Back

BackElasticity in Microeconomics: Price, Income, Cross, and Supply Elasticities

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Elasticity in Microeconomics

Introduction to Elasticity

Elasticity is a fundamental concept in microeconomics that measures the responsiveness of one variable to changes in another. In the context of markets, elasticity helps us understand how quantity demanded or supplied reacts to changes in price, income, or the price of related goods. This chapter focuses on price elasticity of demand, income elasticity of demand, cross elasticity of demand, and elasticity of supply.

Price Elasticity of Demand

Definition and Calculation

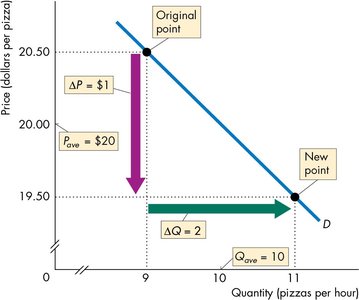

The price elasticity of demand is a units-free measure of the responsiveness of the quantity demanded of a good to a change in its price, holding all other influences constant. It is calculated as:

Formula:

Percentage changes are calculated using the average of the initial and new values for both price and quantity.

Units-Free Measure

Elasticity is a ratio of percentages, making it independent of the units used to measure price or quantity. This ensures comparability across different goods and markets.

Minus Sign and Interpretation

The formula yields a negative value because price and quantity move in opposite directions.

For practical purposes, the absolute value is used to indicate the magnitude of responsiveness.

Types of Price Elasticity of Demand

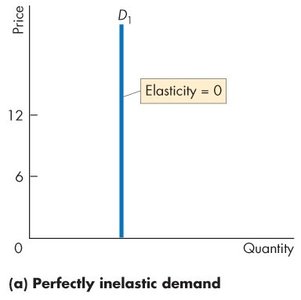

Perfectly Inelastic Demand: Elasticity = 0; quantity demanded does not change as price changes.

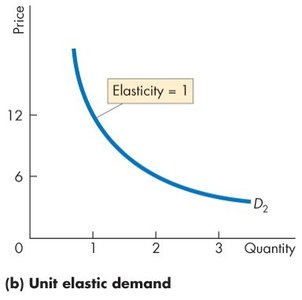

Unit Elastic Demand: Elasticity = 1; percentage change in quantity equals percentage change in price.

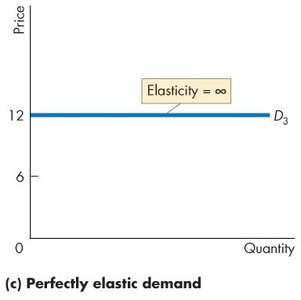

Perfectly Elastic Demand: Elasticity = ∞; any small change in price leads to an infinite change in quantity demanded.

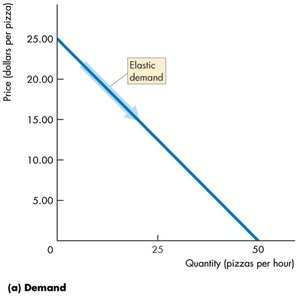

Elastic Demand: Elasticity > 1; quantity demanded changes more than price.

Inelastic Demand: Elasticity < 1; quantity demanded changes less than price.

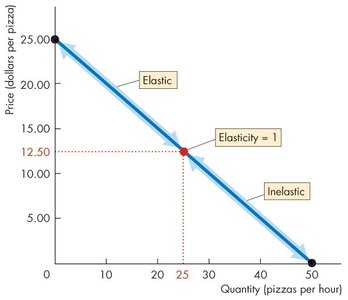

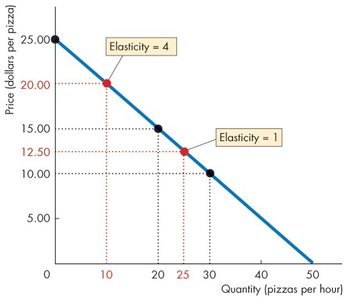

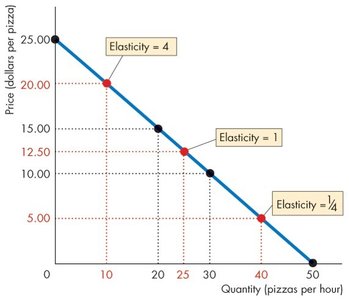

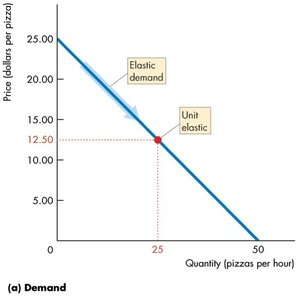

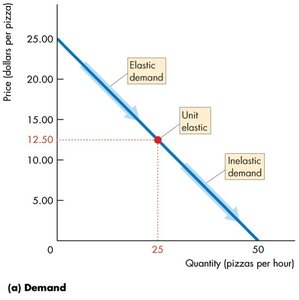

Elasticity Along a Linear Demand Curve

Elasticity varies along a linear demand curve. At the midpoint, demand is unit elastic; above the midpoint, demand is elastic; below the midpoint, demand is inelastic.

Factors Influencing Price Elasticity of Demand

Closeness of Substitutes: The more substitutes available, the more elastic the demand.

Proportion of Income Spent: Goods that take up a larger proportion of income tend to have more elastic demand.

Time Elapsed Since Price Change: Demand becomes more elastic over time as consumers adjust.

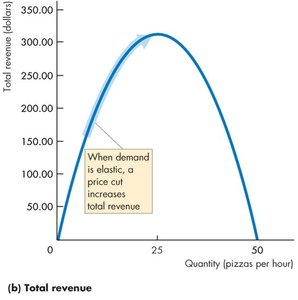

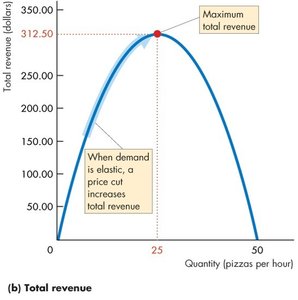

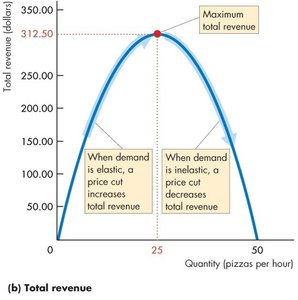

Total Revenue and Elasticity

Relationship Between Total Revenue and Elasticity

Total revenue is calculated as price multiplied by quantity sold. The effect of a price change on total revenue depends on the elasticity of demand:

If demand is elastic, a price cut increases total revenue.

If demand is inelastic, a price cut decreases total revenue.

If demand is unit elastic, a price cut leaves total revenue unchanged.

Total Revenue Test

If a price cut increases total revenue, demand is elastic.

If a price cut decreases total revenue, demand is inelastic.

If a price cut leaves total revenue unchanged, demand is unit elastic.

Income Elasticity of Demand

Definition and Calculation

The income elasticity of demand measures how the quantity demanded of a good responds to a change in income, holding other factors constant. The formula is:

Formula:

Types of Goods Based on Income Elasticity

Normal Goods: Positive income elasticity. If elasticity > 1, demand is income elastic; if 0 < elasticity < 1, demand is income inelastic.

Inferior Goods: Negative income elasticity; demand decreases as income rises.

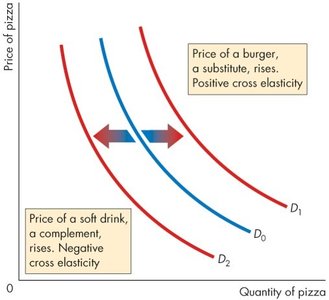

Cross Elasticity of Demand

Definition and Calculation

The cross elasticity of demand measures the responsiveness of demand for a good to a change in the price of a substitute or complement. The formula is:

Formula:

Interpretation

Substitutes: Positive cross elasticity; demand for one good increases as the price of the other rises.

Complements: Negative cross elasticity; demand for one good decreases as the price of the other rises.

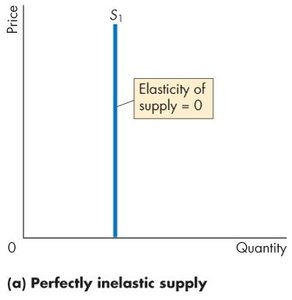

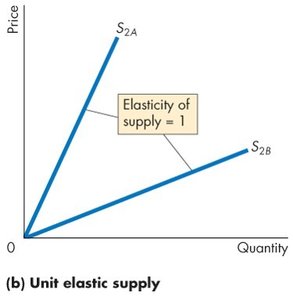

Elasticity of Supply

Definition and Calculation

The elasticity of supply measures the responsiveness of the quantity supplied to a change in the price of a good, holding other factors constant. The formula is:

Formula:

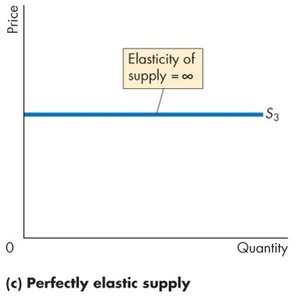

Types of Supply Elasticity

Perfectly Inelastic Supply: Elasticity = 0; quantity supplied does not change as price changes.

Unit Elastic Supply: Elasticity = 1; percentage change in quantity supplied equals percentage change in price.

Perfectly Elastic Supply: Elasticity = ∞; any small change in price leads to an infinite change in quantity supplied.

Factors Influencing Elasticity of Supply

Resource Substitution Possibilities: The easier it is to substitute resources, the greater the elasticity of supply.

Time Frame for Supply Decision: Elasticity increases as more time passes after a price change. Momentary supply is perfectly inelastic, short-run supply is somewhat elastic, and long-run supply is most elastic.

Glossary of Elasticity Measures

Price Elasticities of Demand

Type | Magnitude | Interpretation |

|---|---|---|

Perfectly elastic | Infinity | Smallest price increase causes infinite decrease in quantity demanded |

Elastic | >1 | Quantity demanded changes more than price |

Unit elastic | 1 | Quantity demanded changes equal to price |

Inelastic | <1 | Quantity demanded changes less than price |

Perfectly inelastic | 0 | Quantity demanded does not change |

Income Elasticities of Demand

Type | Value | Interpretation |

|---|---|---|

Income elastic (normal good) | >1 | Quantity demanded increases more than income |

Income inelastic (normal good) | 0<Elasticity<1 | Quantity demanded increases less than income |

Negative (inferior good) | <0 | Quantity demanded decreases as income rises |

Cross Elasticities of Demand

Type | Value | Interpretation |

|---|---|---|

Close substitutes | Large | Small price increase in one good causes large increase in demand for the other |

Substitutes | Positive | Price increase in one good increases demand for the other |

Unrelated goods | Zero | Price change in one good does not affect demand for the other |

Complements | Negative | Price increase in one good decreases demand for the other |

Elasticities of Supply

Type | Magnitude | Interpretation |

|---|---|---|

Perfectly elastic | Infinity | Smallest price increase causes infinite increase in quantity supplied |

Elastic | >1 | Quantity supplied changes more than price |

Unit elastic | 1 | Quantity supplied changes equal to price |

Inelastic | 0<Elasticity<1 | Quantity supplied changes less than price |

Perfectly inelastic | 0 | Quantity supplied does not change |

Conclusion

Understand the concept of elasticity and its importance in microeconomics.

Define and distinguish between different price elasticities.

Apply elasticity of demand to analyze total revenue changes.

Recognize price elasticity of supply and its determinants.

Interpret income elasticity of demand and cross elasticity of demand for different types of goods.