Back

BackMoney, Monetary Policy, and the Bank of Canada: A Study Guide

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Money, Monetary Policy, and the Bank of Canada

Introduction

This study guide explores the nature and functions of money, the role of bonds, the determination of interest rates, the supply of money, and the mechanisms and challenges of monetary policy in Canada. It is structured to provide a comprehensive overview suitable for macroeconomics students, focusing on the Bank of Canada’s role in steering the economy through monetary policy.

Part 1: Money

Functions and Forms of Money

Money is a fundamental concept in macroeconomics, serving as the primary medium for economic transactions. It is defined by its three main functions:

Medium of Exchange: Money is widely accepted as payment for goods and services, solving the barter problem of the double coincidence of wants.

Unit of Account: Money provides a standard measure for pricing goods and services.

Store of Value: Money allows individuals to transfer purchasing power from the present to the future.

Forms of money include:

Commodity Money: Saleable products with alternative uses (e.g., gold, silver).

Convertible Paper Money: Paper money exchangeable for a commodity (e.g., gold).

Fiat Money: Currency with value by government decree, not backed by a physical commodity.

Deposit Money: Demand deposits in bank accounts, accessible via cheques, debit cards, or e-transfers.

Money vs. Bonds

Individuals choose between holding money and bonds based on liquidity and returns:

Money: Most liquid asset, pays no interest but is readily accepted for transactions.

Bonds: Financial assets that pay interest but are less liquid and subject to price risk.

The interest rate is the opportunity cost of holding money instead of bonds. The yield on a bond is the percentage return, which depends on the bond’s price, fixed payments, and time period.

Bond Prices and Interest Rates

Bond prices and market interest rates are inversely related:

When interest rates rise, bond prices fall.

When interest rates fall, bond prices rise.

The present value (price) of a bond is calculated as:

) \text{ available in } n \text{ years}}{(1 + \text{Interest Rate})^n}$

For a perpetuity bond (pays a fixed amount forever):

\text{ amount/year}}{\text{Interest Rate}}$

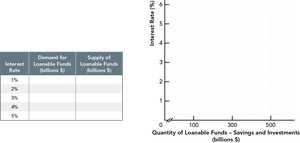

The Loanable Funds Market

Long-run interest rates are determined in the loanable funds market, where savers supply funds and borrowers demand them. The equilibrium interest rate is set by the interaction of these forces.

Part 2: The Supply of Money

Money Creation in the Banking System

In a fractional-reserve banking system, money supply consists of currency and demand deposits. The Bank of Canada issues currency, while commercial banks create money by making loans and generating demand deposits.

M1+: Currency in circulation plus demand deposits.

M2+: M1+ plus other less liquid deposits.

Role of the Bank of Canada

The Bank of Canada is the central bank, responsible for:

Issuing currency

Acting as banker to commercial banks and the government

Lender of last resort

Conducting monetary policy to achieve steady growth, full employment, and stable prices

Money Supply Determinants

The supply of money is influenced by the quantity of loans and demand deposits created by banks. Higher interest rates make loans more profitable, encouraging banks to lend more and increase the money supply.

Modern Money Supply Models

Central banks no longer attempt to control the money supply directly, as it is largely determined by the behavior of consumers, businesses, and commercial banks. The money supply changes with every decision to spend, save, or borrow.

Part 3: Monetary Policy and the Bank of Canada

Monetary Policy Objectives

The Bank of Canada uses monetary policy to achieve:

Steady economic growth

Full employment

Stable prices (inflation control target: 1–3%, aiming for 2%)

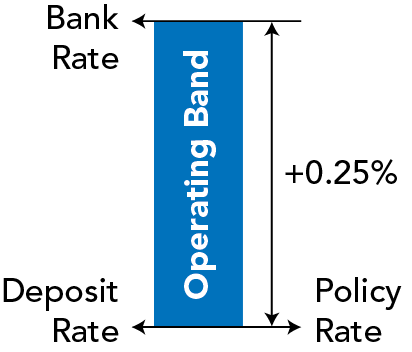

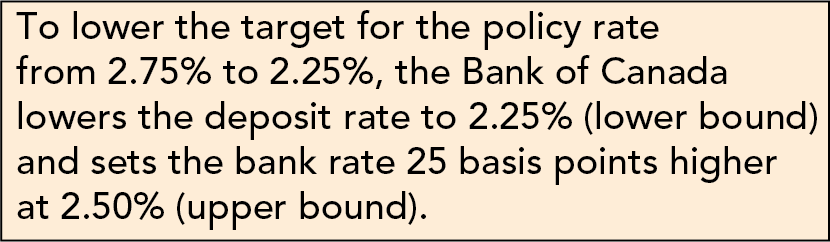

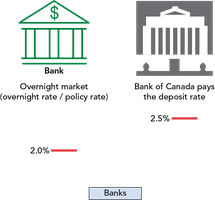

Monetary Policy Tools: The Operating Band

The main tool is the overnight rate—the interest rate banks charge each other for one-day loans. The Bank of Canada sets a target for this rate and uses the operating band, defined by the deposit rate (lower bound) and bank rate (upper bound), to guide it.

To change the policy rate, the Bank of Canada adjusts both the deposit and bank rates by the same amount.

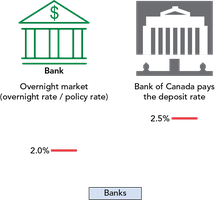

Arbitrage and the Overnight Rate

Arbitrage ensures the overnight rate stays near the deposit rate. If the overnight rate rises above the deposit rate, banks lend in the overnight market; if it falls below, they borrow and deposit at the Bank of Canada, pushing rates back toward equilibrium.

Transmission of Monetary Policy

Changes in the policy rate affect other interest rates (e.g., prime rate, consumer loans, mortgages) in the same direction, influencing aggregate demand and the broader economy.

Part 4: Transmission Mechanisms of Monetary Policy

Aggregate Demand Transmission Mechanisms

Monetary policy affects aggregate demand (AD = C + I + G + X – IM) through:

Domestic Transmission Mechanism: Lower interest rates increase consumption and investment; higher rates decrease them.

International Transmission Mechanism: Lower rates depreciate the Canadian dollar, boosting net exports; higher rates appreciate the dollar, reducing net exports.

Expansionary and Contractionary Monetary Policy

Expansionary Policy: Lower interest rates to correct a recessionary gap, increasing aggregate demand, reducing unemployment, and increasing inflation.

Contractionary Policy: Raise interest rates to correct an inflationary gap, decreasing aggregate demand, increasing unemployment, and reducing inflation.

Time Lags and Policy Challenges

The effects of monetary policy can take up to two years to fully materialize. This lag, combined with changing economic conditions, makes monetary policy difficult to implement effectively.

Part 5: Challenges of Monetary Policy

Transmission Breakdowns

During a balance sheet recession, individuals and businesses focus on paying down debt rather than borrowing or spending, reducing the effectiveness of lower interest rates. The 2008–2009 Global Financial Crisis is an example, where falling asset prices led to reduced spending and saving.

Quantitative Easing

To counteract transmission breakdowns, central banks use quantitative easing—buying large quantities of government bonds and financial assets to lower long-term interest rates and encourage lending and spending.

Inflation Targeting and Expectations

The Bank of Canada’s 2% inflation target anchors expectations, making prices more predictable and supporting smart economic choices. However, once inflation expectations rise, they are difficult to lower, and unpredictable inflation can disrupt investment and economic stability.

Summary Table: Key Concepts

Concept | Definition | Example/Application |

|---|---|---|

Money | Medium of exchange, unit of account, store of value | Currency, demand deposits |

Bond | Financial asset paying fixed interest | Government bond, corporate bond |

Interest Rate | Cost of borrowing or opportunity cost of holding money | Prime rate, overnight rate |

Monetary Policy | Central bank actions to influence economy via interest rates/money supply | Bank of Canada adjusting overnight rate |

Quantitative Easing | Central bank buys assets to lower long-term rates | Bank of Canada buying government bonds |

Additional info: This guide expands on the original slides by providing definitions, formulas, and examples for all major concepts, and by logically grouping fragmented points for clarity and completeness.