Back

BackThe Economics of Health Care: Macroeconomic Perspectives and Policy Debates

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 5: The Economics of Health Care

5.1 The Improving Health of People in the United States

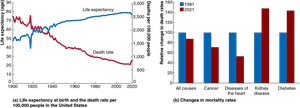

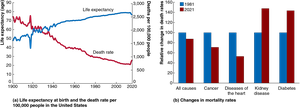

The health of Americans has improved dramatically over the past two centuries, with significant increases in life expectancy and reductions in death rates. Economists study health care to understand the factors driving these trends and the implications for economic policy.

Health care: Goods and services intended to maintain or improve health, including drugs, doctor consultations, and surgeries.

Key factors in improved health outcomes:

Improvements in nutrition

Public health initiatives (sanitation, food safety)

Medical advances in prevention and treatment

Feedback loop: Better health leads to higher incomes, which further improves health

Trends: Life expectancy has risen, while death rates (especially from cardiovascular disease) have fallen. However, deaths from obesity-related illnesses have increased.

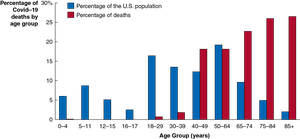

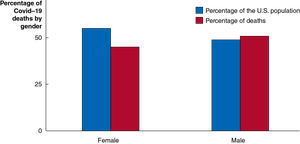

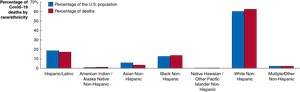

Apply the Concept: The Demographics of Covid-19 Mortality

Covid-19 mortality varied significantly by age, gender, and racial/ethnic group, highlighting disparities in health outcomes and access to care.

Older adults were most affected due to weaker immune systems and living conditions (e.g., nursing homes).

Men had higher mortality rates, partly due to lower vaccination rates.

Racial and ethnic disparities were influenced by vaccination rates, access to health care, socioeconomic status, and occupational exposure.

5.2 Health Care Around the World

Health care systems differ globally in terms of provision, payment, and outcomes. The U.S. system is unique for its reliance on private providers and insurance, with significant government involvement through programs like Medicare and Medicaid.

Health insurance: A contract where buyers pay premiums in exchange for coverage of medical expenses.

Types of insurance payments:

Fee-for-service: Payment for each service provided

Health Maintenance Organizations (HMOs): Flat fee per patient

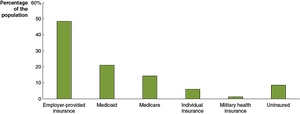

In 2021, 49% of Americans had employer-based insurance, 6% purchased insurance directly, 37% had government insurance, and 9% were uninsured.

Reasons for being uninsured:

Affordability

Perceived lack of need

Cost-benefit concerns

The Affordable Care Act (ACA) reduced the uninsured rate through subsidies and mandates.

Health care is a major and growing sector of the U.S. economy, employing more workers than any other industry in most states.

Comparing Health Care Systems

Canada: Single-payer system, government-funded insurance, private care providers.

Japan: Universal insurance, mandatory enrollment, significant copayments.

UK: Socialized medicine, government owns hospitals and employs doctors, some private insurance.

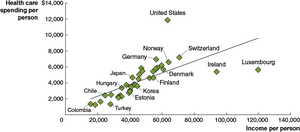

Health care is a normal good: higher income leads to higher spending, but the U.S. spends a larger share of income on health care than other countries.

Cross-Country Comparisons

Challenges include data inconsistencies, differences in care quality, lifestyle choices, and consumer preferences.

5.3 Information Problems and Externalities in the Market for Health Care

The health care market is affected by asymmetric information, leading to market failures such as adverse selection and moral hazard. Externalities also play a significant role in health care consumption and provision.

Asymmetric information: One party has more or better information than the other, leading to inefficient outcomes.

Adverse selection: Those most likely to use insurance are most likely to buy it, raising premiums and excluding healthier individuals.

Moral hazard: Insured individuals may consume more care or take greater risks, increasing costs.

Principal-agent problem: Doctors (agents) may act in their own interests rather than those of insurance companies (principals).

Methods to reduce adverse selection and moral hazard include mandates, deductibles, coinsurance, and standardized payments.

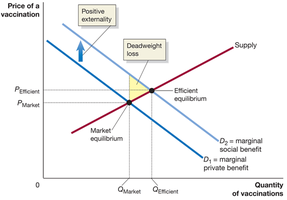

Externalities in Health Care

Positive externalities: Vaccinations benefit others by reducing disease spread; healthy populations benefit employers.

Negative externalities: Poor health choices increase costs for others through higher premiums and taxes.

5.4 The Debate Over Health Care Policy in the United States

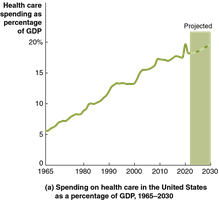

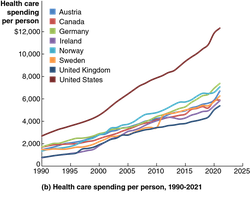

The U.S. spends more per person on health care than any other country, and costs continue to rise. Policy debates focus on how to control costs while maintaining or improving coverage and quality.

Trends: Health care spending as a share of national income and per person has risen faster in the U.S. than in other high-income countries.

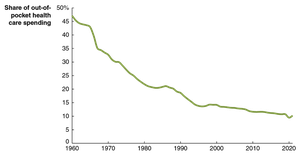

Out-of-pocket spending has declined, increasing the burden on government budgets.

Employer-based insurance may disadvantage U.S. firms, but government provision would likely shift costs to payroll taxes.

Why Are Health Care Costs Rising?

Administrative costs, prescription drug prices, malpractice lawsuits, and uninsured patients contribute, but do not fully explain the rise.

Cost disease: Service sector productivity gains lag behind other sectors, but wages rise to retain workers.

Aging population and medical advances: Older populations require more care; technology keeps people alive longer.

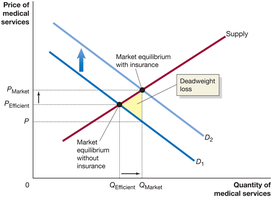

Distorted incentives: Insurance disconnects payment from service, leading to overconsumption and deadweight loss.

Health Insurance vs. Other Insurance

Health insurance often covers routine, predictable events, unlike other insurance types that cover rare adverse events.

Early health insurance programs functioned as prepaid medical care, encouraging overuse.

Policy Debates and Reforms

Universal coverage proposals (Truman, Clinton, Obama) have faced political resistance.

The Affordable Care Act (ACA) introduced mandates, marketplaces, employer requirements, Medicaid expansion, and new taxes.

Market-based reforms aim to reduce tax incentives for employer-based insurance and encourage more efficient spending.

Medicare for All and Public Option

Medicare for All: Single-payer system, universal coverage, cost savings, but high cost and reduced flexibility.

Public option: Competes with private insurance, potentially lowers premiums, but may threaten private insurers.

Conclusions About Health Care

With health care projected to consume nearly 20% of national income by 2030, controlling costs is essential. The challenge is to balance cost reductions with maintaining quality and access, making health care policy a persistent topic of debate in macroeconomics.