Back

BackProduction and Economic Growth: Determinants, Policies, and Global Perspectives

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Production and Growth

Introduction to Economic Growth

Economic growth refers to the increase in the amount of goods and services produced per head of the population over a period of time. It is a central topic in macroeconomics because it determines the long-term standard of living in a country.

Living standards vary widely across countries, with rich countries having much higher average incomes than poor countries.

Growth rates differ significantly between countries and over time, influencing how quickly living standards improve.

For example, Canada's real GDP per person has grown by about 2% per year over the past century, doubling every 35 years.

Some countries, like China, have experienced rapid growth, while others, like Zimbabwe, have seen declines in income per person.

Global Growth Experiences

Comparing growth rates and income levels across countries helps illustrate the diversity of economic experiences worldwide.

Income per person in Canada is about three times higher than in China and 6.5 times higher than in India.

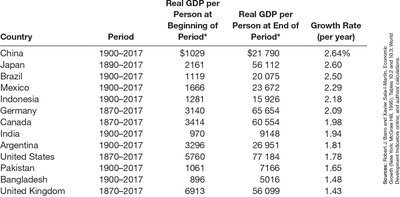

Country | Period | Real GDP per Person at Beginning of Period | Real GDP per Person at End of Period | Growth Rate (per year) |

|---|---|---|---|---|

China | 1900–2017 | $1,029 | $21,790 | 2.64% |

Japan | 1880–2017 | 2,161 | 56,112 | 2.60% |

Brazil | 1900–2017 | 1,119 | 20,075 | 2.50% |

Mexico | 1900–2017 | 1,668 | 25,623 | 2.29% |

Indonesia | 1900–2017 | 1,281 | 15,926 | 2.20% |

Germany | 1870–2017 | 3,140 | 65,654 | 2.09% |

Canada | 1870–2017 | 3,414 | 56,117 | 2.08% |

India | 1900–2017 | 779 | 9,154 | 1.81% |

Argentina | 1900–2017 | 3,286 | 26,981 | 1.81% |

United States | 1870–2017 | 5,760 | 71,187 | 1.80% |

Pakistan | 1900–2017 | 1,061 | 7,166 | 1.65% |

Bangladesh | 1900–2017 | 1,087 | 5,016 | 1.43% |

United Kingdom | 1870–2017 | 6,913 | 56,099 | 1.43% |

Productivity: Its Role and Determinants

Definition and Importance of Productivity

Productivity is the quantity of goods and services produced from each hour of a worker’s time. It is the key determinant of living standards and economic growth.

Higher productivity leads to higher incomes and improved living standards.

Growth in productivity is essential for long-term increases in living standards.

Determinants of Productivity

Physical Capital per Worker: The stock of equipment and structures used to produce goods and services.

Human Capital per Worker: The knowledge and skills workers acquire through education, training, and experience.

Natural Resources per Worker: Inputs provided by nature, such as land, rivers, and mineral deposits.

Technological Knowledge: Society’s understanding of the best ways to produce goods and services.

Economic Growth and Public Policy

Policies to Promote Economic Growth

Governments can influence economic growth through various policies:

Saving and Investment: Encouraging saving and investment increases the capital stock, raising productivity and living standards.

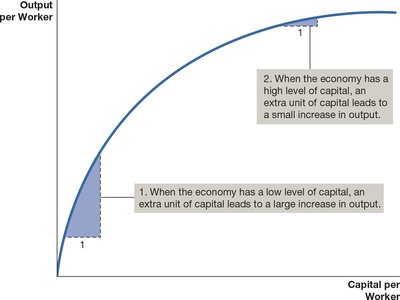

Diminishing Returns and the Catch-Up Effect: As capital increases, the benefit from additional capital decreases (diminishing returns). Poorer countries can grow faster due to the catch-up effect.

Investment from Abroad: Foreign direct investment and foreign portfolio investment can increase a country’s capital stock and productivity.

Education: Investment in human capital is crucial for long-term growth. Education also creates positive externalities.

Health and Nutrition: Healthier workers are more productive, and improvements in health can create a virtuous cycle of growth.

Property Rights and Political Stability: Secure property rights and political stability are essential for a well-functioning market economy.

Free Trade: Outward-oriented policies that promote integration into the world economy can boost growth.

Research and Development: Technological progress, often supported by government policies, is a major driver of long-term growth.

Population Growth: Population growth affects total output, but its impact on living standards depends on how it interacts with other factors of production.

Diminishing Returns and the Catch-Up Effect

The concept of diminishing returns explains why increasing capital leads to smaller increases in output as the capital stock grows. The catch-up effect suggests that poorer countries can grow more rapidly than richer ones because they start with less capital.

Diminishing Returns: The benefit from an extra unit of input declines as the quantity of the input increases.

Catch-Up Effect: Countries that start off poor tend to grow more rapidly than those that start off rich.

Population Growth: Effects and Debates

Stretching Natural Resources: Large populations can strain resources, as argued by Thomas Malthus.

Diluting Capital Stock: Rapid population growth can reduce capital per worker, lowering productivity.

Promoting Technological Progress: Some economists argue that larger populations can drive innovation and economic prosperity.

Conclusion: The Importance of Long-Run Growth

A country’s standard of living depends on its ability to produce goods and services. Policymakers aiming to improve living standards must focus on increasing productivity through sound economic policies. The role of government in promoting growth is debated, but maintaining property rights and political stability is universally recognized as essential.