Back

BackMoney, the Federal Reserve, and the Interest Rate: Structured Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Money, the Federal Reserve, and the Interest Rate

An Overview of Money

Money is a fundamental concept in macroeconomics, serving as the backbone of modern economies. It fulfills three primary functions: a means of payment, a store of value, and a unit of account.

Means of Payment (Medium of Exchange): Money is what sellers accept and buyers use to pay for goods and services, facilitating trade and eliminating the inefficiencies of barter systems, which require a double coincidence of wants.

Store of Value: Money allows individuals to transport purchasing power across time periods. Its liquidity makes it easily exchangeable, but its value can decrease if prices rise (inflation).

Unit of Account: Money provides a standard unit for quoting prices, enabling consistent valuation of goods and services.

Key Terms: barter, medium of exchange, liquidity property of money, store of value, unit of account.

Example: In the 19th century, rolls of red feathers from the Scarlet Honeyeater bird were used as currency in Pacific Islands, illustrating commodity money.

Commodity and Fiat Monies

Money can be classified based on its intrinsic value and government backing.

Commodity Monies: Items used as money that have intrinsic value in other uses (e.g., gold, feathers).

Fiat (Token) Money: Items designated as money by government decree, but intrinsically worthless (e.g., paper currency).

Legal Tender: Money that must be accepted in settlement of debts by law.

Currency Debasement: Occurs when the supply of money increases rapidly, reducing its value.

Measuring the Supply of Money in the United States

The money supply is measured using different aggregates, reflecting varying degrees of liquidity.

M1 (Transactions Money): Money that can be directly used for transactions.

M2 (Broad Money): Includes M1 plus savings accounts, money market accounts, and other near monies.

Beyond M2: Some definitions include available credit on credit cards, but for most purposes, "money" refers to M1.

How Banks Create Money

Banks play a crucial role in money creation through the process of accepting deposits and making loans.

Historical Perspective: Goldsmiths issued receipts backed by gold, which became a form of paper money. The modern system evolved from this practice.

Run on a Bank: Occurs when many depositors demand their money simultaneously, threatening the bank's solvency.

Required Reserve Ratio: The percentage of deposits banks must keep as reserves, imposed by regulation.

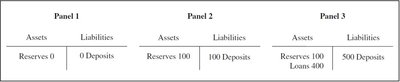

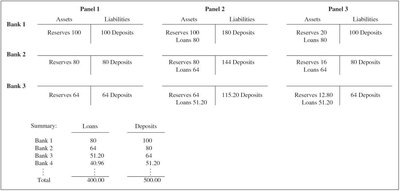

Example: The process of money creation is illustrated by the expansion of deposits and loans in a bank's balance sheet.

Example: In a multi-bank system, the process continues as loans are deposited in other banks, further increasing the money supply.

The Money Multiplier

The money multiplier quantifies how an increase in bank reserves leads to a greater increase in the money supply.

Formula:

Excess Reserves: The difference between a bank's actual reserves and required reserves.

The Federal Reserve System

The Federal Reserve (the Fed) is the central bank of the United States, responsible for monetary policy and regulation of the banking system.

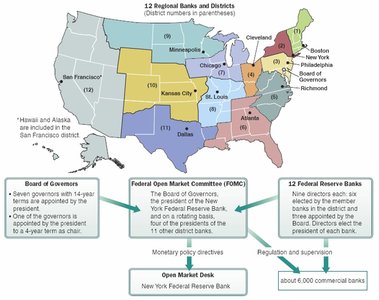

Structure: The Fed consists of the Board of Governors, 12 regional Federal Reserve Banks, and the Federal Open Market Committee (FOMC).

Independence: The Fed operates independently from the executive and legislative branches of government.

FOMC: Sets goals for the money supply and interest rates, directing open market operations.

Example: The map and diagram show the organization of the Federal Reserve System, including its regional banks and governing bodies.

Functions of the Federal Reserve

The Fed performs several key functions in the economy:

Control of Money Supply: The Fed regulates the amount of money in circulation.

Bankers' Bank: Provides services to commercial banks, including clearing payments and lending in times of crisis (lender of last resort).

Regulation: Oversees banking practices and standards.

Management of Exchange Rates: Handles foreign exchange reserves and exchange rate policy.

How the Federal Reserve Controls the Interest Rate

The Fed uses several tools to influence interest rates and the money supply:

Open Market Operations: Buying and selling government securities to affect reserves and interest rates.

Reserve Requirement Ratio: Changing the required reserves for banks.

Discount Rate: The interest rate charged to banks for borrowing from the Fed.

Moral Suasion: Informal influence on banks' lending behavior.

The Demand for Money

The demand for money is determined by the size of transactions and the opportunity cost of holding money (the interest rate).

Transaction Motive: Holding money to buy goods and services.

Speculation Motive: Holding money or bonds based on expected changes in interest rates.

Precautionary Motive: Holding money for emergencies.

Interest Rates and Security Prices

Interest rates and security prices are inversely related. When interest rates rise, the prices of existing securities fall, and vice versa.

Bonds: Issued with a face value and fixed payments (coupons).

Market Dynamics: Investors may prefer bonds when interest rates are high, hoping to sell them when rates fall.

The Equilibrium Interest Rate

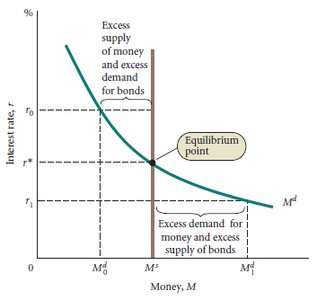

The equilibrium interest rate is determined in the money market, where the quantity of money demanded equals the quantity supplied.

Money Market Equilibrium: At equilibrium, the supply of money equals the demand for money, and the supply of bonds equals the demand for bonds.

Fed's Role: By adjusting the money supply, the Fed can influence the equilibrium interest rate.

Example: The graph shows how changes in the money supply affect the equilibrium interest rate.

Expanded Fed Activities Beginning in 2008

Since 2008, the Fed has expanded its activities, including purchasing mortgage-backed securities and long-term government bonds to stabilize financial markets.

New Tools: The Fed began paying interest on bank reserves, leading to excess reserves above zero.

Traditional Tools: Open market operations, reserve requirements, and the discount rate became less effective.

Appendix: The Various Interest Rates in the U.S. Economy

Interest rates vary by maturity and risk. The term structure of interest rates describes the relationship among rates for securities of different maturities.

Expectations Theory: The 2-year rate equals the average of the current 1-year rate and the expected 1-year rate a year from now.

Types of Interest Rates: Treasury bill rate, government bond rate, federal funds rate, commercial paper rate, prime rate, corporate bond rates (AAA, etc.).

Key Equations

Review Terms: barter, commodity monies, currency debasement, discount rate, excess reserves, Federal Open Market Committee (FOMC), Federal Reserve Bank (the Fed), fiat money, legal tender, lender of last resort, liquidity property of money, M1, M2, medium of exchange, money multiplier, near monies, Open Market Desk, open market operations, required reserve ratio, reserves, run on a bank, store of value, unit of account.