Back

BackMoney and the Banking System: Foundations, Measurement, and Macroeconomic Implications

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Money and the Banking System

What Is Money, and Why Do We Need It?

Money is any asset that is generally accepted as payment for goods and services or for the settlement of debts. The existence of money eliminates the inefficiencies of barter, specifically the double coincidence of wants, by providing a universally accepted medium of exchange. Historically, societies have used commodity money—items with intrinsic value such as gold, silver, or beaver pelts—as well as paper money backed by commodities. Today, most economies use fiat money, which has value by government decree and is not backed by a physical commodity.

Medium of Exchange: Money is widely accepted for transactions.

Unit of Account: Money provides a standard measure of value.

Store of Value: Money preserves purchasing power over time.

Standard of Deferred Payment: Money facilitates transactions over time, such as loans.

For an asset to serve as money, it must be acceptable, standardized, durable, portable, and divisible. Modern economies rely on fiat money, which is valuable because of trust in the issuing authority, not because of intrinsic value.

How Is Money Measured in Canada Today?

The Bank of Canada uses several definitions to measure the money supply, ranging from narrow to broad:

M1+: Currency in circulation plus chequable deposits at banks and similar institutions.

M1++: M1+ plus non-chequable deposits.

M2: Currency plus all personal and non-personal deposits at banks.

M2+: M2 plus deposits at trust and mortgage loan companies, credit unions, life insurance annuities, government savings, and money market mutual funds.

M2++: M2+ plus Canada Savings Bonds and non-money market mutual funds (broadest measure).

M3: M2 plus non-personal term deposits and foreign currency deposits of Canadians at banks.

Liquidity decreases as we move from M1+ to M2++. The most relevant measure for transactions is M1+, which includes currency and demand deposits. The money supply is not just physical cash but also includes bank deposits, which are created through lending.

How Do Banks Create Money?

Banks are central to money creation in the modern economy. They operate on a fractional reserve system, holding only a fraction of deposits as reserves and lending out the rest. This process multiplies the amount of money in the economy through the money multiplier effect.

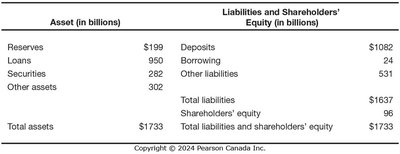

Balance Sheet Structure: Banks' assets include reserves, loans, securities, and other assets; liabilities include deposits, borrowings, and shareholders' equity.

When banks make loans, new deposits are created, expanding the money supply. The money multiplier quantifies this process:

Money Multiplier Formula:

For a 10% reserve ratio, the multiplier is 10: each dollar of reserves supports $10 in deposits.

However, the real-world multiplier is often lower due to excess reserves and cash held outside banks. Bank runs occur when many depositors withdraw funds simultaneously, threatening the stability of the system.

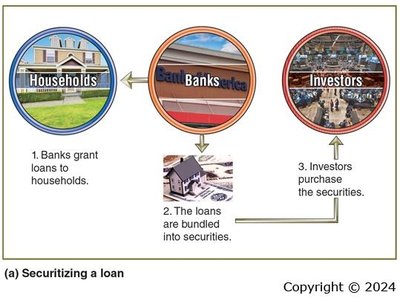

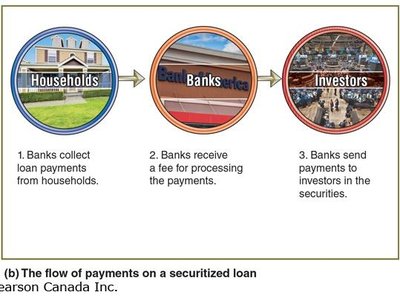

Securitization and the Shadow Banking System

Securitization is the process of bundling loans into securities that can be sold to investors. This allows banks to offload risk and recycle capital for new lending, but also makes the financial system more complex and potentially more fragile.

Shadow Banking: Non-bank financial institutions (investment banks, money market funds, hedge funds) provide credit outside traditional banking, amplifying money creation but with less regulation and safety nets.

The 2007–2009 financial crisis highlighted the risks of shadow banking, as these institutions lacked deposit insurance and central bank support, making them vulnerable to runs on short-term funding.

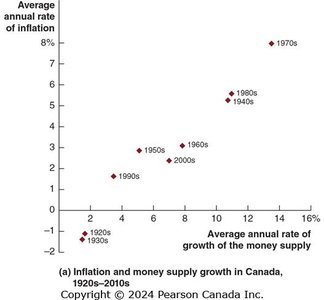

The Quantity Theory of Money

The quantity theory of money links the money supply to the price level and economic output. The core equation is:

M: Money supply

V: Velocity of money (average number of times each dollar is spent per year)

P: Price level

Y: Real output (GDP)

If velocity (V) is constant, changes in the money supply (M) directly affect nominal GDP (P × Y). The theory predicts that sustained money supply growth above real output growth leads to inflation:

Empirical evidence shows a positive relationship between money supply growth and inflation over long periods.

High Rates of Inflation: Hyperinflation

Hyperinflation occurs when inflation exceeds 50% per month, typically triggered by governments financing deficits through excessive money creation. This erodes trust in the currency, causing velocity to spike and prices to soar uncontrollably. Historical examples include Germany in the 1920s and Zimbabwe in the 2000s.

Fiat money systems depend on public confidence. Once trust collapses, the value of money can evaporate rapidly, as seen in episodes of hyperinflation.

Additional info: The notes above expand on the original content by providing definitions, formulas, and historical context, ensuring a comprehensive and self-contained study guide for macroeconomics students.