Back

BackCompetitive Firms and Markets: Perfect Competition and Economic Well-Being

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Perfect Competition

Definition and Characteristics

Perfect competition is a market structure where buyers and sellers are price takers, meaning no individual participant can influence the market price. The demand curve facing a firm in perfect competition is horizontal, indicating that the firm can sell any quantity at the market price but nothing above it.

Large Number of Buyers and Sellers: No single firm or buyer can affect the market price.

Identical Products: All firms sell homogeneous products perceived as identical by buyers.

Full Information: Market participants have complete knowledge of prices and product characteristics.

Negligible Transaction Costs: Trading is easy and costless; buyers can switch suppliers without difficulty.

Free Entry and Exit: Firms can enter or leave the market freely in the long run.

Markets may deviate from perfect competition but can still be highly competitive if buyers and sellers are price takers.

Competition in the Short Run

Profit Maximization and Output Decision

In the short run, a competitive firm decides how much to produce to maximize profit. The profit-maximizing condition is:

Marginal Revenue equals Marginal Cost:

For a competitive firm, (market price).

Thus, the firm produces the quantity where .

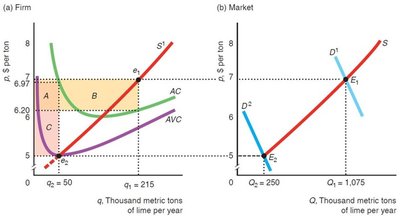

Example: If the market price is p = 8$.

Shutdown Decision

The firm must decide whether to produce or shut down:

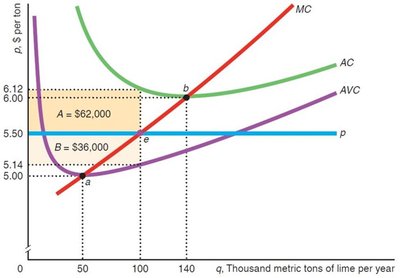

If revenue covers variable costs (), the firm operates.

If price is below average variable cost (), the firm shuts down.

The minimum of the AVC curve is the shutdown point.

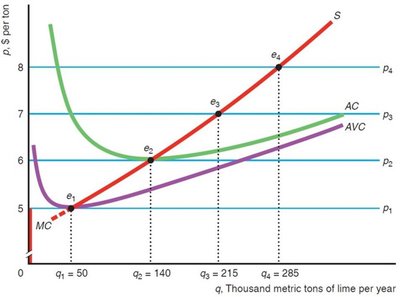

Short-Run Firm Supply Curve

The firm's short-run supply curve is its marginal cost curve above the minimum AVC.

Short-Run Market Supply Curve

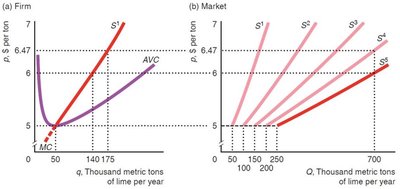

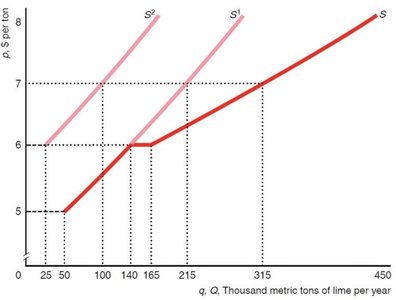

The market supply curve is the horizontal sum of individual firm supply curves. With identical firms, market supply is flatter than individual supply. With differing firms, the market supply curve reflects the sum of their supply curves.

Short-Run Competitive Equilibrium

Short-run equilibrium is found where the market supply and demand curves intersect. At equilibrium, firms maximize profit and no firm wants to change its output.

Competition in the Long Run

Long-Run Profit Maximization and Supply

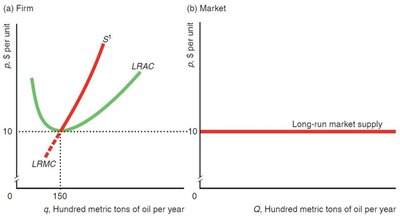

In the long run, firms maximize profit by choosing output where . Firms shut down if revenue is less than avoidable cost ().

The firm's long-run supply curve is its long-run marginal cost curve above the minimum of its long-run average cost curve.

Long-Run Market Supply Curve

With free entry and identical firms, the long-run market supply curve is horizontal at the minimum long-run average cost. If entry is limited or firms differ, the supply curve slopes upward.

Long-Run Competitive Equilibrium

The intersection of long-run supply and demand determines equilibrium. With identical firms and free entry, equilibrium price equals minimum long-run average cost and all firms earn zero profit. A shift in demand changes equilibrium quantity, not price.

Competition Maximizes Economic Well-Being

Surplus Concepts

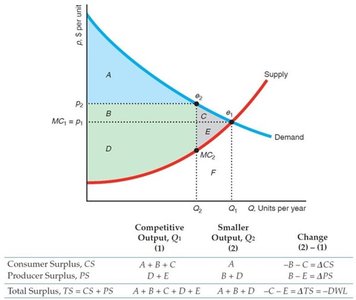

Perfect competition maximizes economic well-being, measured by consumer surplus, producer surplus, and total surplus.

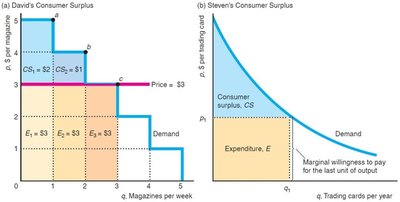

Consumer Surplus (CS): The difference between what consumers are willing to pay and what they actually pay.

Producer Surplus (PS): The difference between the price received and the minimum cost of production.

Total Surplus (TS): The sum of consumer and producer surplus: .

Measuring Consumer Surplus

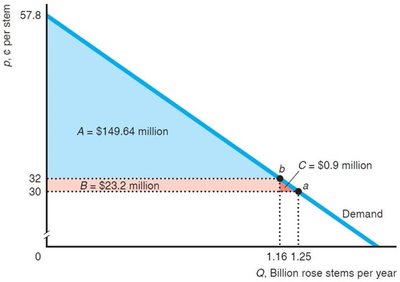

Consumer surplus is the area below the demand curve and above the market price up to the quantity consumed.

Effects of Price Changes on Consumer Surplus

When price rises due to supply shifts or taxes, consumer surplus falls. The loss is the area between the old and new prices under the demand curve.

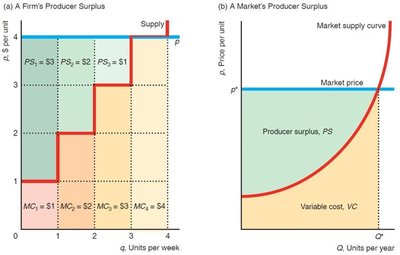

Measuring Producer Surplus

Producer surplus is the area above the supply curve and below the market price up to the quantity produced. It can be used to analyze the effects of cost shocks on profits.

Competition Maximizes Total Surplus

Perfect competition maximizes total surplus. Producing less or more than the competitive output reduces total surplus, creating deadweight loss.

Deadweight Loss (DWL)

Deadweight loss is the net reduction in total surplus from an action that alters market equilibrium, such as producing less than the competitive output. It represents lost gains from trade.

Effects of Government Intervention

Government policies like price ceilings reduce total surplus in competitive markets. A price ceiling below equilibrium causes fewer units to be sold, reducing producer surplus and creating deadweight loss.

Concept | Definition | Formula |

|---|---|---|

Consumer Surplus (CS) | Difference between willingness to pay and actual price | |

Producer Surplus (PS) | Difference between price received and minimum cost | |

Total Surplus (TS) | Sum of consumer and producer surplus | |

Deadweight Loss (DWL) | Loss in total surplus from non-optimal output |