Back

BackLecture 12: Monetary Policy

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Monetary Policy: Short-Run and Long-Run Effects

Introduction to Monetary Policy

Monetary policy refers to the actions undertaken by a nation's central bank to influence the availability and cost of money and credit to promote national economic goals. The Federal Reserve (Fed) is the central bank of the United States and plays a crucial role in implementing monetary policy.

Central banks use monetary policy to manage economic growth, control inflation, and reduce unemployment.

Monetary policy can be expansionary (stimulating the economy) or contractionary (slowing the economy).

Short-Run Effects of Monetary Policy

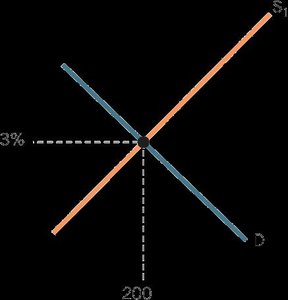

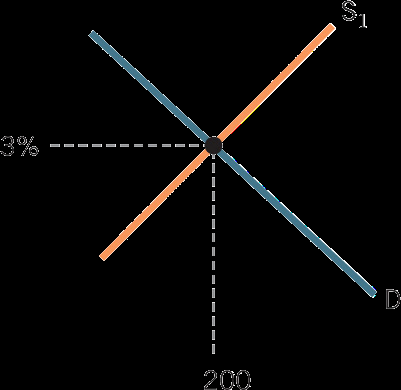

In the short run, monetary policy can influence real economic variables such as real GDP and unemployment due to price stickiness. The central bank typically manipulates the interest on reserve balances (IORB) rate to affect the money supply and interest rates.

Expansionary monetary policy lowers the IORB rate, increases the money supply, reduces interest rates, and stimulates investment and aggregate demand (AD).

Contractionary monetary policy raises the IORB rate, decreases the money supply, increases interest rates, and reduces investment and AD.

In the short run, these policies can increase or decrease real GDP and affect unemployment.

Example: Expansionary Policy in Action

A business owner is offered a loan at a lower interest rate after the Fed reduces the IORB rate, making investment more attractive and increasing aggregate demand.

Expansionary Monetary Policy: Transmission Mechanism

Decreases IORB rate → Increases money supply → Increases supply of loanable funds → Decreases interest rates → Increases investment → Increases AD

Expansionary Policy and the AD-AS Model

Lower interest rates increase investment, shifting the aggregate demand curve to the right, raising real GDP and lowering unemployment in the short run.

Contractionary Monetary Policy: Transmission Mechanism

Increases IORB rate → Decreases money supply → Decreases supply of loanable funds → Increases interest rates → Decreases investment → Decreases AD

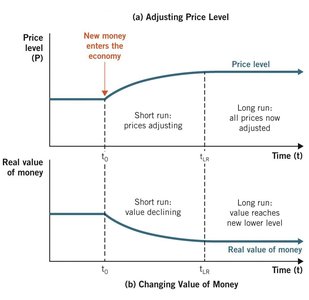

Real Versus Nominal Effects

While monetary policy can affect real variables in the short run, its long-run effects are primarily on nominal variables such as the price level. As prices adjust, the real value of money declines, leading to inflation.

Short-run: Increase in money supply raises real GDP and lowers unemployment.

Long-run: All prices adjust, and the only lasting effect is a higher price level (inflation).

Unexpected Inflation and Its Effects

Unexpected inflation resulting from expansionary monetary policy can harm individuals with fixed-price contracts, such as workers with fixed wages, lenders, and landlords. Conversely, unexpected deflation from contractionary policy can harm employers, borrowers, and renters with fixed contracts.

Limitations of Monetary Policy

Why Monetary Policy Doesn't Always Work

Monetary policy has several limitations that reduce its effectiveness in certain circumstances:

Long-run adjustments: In the long run, all prices adjust, and monetary policy does not affect real GDP or unemployment (monetary neutrality).

Adjustments in expectations: If monetary policy is anticipated, prices adjust quickly, and real effects are minimized.

Aggregate supply (AS) shifts: If recessions are caused by negative AS shocks, monetary policy may not restore normal growth.

Monetary Neutrality

Monetary neutrality is the concept that changes in the money supply do not affect real economic variables in the long run.

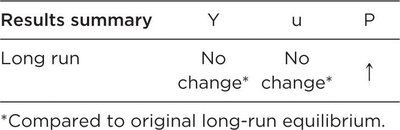

Summary Table: Long-Run Effects of Monetary Policy

Results summary | Y | u | P |

|---|---|---|---|

Long run | No change* | No change* | ↑ |

*Compared to original long-run equilibrium. | |||

Expectations and Aggregate Supply Shocks

If inflation is fully expected, contracts adjust, and monetary policy has no real effect, even in the short run.

Negative AS shocks (e.g., financial crises) can cause recessions that monetary policy cannot easily resolve.

The Phillips Curve

Definition and Short-Run Phillips Curve

The Phillips curve illustrates the short-run inverse relationship between inflation and unemployment. In the short run, higher inflation is associated with lower unemployment, and vice versa.

Central banks can, in theory, choose between higher inflation and lower unemployment in the short run.

Long-Run Phillips Curve

In the long run, the Phillips curve becomes vertical, indicating that there is no trade-off between inflation and unemployment. The unemployment rate returns to its natural rate regardless of the inflation rate.

Expectations and the Phillips Curve

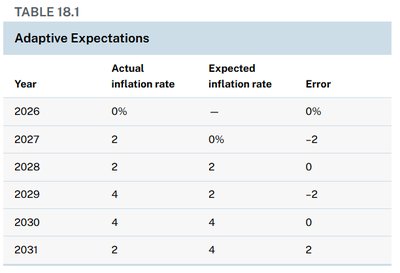

Adaptive expectations theory: People base their expectations of future inflation on past inflation rates. This can lead to systematic errors if inflation accelerates or decelerates.

Rational expectations theory: People use all available information to forecast future inflation, making fewer systematic errors.

Year | Actual inflation rate | Expected inflation rate | Error |

|---|---|---|---|

2026 | 0% | – | 0% |

2027 | 2% | 0% | -2 |

2028 | 2% | 2% | 0 |

2029 | 4% | 2% | -2 |

2030 | 4% | 4% | 0 |

2031 | 2% | 4% | 2 |

Implications for Monetary Policy

Active vs. Passive Monetary Policy

Active monetary policy: Central banks use policy to counteract economic fluctuations, but its effectiveness is limited by expectations and the long-run neutrality of money.

Passive monetary policy: Central banks focus on stabilizing the money supply and price levels, avoiding attempts to exploit the Phillips curve.

Protecting Against Inflation

Workers and lenders can protect themselves from inflation by including cost-of-living adjustments (COLA) in contracts or investing in assets that rise with inflation, such as Treasury Inflation Protected Securities (TIPS).

Conclusion

Monetary policy can influence real economic activity in the short run, but its long-run effects are limited to nominal variables like the price level. The effectiveness of monetary policy is constrained by expectations and the nature of economic shocks. The Phillips curve relationship holds only in the short run, and modern macroeconomics emphasizes the importance of expectations in determining the real effects of monetary policy.