Back

BackInflation and Interest Rates: Concepts, Measurement, and Canadian Trends

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Inflation and Interest Rates

Inflation: Definition and Measurement

Inflation is a key macroeconomic concept that measures the growth in the cost of living over time. It is most commonly quantified using the Consumer Price Index (CPI), which tracks the price changes of a representative basket of consumer goods and services.

Inflation Rate Formula: The inflation rate between year t and t+1 is calculated as: where is the CPI in year t.

Consumer Price Index (CPI): The CPI is defined as: It is a weighted average of consumer goods prices, and the base year is periodically updated to reflect changes in consumer preferences.

Core CPI: Core CPI excludes volatile items such as food and energy to provide a more stable measure of underlying inflation.

Annualized Inflation Rate

Inflation rates are typically reported on an annualized basis, even if the underlying data is monthly. To convert an annual inflation rate to a monthly rate, compounding must be considered.

Monthly Inflation Rate Formula: If the annual inflation rate is , the monthly rate is: For example, an annual rate of 3.2% corresponds to a monthly rate of approximately 0.26%.

Application: This compounding approach is also used for other rates, such as interest rates.

Interest Rates: Types and Measurement

An interest rate is the rate of return promised by a borrower to a lender. There are many types of interest rates in the economy, including explicit rates (e.g., GICs, mortgages, credit cards) and rates implied by asset prices (e.g., government bond yields).

Explicit Interest Rates: Directly stated rates, such as those on loans and deposits.

Implied Interest Rates: Derived from asset prices, such as bond yields.

Substitution Effect: Because assets can often be substituted, interest rates tend to move together.

Annualized Interest Rates and Compounding

Interest rates are usually reported on an annualized basis, but actual payment periods may differ. Compounding affects the effective rate paid or received.

Example: If a mortgage rate is 8% annually and payments are made twice per month, the per-period rate is: Compounding this rate for 24 periods yields an effective rate of approximately 8.31%.

Effective Rate: The true rate is between the nominal and compounded rates, depending on payment structure.

Nominal vs. Real Interest Rates

Inflation erodes the purchasing power of money, affecting the real return on loans and investments. The distinction between nominal and real interest rates is crucial for understanding the true cost or benefit of borrowing and lending.

Real Interest Rate (ex post): The realized real interest rate is: where is the nominal interest rate and is the actual inflation rate.

Nominal Interest Rate: The stated rate, not adjusted for inflation.

Real Interest Rate: The inflation-adjusted rate, reflecting the true increase in purchasing power.

Example: If the nominal interest rate is 5% and inflation is 2%, the real interest rate is 3%.

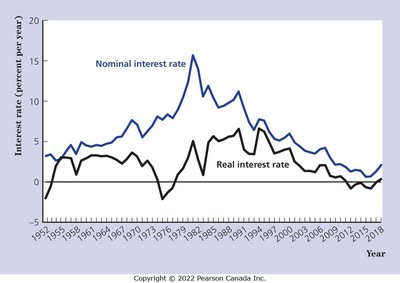

Trends in Canadian Interest Rates

Interest rates in Canada have fluctuated significantly over the decades. Nominal rates peaked in the 1980s, while real rates have also varied, sometimes becoming negative during periods of high inflation or economic crisis.

Recent Trends: Both nominal and real interest rates are lower today than in past decades. Real rates became negative during COVID-19 but have turned positive as nominal rates rose and inflation fell.

Implication: Low real interest rates can make borrowing more attractive, but the true cost depends on inflation expectations.

Expected Real Interest Rate (ex ante)

When making borrowing or lending decisions, the expected real interest rate is more relevant than the realized rate, since future inflation is uncertain.

Expected Real Interest Rate Formula: where is expected inflation.

Measurement: Expected inflation is difficult to measure and varies across individuals and institutions, but it is central to macroeconomic policy and decision-making.

Importance of Expected Inflation

Small differences in expected inflation can have significant effects on real interest rates and economic decisions. For example, an annual inflation rate of 3.2% versus 3.3% results in a slightly higher monthly rate, but this can impact borrowing costs and investment returns over time.

Monthly Rate Calculation: For an annual rate of 3.3%, the monthly rate is:

Significance: Even small changes in inflation expectations can affect real interest rates and macroeconomic outcomes.