Back

BackMoney, Banks, and the Federal Reserve System: Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Money, Banks, and the Federal Reserve System

Introduction

This chapter explores the nature and functions of money, how money is measured and created in the United States, the structure and role of the Federal Reserve System, and the relationship between money supply and inflation. Understanding these concepts is essential for analyzing macroeconomic policy and financial stability.

What Is Money, and Why Do We Need It?

Definition and Functions of Money

Money is any asset that people are generally willing to accept in exchange for goods and services or for payment of debts. It is a fundamental invention that facilitates trade and economic development.

Medium of Exchange: Money is widely accepted as payment for goods and services, eliminating the inefficiencies of barter systems.

Unit of Account: Money provides a standard measure of value, making it easier to compare prices and record debts.

Store of Value: Money allows individuals to transfer purchasing power from the present to the future. Its liquidity makes it especially effective in this role.

Standard of Deferred Payment: Money enables transactions to be settled over time, as its value is expected to remain relatively stable.

Example: In a barter economy, exchanging shoes for bread requires a double coincidence of wants. Money solves this problem by serving as a universally accepted medium.

Characteristics of Good Money

Acceptable to most people

Standardized quality

Durable

Valuable relative to weight

Divisible for transactions of varying sizes

Types of Money

Commodity Money: Has intrinsic value (e.g., gold, silver, cowrie shells, cigarettes in prisons).

Fiat Money: Authorized by governments or central banks, has no intrinsic value, and is not backed by a commodity. Its value depends on public confidence.

Advantages of Fiat Money: Flexibility for central banks; Disadvantages: Relies on public trust.

How Is Money Measured in the United States Today?

Definitions of the Money Supply

The money supply is measured using two main aggregates:

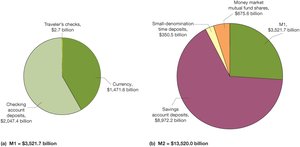

M1: Currency in circulation, checking account deposits, and traveler’s checks.

M2: Includes M1 plus savings deposits, small-denomination time deposits, money market deposit accounts, and noninstitutional money market fund shares.

Example: As of June 2017, M1 was $3,621.7 billion, and M2 was $13,520.0 billion.

Debit and Credit Cards

Debit Cards: Access checking accounts directly, but the card itself is not money.

Credit Cards: Provide short-term loans; transactions are not complete until the loan is repaid. Credit cards are not considered money.

Are Bitcoins Money?

Bitcoins are a decentralized form of e-money, not issued by any government or firm. While they can be traded and used for some transactions, they are not currently included in official measures of the money supply.

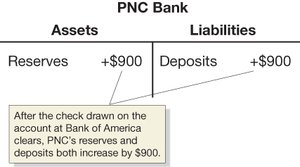

How Do Banks Create Money?

The Role of Banks

Banks are profit-seeking firms that play a critical role in the money supply by accepting deposits and making loans. They operate under a fractional reserve system, keeping only a fraction of deposits as reserves.

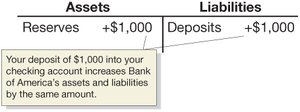

Bank Balance Sheets

A bank’s balance sheet lists assets (e.g., reserves, loans, securities) and liabilities (e.g., deposits). The difference is the bank’s net worth.

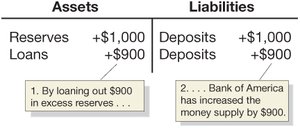

Required and Excess Reserves

Required Reserves: The minimum reserves a bank must hold, set by the required reserve ratio (e.g., 10%).

Excess Reserves: Reserves held above the required minimum.

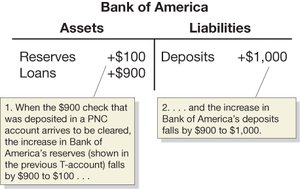

Money Creation Process

When a deposit is made, the bank keeps a fraction as reserves and lends out the rest, creating new deposits in the banking system. This process multiplies the initial deposit throughout the economy.

Simple Deposit Multiplier

The simple deposit multiplier is given by:

For a 10% reserve ratio, the multiplier is 10. In reality, the actual multiplier is lower due to excess reserves and currency held by the public.

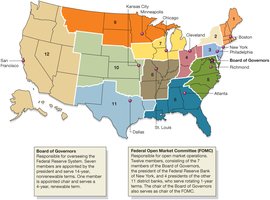

The Federal Reserve System

Structure and Functions

The Federal Reserve (the Fed) is the central bank of the United States, established in 1914 to prevent bank panics and manage the money supply. It consists of 12 regional Federal Reserve Banks and a Board of Governors in Washington, D.C.

Bank Runs and Panics

A bank run occurs when many depositors withdraw funds simultaneously. If widespread, this leads to a bank panic. The Fed acts as a lender of last resort to prevent such crises.

Federal Deposit Insurance Corporation (FDIC)

Established in 1934, the FDIC insures deposits up to a set limit, reducing the risk of bank runs.

Monetary Policy Tools

Open Market Operations: Buying and selling Treasury securities to influence the money supply.

Discount Policy: Setting the discount rate for loans to banks.

Reserve Requirements: Changing the required reserve ratio.

The Shadow Banking System and the Financial Crisis

Securitization

Securitization is the process of transforming loans into securities that can be traded. This development allowed banks to sell loans and transfer risk.

The Shadow Banking System

Non-bank financial firms (investment banks, money market mutual funds, hedge funds) became major sources of credit but were less regulated and more leveraged, making them vulnerable to runs.

The Financial Crisis of 2007-2009

The collapse of major investment banks led to a credit crunch and recession. The Fed responded with emergency measures, including the Troubled Asset Relief Program (TARP).

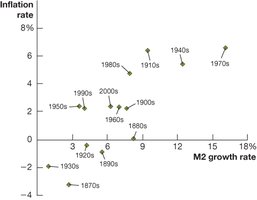

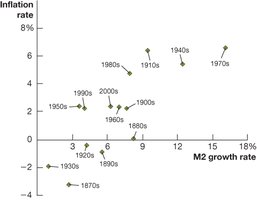

The Quantity Theory of Money

The Quantity Equation

The quantity theory of money links the money supply to the price level and output:

M: Money supply

V: Velocity of money

P: Price level

Y: Real output

Inflation and Money Growth

Assuming constant velocity, the theory predicts:

If the money supply grows faster than real GDP, inflation results; if slower, deflation occurs.

Hyperinflation

Hyperinflation is extremely high inflation (over 50% per month), usually caused by rapid money supply growth far exceeding real output growth. Historical examples include Zimbabwe in the 2000s and Germany in the 1920s.

Summary Table: Key Concepts

Concept | Definition | Example/Application |

|---|---|---|

Medium of Exchange | Asset accepted for payment | U.S. dollar bills |

Commodity Money | Money with intrinsic value | Gold coins |

Fiat Money | Money by government decree | Modern paper currency |

M1 | Currency + checking deposits + traveler’s checks | Used for daily transactions |

M2 | M1 + savings, time deposits, money market funds | Broader measure of money |

Simple Deposit Multiplier | 1 / Required Reserve Ratio | 10 for a 10% ratio |

Open Market Operations | Fed buys/sells Treasury securities | Buying increases money supply |

Quantity Theory of Money | Links money supply to price level | Explains long-run inflation |

Additional info: These notes expand on the textbook content with definitions, examples, and formulas to provide a comprehensive overview suitable for exam preparation in a college-level macroeconomics course.