Back

BackMacroeconomics Study Notes: GDP, Labor Markets, Inflation, and Economic Growth

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Monitoring the Value of Production: GDP

Introduction to Macroeconomic Measurement

Macroeconomics focuses on the overall performance of an economy, particularly the measurement of total production within a country over a specific period. The main challenge is aggregating the value of diverse goods and services into a single, comprehensive measure.

Gross Domestic Product (GDP): The market value of all final goods and services produced within a country in a given time period.

GDP is the primary indicator of a country's productivity and wealth.

Key Concepts in GDP Measurement

Market Values: GDP uses market prices to value goods and services, allowing aggregation of different products.

Final Goods vs. Intermediate Goods:

Final good: Purchased by the end user; included in GDP.

Intermediate good: Used as input for another product; not included in GDP to avoid double counting.

Example: A log sold to a lumber company is an intermediate good; a finished cornhole board sold to a consumer is a final good and counts toward GDP.

Domestic Production: Only goods and services produced within a country's borders are counted in its GDP.

Time Period: GDP is measured over a specific interval, typically quarterly or annually.

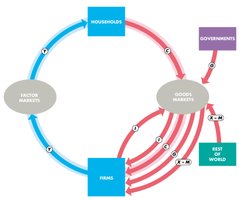

The Circular Flow of Expenditure and Income

The circular flow model illustrates how money moves through the economy between households, firms, governments, and the rest of the world. Payments for goods and services (expenditures) and payments for factors of production (income) are tracked to measure GDP.

Expenditure Types:

Consumption (C): Household spending on goods and services; largest GDP component.

Investment (I): Firm spending on capital goods; includes gross and net investment (net investment = gross investment – depreciation).

Government Expenditure (G): Government purchases of goods and services; excludes transfer payments and taxes.

Net Exports (X – M): Exports minus imports; positive if exports exceed imports, negative otherwise.

Income (Y): Payments to households for providing factors of production (wages, interest, rent, profit).

GDP Identity:

Nominal vs. Real GDP

Nominal GDP: Values output using current prices; does not account for inflation.

Real GDP: Values output using prices from a base year; allows comparison of production over time by removing price changes.

Real GDP per person: ; measures average standard of living.

Comparing GDP Across Countries

Exchange Rates: Converting GDP to a common currency can be misleading due to price differences between countries.

Purchasing Power Parity (PPP): Adjusts for price level differences, providing a more accurate comparison of living standards.

Limitations of Real GDP

Excludes household production, underground economic activity, leisure, and environmental quality.

Does not account for new goods or changes in quality.

Alternative measures: Human Development Index, Green Net National Product, Happiness Index.

Monitoring Jobs and Inflation

Labor Market Measurement

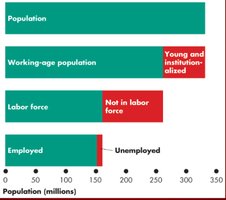

Labor is a critical factor in economic performance. The labor market is monitored using surveys and statistical indicators to assess employment and unemployment trends.

Current Population Survey (CPS): Monthly survey classifying individuals as employed, unemployed, or not in the labor force.

Labor Force: People working or actively seeking work.

Unemployed: No job, actively seeking work, or waiting to start a new job.

Marginally Attached Workers: Not in labor force, want a job but not actively searching.

Discouraged Workers: Marginally attached, stopped searching due to job market conditions.

Economic Part-Time Workers: Working part-time but want full-time employment.

Labor Market Indicators

Unemployment Rate:

Employment-to-Population Ratio:

Labor Force Participation Rate:

Types of Unemployment

Frictional Unemployment: Short-term, due to normal labor market turnover (e.g., job search, retirement).

Structural Unemployment: Mismatch between skills and job requirements due to economic changes.

Cyclical Unemployment: Caused by economic fluctuations (recessions and expansions).

Natural Unemployment Rate: Unemployment rate when cyclical unemployment is zero; economy is at full employment.

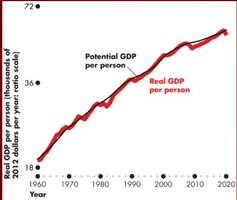

Unemployment and the Business Cycle

Potential GDP: Output at full employment.

Output Gap: Difference between real GDP and potential GDP.

When unemployment is above the natural rate, output gap is negative; when below, output gap is positive.

Inflation and the Price Level

Price Level: Average price of all goods and services; measured by indices like the Consumer Price Index (CPI).

Inflation: Persistent rise in the price level.

Deflation: Persistent fall in the price level.

Effects of Unexpected Inflation/Deflation: Redistributes income and wealth, affects real GDP and employment, and diverts resources from production.

Measuring the Price Level: CPI

Consumer Price Index (CPI):

CPI Inflation Rate:

Biases in CPI: New goods, quality changes, substitution, and outlet substitution biases cause CPI to overstate inflation.

Alternative Measures: Personal Consumption Expenditure (PCE) index and core inflation rate (excludes food and energy).

Real vs. Nominal Values

To compare values over time, adjust nominal values for inflation:

Example: Real wage rate = (Nominal wage rate / CPI) × 100

Economic Growth

Understanding Economic Growth

Economic growth refers to the sustained increase in a country's output of goods and services, typically measured by real GDP or real GDP per person.

Growth Rate Formula:

Growth Rate of Real GDP per Person: Growth rate of real GDP – Growth rate of population

Rule of 70: Years to double = 70 / (annual growth rate in percent)

Sources of Economic Growth

Potential GDP: Maximum sustainable output, determined by available factors of production.

Aggregate Production Function: Shows the relationship between labor input and real GDP; exhibits diminishing returns to labor.

Aggregate Labor Market: Labor supply and demand determine equilibrium wage and employment.

Growth of Potential GDP:

Increase in labor supply (population growth, higher participation).

Growth in labor productivity (output per labor hour).

Labor Productivity Growth: Driven by physical capital, human capital, and technological advances.

Theories of Economic Growth

Classical Growth Theory: Growth is temporary; population growth offsets gains, leading to subsistence living (Malthusian theory).

Neoclassical Growth Theory: Long-run growth depends on technological progress, which occurs randomly.

New Growth Theory: Technological progress results from purposeful investment in knowledge; knowledge is a public good, enabling sustained growth.