Back

BackEconomic Efficiency, Government Price Setting, and Taxes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Economic Efficiency, Government Price Setting, and Taxes

Introduction

This chapter explores how government interventions such as price controls and taxes affect market outcomes, economic efficiency, and the distribution of surplus among consumers and producers. It also examines the concepts of consumer surplus, producer surplus, and deadweight loss, providing a foundation for understanding the efficiency of competitive markets and the consequences of government policies.

Consumer Surplus and Producer Surplus

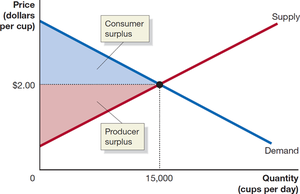

Consumer Surplus

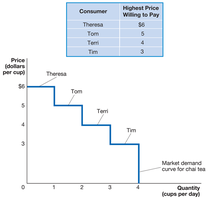

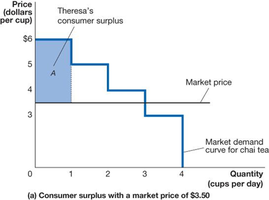

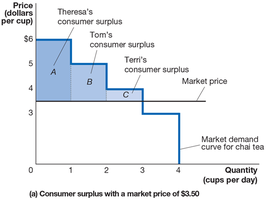

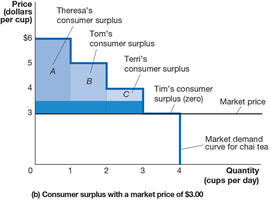

Consumer surplus is the difference between the highest price a consumer is willing to pay for a good or service and the actual price paid. It measures the net benefit to consumers from participating in a market.

Marginal Benefit: The additional benefit to a consumer from consuming one more unit of a good or service.

Consumer surplus is represented graphically as the area below the demand curve and above the market price.

When the price decreases, consumer surplus increases, as more consumers can purchase the good at a lower price.

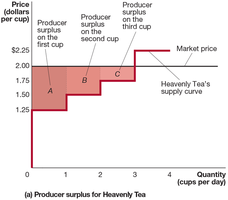

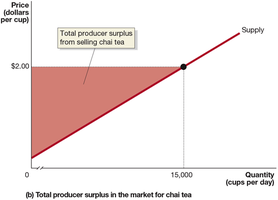

Producer Surplus

Producer surplus is the difference between the lowest price a firm would accept for a good or service (usually the marginal cost of production) and the price it actually receives. It measures the net benefit to producers from participating in a market.

Marginal Cost: The change in a firm’s total cost from producing one more unit of a good or service.

Producer surplus is represented graphically as the area above the supply curve and below the market price.

Economic Surplus

Economic surplus is the sum of consumer surplus and producer surplus. It measures the total net benefit to society from the production and consumption of a good or service.

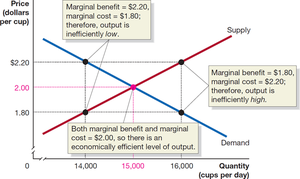

Economic surplus is maximized at the competitive equilibrium, where the quantity supplied equals the quantity demanded.

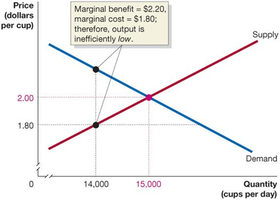

The Efficiency of Competitive Markets

Conditions for Efficiency

A market is considered efficient if:

All trades take place where the marginal benefit to consumers exceeds the marginal cost to producers.

The sum of consumer and producer surplus (economic surplus) is maximized.

Deadweight Loss

Deadweight loss is the reduction in economic surplus resulting from a market not being in competitive equilibrium. It represents the value of trades that do not occur due to inefficiency, such as those caused by price controls or taxes.

At equilibrium, deadweight loss is zero.

When the market is not at equilibrium, deadweight loss is positive, indicating inefficiency.

Government Intervention: Price Floors and Price Ceilings

Price Ceilings

A price ceiling is a legally determined maximum price that sellers may charge. Common examples include rent controls.

Price ceilings set below equilibrium create shortages, as quantity demanded exceeds quantity supplied.

They transfer surplus from producers to consumers but create deadweight loss due to lost transactions.

Price Floors

A price floor is a legally determined minimum price that sellers may receive. Common examples include minimum wages and agricultural price supports.

Price floors set above equilibrium create surpluses, as quantity supplied exceeds quantity demanded.

They transfer surplus from consumers to producers but also create deadweight loss.

Minimum Wage and Rent Control

Minimum wage laws are a form of price floor in the labor market. They can increase incomes for some workers but may reduce employment for others.

Rent controls are a form of price ceiling in the housing market. They can lower rents for some tenants but reduce the quantity and quality of available housing.

The Economic Effect of Taxes

Per-Unit Taxes

Governments often impose per-unit taxes (excise taxes) on goods and services. These taxes shift the supply curve upward by the amount of the tax, increasing the price paid by consumers and reducing the price received by producers.

Taxes create deadweight loss by reducing the quantity traded below the efficient equilibrium level.

Some consumer and producer surplus is converted into government tax revenue, while some is lost as deadweight loss.

Tax Incidence

Tax incidence refers to the actual division of the burden of a tax between buyers and sellers, regardless of who is legally responsible for paying the tax.

The incidence depends on the relative elasticities (slopes) of the demand and supply curves.

If demand is inelastic relative to supply, consumers bear more of the tax burden. If supply is inelastic relative to demand, producers bear more of the burden.

Efficiency of Taxes

A tax is considered more efficient if it raises a given amount of revenue with a smaller deadweight loss (excess burden).

Economists advise policymakers to design taxes that minimize excess burden while achieving revenue goals.

Summary Table: Effects of Price Controls and Taxes

Policy | Market Outcome | Winners | Losers | Deadweight Loss? |

|---|---|---|---|---|

Price Ceiling (e.g., Rent Control) | Shortage | Some consumers | Producers, some consumers | Yes |

Price Floor (e.g., Minimum Wage) | Surplus | Some producers | Consumers, some producers | Yes |

Tax | Reduced quantity traded | Government (tax revenue) | Consumers, producers | Yes |

Key Formulas

Consumer Surplus:

Producer Surplus:

Economic Surplus:

Deadweight Loss:

Additional info: The chapter also discusses real-world applications such as the effects of Uber on consumer surplus, the impact of minimum wage laws, and the debate over price gouging during emergencies. These examples illustrate the practical importance of understanding economic efficiency and the consequences of government intervention in markets.