Back

BackCompetitive Markets and Perfect Competition: Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Competitive Markets

Market Structure and Firm Behaviour

Market structure refers to the characteristics of a market that influence the behaviour and performance of firms. These include the number and size of sellers, the degree of product differentiation, the extent of knowledge about competitors, and the freedom of entry and exit.

Market Power: The ability of a firm to influence the price of its product. Firms with little or no market power operate in competitive markets.

Competitive Market: A market where firms have little or no market power. The extreme case is perfect competition, where each firm has zero market power.

Competitive Behaviour: The extent to which firms actively compete for business. Not all competitive behaviour occurs in competitive markets (e.g., MasterCard vs. Visa), and not all firms in competitive markets engage in aggressive behaviour (e.g., wheat farmers).

The Theory of Perfect Competition

Assumptions of Perfect Competition

Perfect competition is an idealized market structure characterized by several key assumptions:

All firms sell a homogeneous product.

Buyers and sellers have perfect information about prices and products.

Each firm’s minimum efficient scale is small relative to total industry output.

There is freedom of entry and exit in the industry.

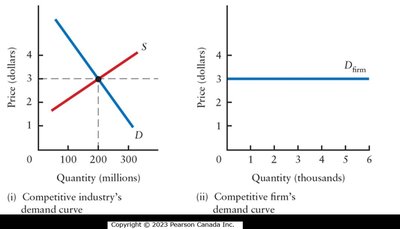

Demand Curve for a Competitive Firm

In a perfectly competitive market, the industry faces a downward-sloping demand curve, but each individual firm faces a perfectly elastic (horizontal) demand curve at the market price. This means the firm can sell any quantity at the market price but cannot influence the price by its own output decisions.

Price Taker: Each firm is a price taker because its output is too small to affect the market price.

Horizontal Demand Curve: The firm’s demand curve is perfectly elastic at the market price.

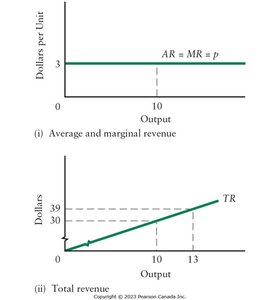

Total, Average, and Marginal Revenue

Revenue concepts are central to understanding firm behaviour in perfect competition:

Total Revenue (TR): The total amount received from sales.

Average Revenue (AR): Revenue per unit sold.

Marginal Revenue (MR): The change in total revenue from selling one more unit.

For a competitive firm, .

Short-Run Decisions in Perfect Competition

Profit Maximization

The objective of the firm is to maximize profits, where:

If , the firm incurs economic losses.

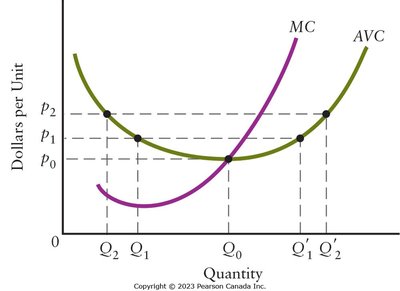

Shut-Down Decision

A firm must decide whether to produce or shut down in the short run:

If the firm produces nothing, it loses an amount equal to its fixed costs.

If it produces, it incurs variable costs in addition to fixed costs.

It should produce if there is some output level where (total variable cost).

Equivalently, the firm should produce if (average variable cost).

The shut-down price is the minimum of the AVC curve. Below this price, the firm will not produce.

Output Decision: How Much to Produce?

If production is worthwhile, the profit-maximizing output is where marginal revenue equals marginal cost:

Produce where (for a competitive firm, ).

If , increase output; if , decrease output.

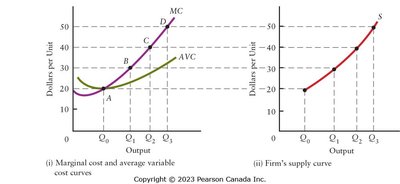

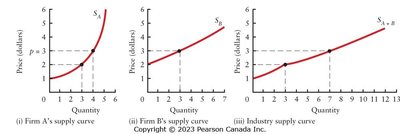

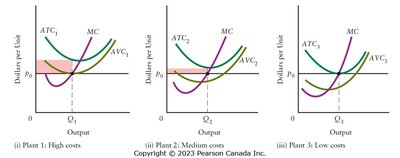

Short-Run Supply Curve

The competitive firm’s short-run supply curve is the portion of its marginal cost curve that lies above the average variable cost curve.

The industry supply curve is the horizontal sum of all firms’ supply curves (i.e., their MC curves above AVC).

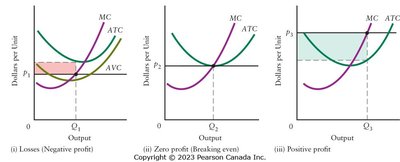

Short-Run Equilibrium

In short-run equilibrium, quantity demanded equals quantity supplied, and each firm maximizes profit given the market price. Firms may make profits, break even, or incur losses.

If , the firm makes losses but may continue to produce if .

If , the firm breaks even (zero economic profit).

If , the firm earns positive economic profit.

Long-Run Decisions in Perfect Competition

Entry and Exit

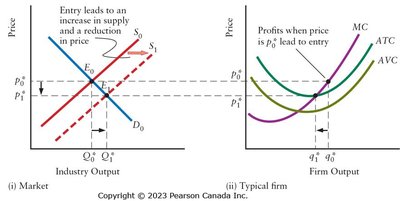

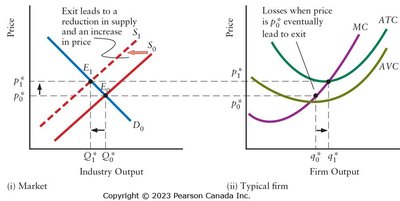

In the long run, firms can enter or exit the industry:

Positive economic profits attract new entrants, increasing supply and lowering price.

Economic losses cause firms to exit, reducing supply and raising price.

Entry and exit continue until firms earn zero economic profit (break-even).

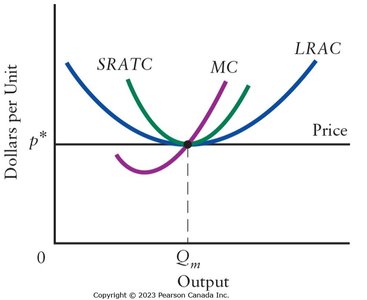

Long-Run Equilibrium

Long-run equilibrium in a competitive industry is characterized by:

Firms earning zero economic profit (break-even price).

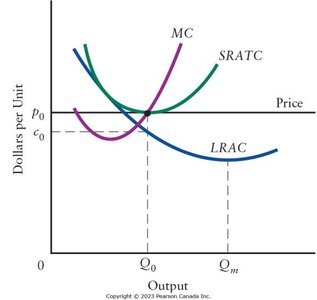

Price equals the minimum point of the long-run average cost (LRAC) curve.

Firms have no incentive to enter or exit.

Each firm is producing at the minimum efficient scale.

Technological Change and Industry Dynamics

Effects of Technological Change

Technological improvements lower costs for new plants, allowing them to earn profits and attract entry. As industry output expands, price falls to the new (lower) average cost. Older, higher-cost plants may exit if they cannot compete.

Declining Industries

When demand for a product continually decreases, the industry contracts. Firms with obsolete equipment may not replace it, and exit is common. Declining industries often result from technological change or the emergence of substitutes (e.g., whale oil replaced by kerosene).

Example: The whaling industry declined due to falling whale populations and the invention of kerosene, a substitute for whale oil. Similarly, the oil industry faces challenges from new energy sources and environmental concerns.