Back

BackFoundations of Economics: Scarcity, Trade-Offs, and Market Dynamics

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 1: The Nature of Economics

Incentives and Economic Behavior

In economics, incentives are rewards or penalties that influence the choices individuals make. The study of economics begins with understanding how people respond to these incentives, often in self-interested ways.

Positive incentives: Rewards such as bonuses, gold stars, or improved quality of life.

Negative incentives: Penalties or punishments, such as fines or overdraft fees.

Rationality assumption: People do not intentionally make decisions that leave them worse off.

Marginal analysis is central to economic decision-making, focusing on the additional benefit versus the additional cost ().

Economics: Definition and Scope

Economics is the study of how people allocate limited resources to satisfy unlimited wants. It examines choices made by individuals, households, firms, and governments.

Microeconomics: Focuses on individual and firm decision-making.

Macroeconomics: Studies the economy as a whole, including aggregates like national output, unemployment, and inflation.

Economic Systems and Fundamental Questions

Every society must answer three basic economic questions:

What and how much will be produced?

How will items be produced?

For whom will items be produced?

Economic systems provide different answers:

Traditional Economy: Decisions based on customs and traditions.

Command Economy: Central authority makes decisions.

Market Economy: Decisions made by buyers and sellers through price signals.

Models, Assumptions, and Empirical Science

Economists use models—simplified representations of reality—to predict and explain economic phenomena. Models are based on assumptions and are tested using real-world data (empirical science).

Ceteris paribus: "Other things equal"—holding other factors constant when analyzing changes.

Behavioral economics: Considers psychological limitations and bounded rationality in decision-making.

Positive vs. Normative Statements

Positive statements: Descriptive, "what is" (e.g., "If A, then B").

Normative statements: Value judgments, "what ought to be" (e.g., "The government should lower taxes.").

Correlation vs. Causation

Correlation: Predictable relationship between two variables.

Causation: One event directly triggers another (cause and effect).

Chapter 2: Scarcity and the World of Trade-Offs

Scarcity and Trade-Offs

Scarcity is the fundamental economic problem: resources are limited, but wants are unlimited. Scarcity is not the same as a shortage or poverty.

Trade-offs: Choosing one option means giving up another.

Opportunity cost: The value of the next-best alternative forgone.

Factors of Production

Land: Natural resources.

Labor: Human effort (physical and mental).

Physical capital: Machinery, factories.

Human capital: Education and training.

Entrepreneurship: Organizing resources, taking risks.

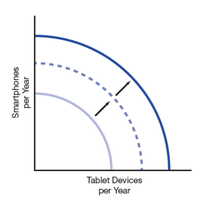

Production Possibilities Curve (PPC)

The PPC illustrates all possible combinations of two goods that can be produced with fixed resources and technology. It demonstrates opportunity cost, efficiency, and economic growth.

Efficient point: On the curve—maximum output.

Inefficient point: Inside the curve—resources underutilized.

Law of increasing additional cost: Opportunity cost rises as more of a good is produced, causing the curve to bow outward.

Economic growth: Outward shift of the PPC.

Consumer goods satisfy personal wants; capital goods are used to produce other goods. Investing in capital goods increases future economic growth.

Specialization and Comparative Advantage

Specialization increases productivity by focusing on tasks where individuals or nations have a comparative advantage—the ability to produce at a lower opportunity cost. Absolute advantage means producing more with the same resources.

Specialization leads to division of labor and greater efficiency.

Trade based on comparative advantage raises output and living standards.

Chapter 3: Demand and Supply

Markets and Price Determination

A market is any arrangement for exchanging goods and services. Prices are determined by the interaction of demand and supply.

Demand: Quantity of a good consumers are willing to buy at various prices.

Law of demand: As price rises, quantity demanded falls (inverse relationship).

Supply: Quantity of a good producers are willing to sell at various prices.

Law of supply: As price rises, quantity supplied increases (direct relationship).

Demand and Supply Schedules

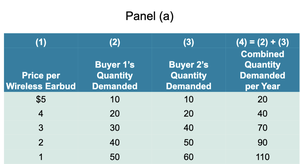

Demand and supply schedules are tables relating prices to quantities demanded or supplied. The market demand is the sum of individual demands.

Price per Wireless Earbud | Buyer 1's Quantity Demanded | Buyer 2's Quantity Demanded | Combined Quantity Demanded per Year |

|---|---|---|---|

$5 | 10 | 10 | 20 |

$4 | 20 | 20 | 40 |

$3 | 30 | 40 | 70 |

$2 | 40 | 50 | 90 |

$1 | 50 | 60 | 110 |

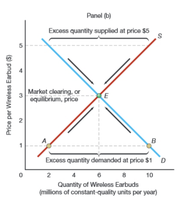

Demand and Supply Curves

Demand and supply curves graphically represent the relationship between price and quantity. The intersection is the equilibrium price, where quantity demanded equals quantity supplied.

Shortage: Quantity demanded exceeds quantity supplied (price below equilibrium).

Surplus: Quantity supplied exceeds quantity demanded (price above equilibrium).

Shifts vs. Movements

Change in demand/supply: Entire curve shifts due to factors other than price (e.g., income, tastes, technology).

Change in quantity demanded/supplied: Movement along the curve due to price change.

Chapter 4: Extensions of Demand and Supply Analysis

Price System and Voluntary Exchange

The price system uses changing prices to signal relative scarcity and abundance. Voluntary exchange makes both parties better off, but involves transaction costs (search, contracting, enforcement).

Middlemen: Reduce transaction costs by providing information.

Platform firms: Connect buyers and sellers via networks.

Market Adjustments and Price Controls

Changes in demand or supply create disequilibrium, prompting price and quantity adjustments. Government-imposed price ceilings (maximum price) and price floors (minimum price) disrupt equilibrium, causing shortages or surpluses.

Price ceiling: Below equilibrium, creates shortage and black markets.

Price floor: Above equilibrium, creates surplus (e.g., minimum wage, agricultural supports).

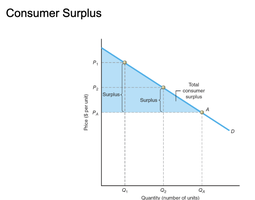

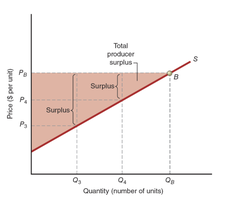

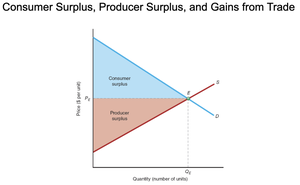

Consumer Surplus and Producer Surplus

Consumer surplus is the difference between what consumers are willing to pay and what they actually pay. Producer surplus is the difference between what producers receive and their minimum acceptable price.

Gains from trade: Sum of consumer and producer surplus.

Price controls reduce gains from trade by lowering both consumer and producer surplus.

Nonprice Rationing and Black Markets

Nonprice rationing: Queues, random assignment, coupons, or force.

Black market: Illegal sales above controlled prices.

Price rationing is generally more efficient than nonprice rationing, capturing all gains from trade.

Summary Table: Key Concepts

Concept | Definition | Example |

|---|---|---|

Scarcity | Limited resources, unlimited wants | Time, money, raw materials |

Opportunity Cost | Value of next-best alternative forgone | Choosing study over leisure |

Comparative Advantage | Lower opportunity cost in production | Country A produces wheat, Country B produces cars |

Equilibrium Price | Price where demand equals supply | Market price for wireless earbuds |

Consumer Surplus | Willingness to pay minus actual payment | Buying a product for less than expected |

Producer Surplus | Actual receipt minus minimum acceptable price | Selling above minimum price |