Back

BackIntroduction to Macroeconomics: Growth, Fluctuations, and Policy Foundations

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Introduction to Macroeconomics

Scope and Historical Context

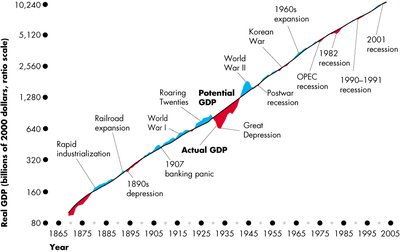

Macroeconomics studies the behavior and performance of an economy as a whole, focusing on aggregate measures such as output, unemployment, and inflation. The field emerged in response to the inability of classical economics to explain prolonged periods of high unemployment, most notably during the Great Depression.

A Brief History of Macroeconomics

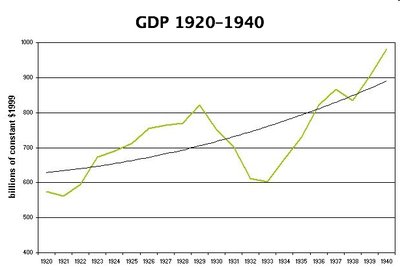

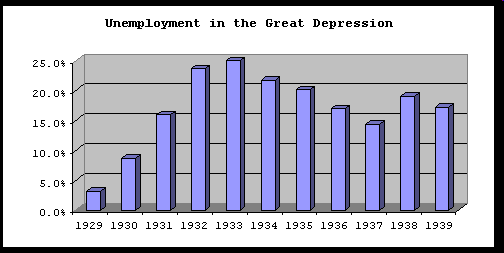

The Great Depression and the Birth of Macroeconomics

Great Depression: A period of severe economic contraction and high unemployment beginning in 1929 and lasting through the 1930s.

Classical Macroeconomics: Argued that markets are self-correcting and government intervention is unnecessary. However, this view failed to explain persistent unemployment during the Great Depression.

Keynesian Revolution: John Maynard Keynes, in his 1936 work The General Theory of Employment, Interest, and Money, argued that economies can remain in prolonged periods of underemployment and require active government intervention to restore full employment.

Fine-Tuning and Disillusionment

Fine-tuning: The idea, popular in the 1960s, that government could regulate inflation and unemployment through policy adjustments.

Stagflation: In the 1970s, economies experienced high inflation and high unemployment simultaneously, challenging Keynesian models and leading to new approaches.

Macroeconomic Concerns

Output Growth

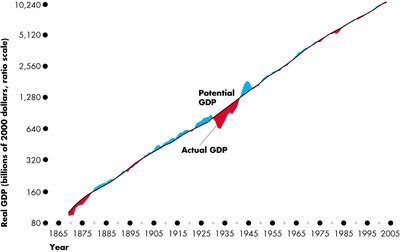

Output growth refers to the increase in the total quantity of goods and services produced in an economy over time. Economists distinguish between short-run fluctuations (business cycles) and long-run growth trends.

Aggregate Output: The total quantity of goods and services produced in an economy in a given period.

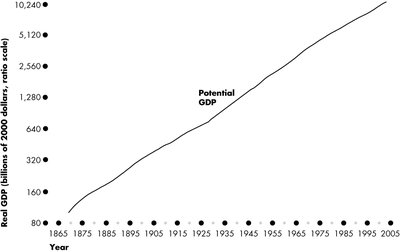

Potential GDP: The level of output an economy can produce at full employment.

Actual GDP: The real output produced, which may fluctuate around potential GDP due to economic cycles.

Unemployment

Unemployment measures the percentage of the labor force that is not employed but actively seeking work. High unemployment is a major concern for policymakers.

Unemployment Rate Formula:

$ \text{Unemployment Rate} = \frac{\text{Number of Unemployed}}{\text{Labor Force}} \times 100 $

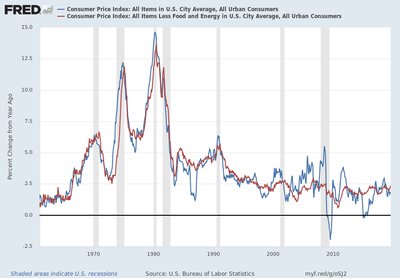

Inflation and Deflation

Inflation is the rate at which the general price level of goods and services rises, eroding purchasing power. Deflation is the opposite, with falling prices. Hyperinflation refers to extremely rapid price increases.

Inflation: Sustained increase in the overall price level.

Deflation: Sustained decrease in the overall price level.

Hyperinflation: Exceptionally high and typically accelerating inflation.

The Components of the Macroeconomy

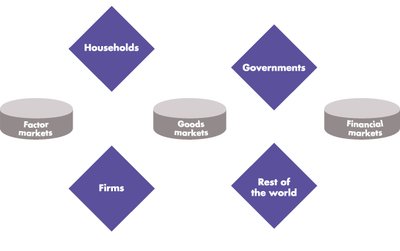

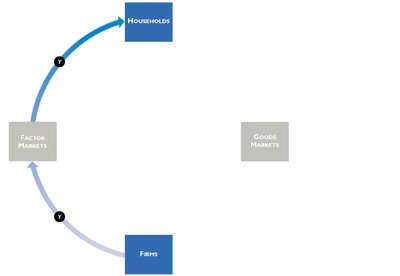

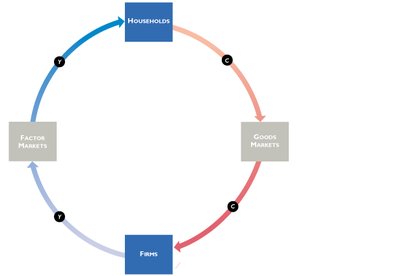

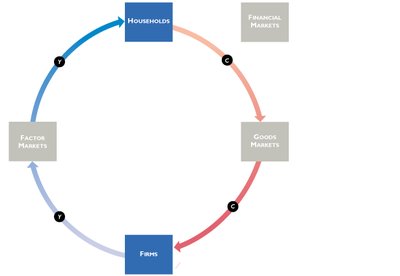

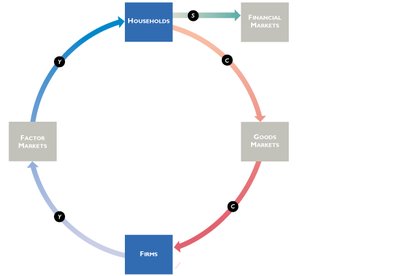

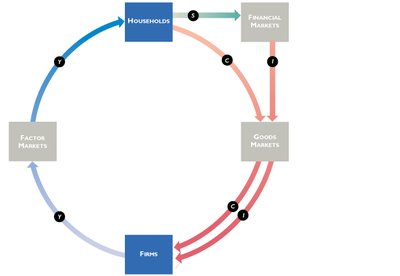

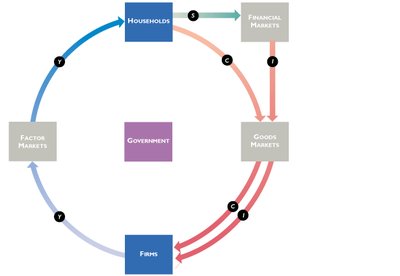

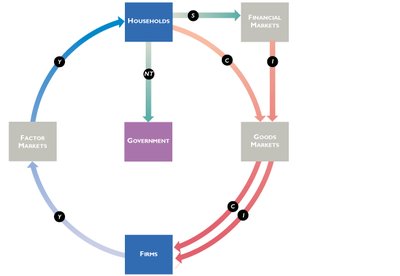

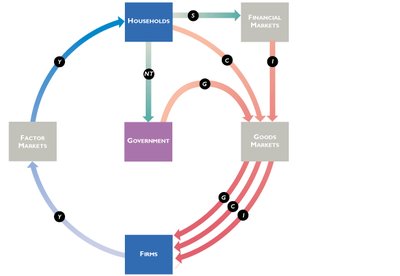

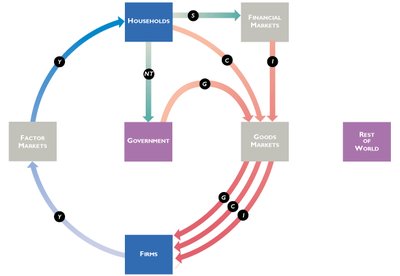

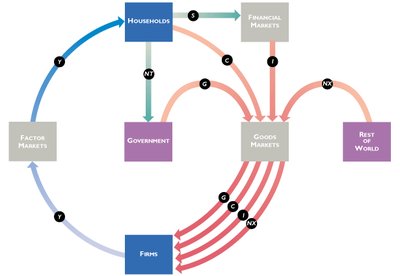

The Circular Flow Diagram

The circular flow diagram illustrates the movement of money, resources, and goods among households, firms, the government, and the rest of the world. It highlights the interdependence of different sectors in the economy.

Households: Supply factors of production and demand goods and services.

Firms: Demand factors of production and supply goods and services.

Government: Collects taxes and provides public goods and services.

Financial Markets: Channel savings and investment.

Rest of the World: Engages in trade (exports and imports).

The Three Market Arenas

Goods and Services Market: Where households buy and firms sell goods and services.

Labor (Factor) Market: Where households supply labor and firms demand it.

Financial Market: Where savings are channeled to investment.

The Role of Government in the Macroeconomy

Government influences the macroeconomy through fiscal, monetary, and supply-side policies.

Fiscal Policy: Government decisions on taxation and spending.

Monetary Policy: Central bank actions that determine the money supply and interest rates.

Supply-Side Policies: Policies aimed at increasing aggregate supply, such as deregulation and tax incentives.

Aggregate Demand and Aggregate Supply

Definitions

Aggregate Demand (AD): The total demand for goods and services in an economy at a given overall price level and in a given period.

Aggregate Supply (AS): The total supply of goods and services that firms in an economy plan on selling during a specific time period.

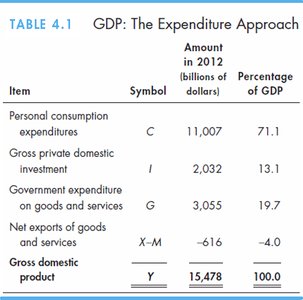

Summary Table: GDP by the Expenditure Approach

The expenditure approach to GDP sums consumption, investment, government spending, and net exports:

Item | Symbol | Amount in 2012 (billions of dollars) | Percentage of GDP |

|---|---|---|---|

Personal consumption expenditures | C | 11,007 | 71.1 |

Gross private domestic investment | I | 2,032 | 13.1 |

Government expenditure on goods and services | G | 3,055 | 19.7 |

Net exports of goods and services | X-M | -616 | -4.0 |

Gross domestic product | Y | 15,478 | 100.0 |

Key Equations

GDP (Expenditure Approach):

$ Y = C + I + G + (X - M) $

Unemployment Rate:

$ \text{Unemployment Rate} = \frac{\text{Number of Unemployed}}{\text{Labor Force}} \times 100 $

Conclusion

Macroeconomics provides the tools to analyze the overall performance of economies, understand the causes of economic fluctuations, and evaluate the effectiveness of government policies. Key concerns include output growth, unemployment, and inflation, all of which are interconnected through the circular flow of income and expenditure.