Back

BackPrice Levels and the Exchange Rate in the Long Run

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Price Levels and the Exchange Rate in the Long Run

Chapter Overview

This chapter explores the determinants of exchange rates in the long run, focusing on the concepts of Purchasing Power Parity (PPP), the law of one price, the monetary approach to exchange rates, and the real exchange rate. It also discusses the empirical shortcomings of PPP and the influence of monetary and real factors on exchange rates.

The Law of One Price and Purchasing Power Parity (PPP)

Law of One Price

The law of one price states that identical goods should sell for the same price in different competitive markets when there are no transportation costs or trade barriers. Arbitrage ensures that price differences are eliminated as buyers and sellers exploit profit opportunities until prices converge.

Example: If a pizza costs $20 in one location and $40 in another, buyers will flock to the cheaper option, pushing its price up and the expensive one's price down until equilibrium is reached.

Purchasing Power Parity (PPP)

Purchasing Power Parity (PPP) extends the law of one price to baskets of goods across countries. It posits that exchange rates adjust so that identical baskets of goods have the same price when expressed in a common currency.

Absolute PPP: Exchange rates equal the ratio of average price levels between countries.

Relative PPP: Changes in exchange rates reflect changes in relative price levels (inflation rates) between countries.

Formulas:

Absolute PPP:

Relative PPP:

Example: If the price level in the U.S. is $200 and in Canada is C$400, PPP predicts the exchange rate should be C$2/US$1.

The Monetary Approach to Exchange Rates

Monetary Model and PPP

The monetary approach uses monetary factors to predict long-run exchange rates, assuming PPP holds. It states that exchange rates are determined by the relative supply and demand for real monetary assets across countries.

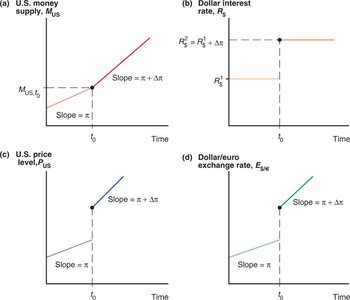

Money Supply: A permanent increase in domestic money supply raises the domestic price level and causes proportional currency depreciation.

Interest Rates: Higher domestic interest rates lower real money demand, raise prices, and depreciate the currency.

Output: Higher domestic output increases real money demand, lowers prices, and appreciates the currency.

Equation:

Inflation and Money Growth: A higher money growth rate leads to higher inflation and, via PPP, a higher rate of currency depreciation.

The Fisher Effect

The Fisher effect links nominal interest rates and expected inflation. In the long run, a rise in expected inflation leads to an equal rise in nominal interest rates.

Equation:

Where is the nominal interest rate, is the real interest rate, and is expected inflation.

Shortcomings of PPP

Empirical Evidence and Deviations

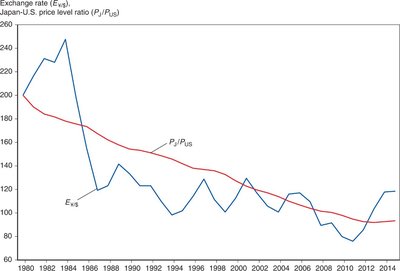

Absolute PPP rarely holds in practice due to persistent price differences across countries. Relative PPP is more consistent with data but still performs poorly in predicting exchange rates.

Reasons for Deviations:

Trade barriers and nontradable goods (e.g., services, perishable goods)

Imperfect competition and price discrimination

Differences in how price baskets are measured

Example: The Big Mac Index uses the price of a McDonald's Big Mac to compare PPP across countries, but differences in taxes, rents, and wages cause deviations from market exchange rates.

The Real Exchange Rate Approach

Definition and Importance

The real exchange rate measures the relative price of goods between countries, adjusting for nominal exchange rates and price levels. It is a key indicator of international competitiveness.

Formula:

A real depreciation means domestic goods become cheaper relative to foreign goods, boosting exports.

A real appreciation means domestic goods become more expensive, reducing exports.

Determinants of the Real Exchange Rate

Relative Demand: Higher demand for domestic goods appreciates the real exchange rate.

Relative Supply: Higher productivity or output increases supply, depreciating the real exchange rate.

Both monetary and real factors influence nominal exchange rates in the long run.

Interest Rate Differentials and Real Interest Parity

Interest Rate Parity and Exchange Rates

Interest rate differentials across countries reflect expected changes in exchange rates and inflation differentials. The real interest parity condition states that differences in real interest rates are equal to expected changes in the real exchange rate.

Equation:

Summary Table: Effects of Money Market and Output Market Changes

Change | Effect on Long-Run Nominal Dollar/Euro Exchange Rate (E24/20) |

|---|---|

Increase in U.S. money supply level | Proportional increase (nominal depreciation of $) |

Increase in European money supply level | Proportional decrease (nominal depreciation of euro) |

Increase in U.S. money supply growth rate | Increase (nominal depreciation of $) |

Increase in European money supply growth rate | Decrease (nominal depreciation of euro) |

Increase in demand for U.S. output | Decrease (nominal appreciation of $) |

Increase in demand for European output | Increase (nominal appreciation of euro) |

Output supply increase in the United States | Ambiguous |

Output supply increase in Europe | Ambiguous |

Key Takeaways

PPP is a long-run anchor, but not a short-run trading rule.

Absolute PPP fails due to nontradables, taxes, and barriers; relative PPP links inflation differentials to exchange rate trends.

The real exchange rate is crucial for understanding international competitiveness.

Interest rate differentials reflect both inflation expectations and real exchange rate movements.

Tariffs and trade policies can create persistent deviations from PPP.