit.

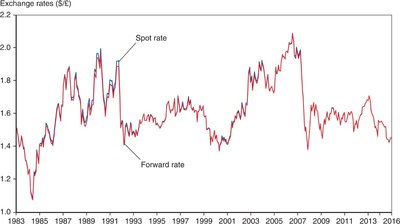

Spot Rates and Forward Rates

Definitions

Spot rates are for immediate currency exchanges, while forward rates are for exchanges at a future date, typically 30, 90, 180, or 360 days ahead.

Negotiation: Forward rates are agreed upon today for future exchanges.

Forward Points and Rate Calculation

Forward points are added to the spot rate to obtain the forward rate. For most currencies, divide points by 10,000 and add to the spot rate.

Formula:

Example: Spot rate = 1.15885, 3-month forward points = 80.9, Forward rate = 1.16694.

Other Methods of Currency Exchange

Swaps, Futures, and Options

Foreign Exchange Swaps: Combine a spot sale with a forward repurchase.

Futures Contracts: Standardized contracts for currency delivery on a set date.

Options Contracts: Give the right, but not obligation, to buy/sell currency by a set date.

The Demand for Currency Deposits

Determinants of Demand

The demand for currency deposits is influenced by the expected rate of return, risk, and liquidity. In FX markets, risk and liquidity are assumed similar across currencies, so rate of return is primary.

Rate of Return: Percentage change in asset value over time.

Real Rate of Return: Adjusted for inflation.

Interest Rate: The main determinant for deposit returns.

Expected Appreciation/Depreciation: Also affects returns.

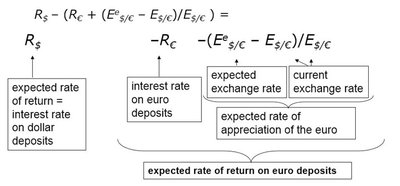

Comparing Returns on Domestic and Foreign Deposits

To compare returns, consider the interest rate and expected currency appreciation/depreciation.

Formula: /\euro} - E_{\/\euro}}$

Example: If dollar deposit rate is 2%, euro deposit rate is 4%, and expected exchange rate changes, calculate expected returns accordingly.

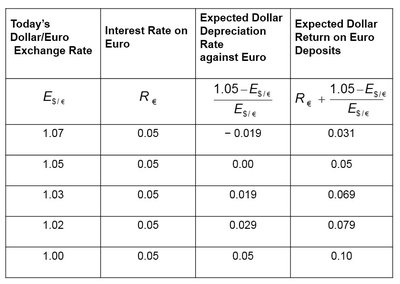

Table: Dollar/Euro Exchange Rate and Expected Returns

This table compares today's dollar/euro exchange rate, euro interest rate, expected dollar depreciation rate, and expected dollar return on euro deposits.

Today's Dollar/Euro Exchange Rate | Interest Rate on Euro | Expected Dollar Depreciation Rate against Euro | Expected Dollar Return on Euro Deposits |

|---|---|---|---|

1.07 | 0.05 | -0.019 | 0.031 |

1.05 | 0.05 | 0 | 0.05 |

1.03 | 0.05 | 0.019 | 0.069 |

1.02 | 0.05 | 0.029 | 0.079 |

1.00 | 0.05 | 0.05 | 0.10 |

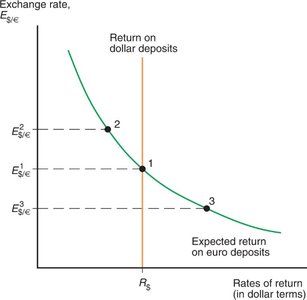

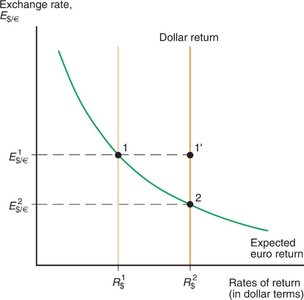

Model of Foreign Exchange Markets

Interest Parity and Equilibrium

The foreign exchange market is in equilibrium when deposits in all currencies offer the same expected rate of return. This is known as interest parity.

Interest Parity Condition: } = R_{\text{euro}} + \frac{E^e_{\/\euro}}{E_{\

Implication: No arbitrage opportunities exist; assets are equally desirable.

Graphical Representation

Equilibrium occurs where the expected dollar returns on dollar and euro deposits are equal.

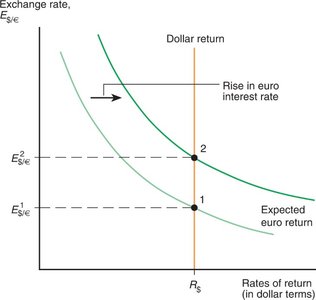

Effects of Changing Interest Rates

Changes in interest rates affect currency values:

Increase in Dollar Interest Rate: Dollar appreciates.

Increase in Euro Interest Rate: Dollar depreciates.

Expectations and Currency Movements

Expectations of future appreciation or depreciation can lead to actual currency movements, often becoming self-fulfilling prophecies.

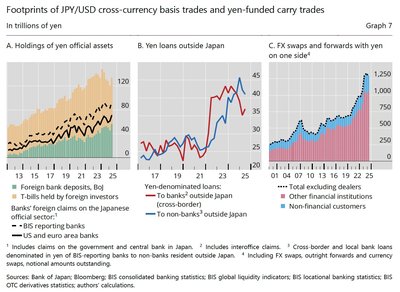

Carry Trades and FX Risk

Yen-Funded Carry Trades

Carry trades exploit interest rate differentials, often borrowing in low-yield currencies (like JPY) and investing in higher-yield currencies. These trades are exposed to sharp reversals during risk-off episodes.

Crash Risk: The main risk is abrupt unwinding when global risk sentiment changes.

Covered Interest Parity and Forward Rates

Covered Interest Parity

Covered interest parity relates interest rates across countries and the rate of change between forward and spot exchange rates.

Formula: } = R_{\text{euro}} + \frac{F_{\/\euro}}{E_{\

Implication: Rates of return on dollar deposits and "covered" foreign currency deposits are equal.

Forward Rate Calculation

Formula:

Application: The currency with the higher interest rate trades at a discount in the forward market.

Example: For a 30-day term, if domestic rate is 2%, foreign rate is 3%, spot rate is 1.6555, then .

Forward Discounts and Premiums

Formula:

Interpretation: Forward rates are at a premium or discount depending on interest rate differentials.