Back

BackLong-Run Economic Growth: Sources and Policies – Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Long-Run Economic Growth: Sources and Policies

Introduction

Long-run economic growth is a central topic in macroeconomics, focusing on the sustained increase in real GDP per capita and the policies and factors that drive or hinder this growth. Understanding the sources of economic growth, the reasons for differences across countries, and the role of government policy is essential for analyzing global prosperity and development.

Economic Growth over Time and around the World

Definition and Measurement of Economic Growth

Economic growth occurs when real GDP per capita increases over time.

Growth rates are calculated as the percentage change in real GDP per capita from one period to the next.

Small differences in growth rates, when compounded over many years, lead to large differences in living standards.

Historical Trends

There was little to no economic growth from year 1 to 1000 CE.

Significant growth began with the Industrial Revolution (England, ~1750), which introduced mechanical power to production.

High-income countries (Western Europe, US, Japan, etc.) have experienced sustained growth, while many developing countries have not.

Global Variation in Income

The world is divided into high-income (industrialized) and developing countries.

Some developing countries (e.g., Singapore, South Korea, Taiwan) have achieved rapid growth and are termed "newly industrializing countries."

Standard of living includes not only income but also health, education, and civil liberties.

What Determines How Fast Economies Grow?

The Economic Growth Model

The economic growth model explains long-run increases in real GDP per capita by focusing on labor productivity, which is determined by capital and technology.

Labor productivity: Quantity of goods and services produced by one worker or one hour of work.

Key determinants:

Quantity of capital per hour worked

Level of technology

Technological change: Improvements in machinery, human capital, and organizational methods.

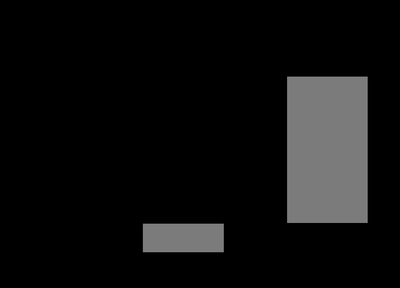

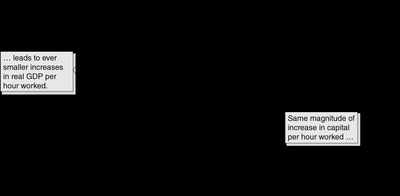

The Per-Worker Production Function

The per-worker production function shows the relationship between real GDP per hour worked and capital per hour worked, holding technology constant. It illustrates the concept of diminishing returns to capital.

Increases in capital per hour worked lead to smaller and smaller increases in output per hour worked (diminishing returns).

Technological change shifts the production function upward, allowing more output with the same input.

Capital vs. Technological Change

Technological change is essential for sustaining long-run growth, as it helps economies avoid diminishing returns to capital.

Replacing old capital with more productive capital or reorganizing production are examples of technological change.

New Growth Theory

Developed by Paul Romer, this theory emphasizes that technological change is driven by economic incentives and market forces.

Knowledge capital (accumulated knowledge from R&D and education) is subject to increasing returns at the economy-wide level.

Government policies can increase knowledge capital by:

Protecting intellectual property (patents, copyrights)

Subsidizing research and development

Subsidizing education

Creative Destruction

Joseph Schumpeter described creative destruction as the process by which new technologies and products replace old ones, driving economic growth but also causing some firms to fail.

Economic Growth in the United States

Trends in Productivity Growth

Rapid productivity growth from post-WWII to mid-1970s, slowdown until mid-1990s, then a brief acceleration, and another slowdown after 2006.

Debate exists over whether the US is entering a period of slow growth (secular stagnation) or if new technologies (e.g., AI) will drive future growth.

Productivity growth can cause short-term job losses in some industries but raises wages and living standards in the long run.

Why Isn’t the Whole World Rich?

The Catch-Up Effect

The economic growth model predicts that poor countries should grow faster than rich countries (catch-up effect).

In reality, only some countries have caught up; many developing countries have not.

Barriers to Growth in Poor Countries

Failure to enforce the rule of law (property rights, contract enforcement)

Wars and revolutions

Poor public education and health

Low rates of saving and investment

Role of Globalization

Globalization (openness to trade and investment) helps developing countries access technology and capital, promoting growth.

Foreign direct investment (FDI) and foreign portfolio investment are important channels for technology and capital transfer.

Growth Policies

Government Policies to Foster Growth

Enhancing property rights and the rule of law to encourage entrepreneurship and investment

Improving health and education to increase labor productivity

Promoting technological change through R&D subsidies and support for education

Encouraging saving and investment with tax incentives (e.g., investment tax credits)

Debates about Economic Growth

Growth is associated with higher living standards but may also contribute to environmental problems and inequality.

Economic analysis can inform the debate but cannot resolve normative questions about the desirability of growth.

Key Terms and Concepts

Catch-up: Prediction that poor countries will grow faster than rich countries.

Economic growth model: Explains long-run growth in real GDP per capita.

Foreign direct investment (FDI): Building or purchasing facilities in a foreign country.

Foreign portfolio investment: Buying stocks or bonds issued in another country.

Globalization: Openness to foreign trade and investment.

Human capital: Knowledge and skills acquired by workers.

Labor productivity: Output per worker or per hour worked.

New growth theory: Emphasizes the role of incentives and knowledge capital in technological change.

Patent: Exclusive right to produce a product for 20 years.

Per-worker production function: Relationship between output per worker and capital per worker, holding technology constant.

Property rights: Rights to use, buy, or sell property.

Rule of law: Government's ability to enforce laws and protect property rights.

Technological change: Changes in the ability to produce output with given inputs.