Back

BackFoundations of Microeconomics: Scarcity, Resource Allocation, and Economic Systems

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Foundations of Economics

Introduction to Scarcity and Economic Decision-Making

Economics is the study of how individuals and societies allocate limited resources to satisfy unlimited wants. The fundamental problem of scarcity forces both individuals and societies to make choices about how to use their resources. Every decision involves comparing the costs and benefits of alternative actions, a process that is central to economic reasoning and ensures efficient resource use.

Scarcity: The inability to satisfy all wants due to limited resources.

Economic Choices: Individuals and societies must prioritize and make trade-offs.

Specialization and Exchange: Focusing on specific tasks increases productivity, while exchange allows access to a wider variety of goods and services.

Economic Models: Simplified representations used to analyze and predict economic outcomes.

Example: Choosing between spending time studying or working is an economic decision driven by scarcity of time.

Key Economic Principles and Terms

Allocation: Distributing limited resources among competing uses.

Factors of Production: Land, labor, capital, and entrepreneurship used to produce goods and services.

Trade-off: Choosing one alternative means giving up another due to scarcity.

Opportunity Cost: The value of the next best alternative forgone when a choice is made.

Scarcity and Economic Resources

Definition and Scope of Economics

Scarcity is a universal condition that affects everyone, from individuals to governments. Economics is divided into two main branches:

Microeconomics: Focuses on individual decision-makers, such as households and firms, and their resource allocation.

Macroeconomics: Studies the aggregate outcomes and performance of entire economies, including growth, unemployment, and inflation.

Example: Deciding whether to buy a concert ticket or save money for a new phone illustrates microeconomic decision-making.

What, How, and For Whom in the U.S. Economy

Economists analyze three fundamental questions:

What to produce? (e.g., capital goods vs. consumption goods)

How to produce? (e.g., labor-intensive vs. capital-intensive methods)

For whom to produce? (distribution based on income and factor ownership)

Goods and services are classified as:

Capital Goods: Used to produce other goods and services (e.g., machinery, infrastructure).

Consumption Goods: Purchased for direct satisfaction (e.g., food, clothing, entertainment).

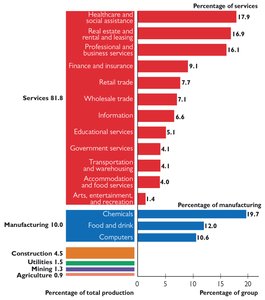

In the U.S., services dominate production, with healthcare, real estate, and professional services being the largest sectors. Manufacturing, construction, and agriculture make up smaller shares.

Changes in Production and the Role of Technology

Over time, the U.S. economy has shifted from manufacturing to services. Technological advancements have replaced some labor with capital, creating new jobs while eliminating others.

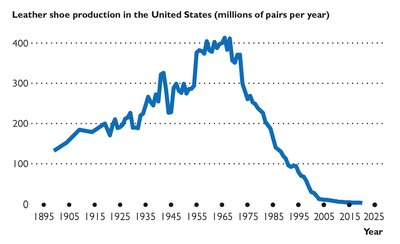

Example: The decline of shoe manufacturing in the U.S. and the rise of retail and service industries.

Factors of Production

Land: Natural resources used in production (renewable and non-renewable).

Labor: Human effort, both physical and mental, used in production. The quality of labor is enhanced by human capital (education, training, experience).

Capital: Man-made resources such as tools, machinery, and buildings. Note: Financial capital (money, stocks, bonds) is not considered a productive resource in economics.

Entrepreneurship: The ability to organize land, labor, and capital, take risks, and innovate.

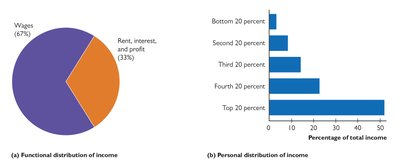

Distribution of Income

Income is earned by selling the services of the factors of production:

Rent: Payment for land

Wages: Payment for labor

Interest: Payment for capital

Profit: Payment for entrepreneurship

The functional distribution of income shows how total income is divided among these factors, while the personal distribution of income shows how income is distributed among households.

Resource Allocation and Economic Systems

Methods of Resource Allocation

Societies must decide how to allocate scarce resources. The main methods are:

Market Price: Resources go to those willing and able to pay. Prices act as signals and incentives.

Command: Allocation by authority or government directive. Common in centrally planned economies.

Mixed Economy: Combines market and command elements. Most modern economies, including the U.S., are mixed.

Example: In the U.S., most goods are allocated by market price, but public goods like education and infrastructure are provided by the government.

Self-Interest vs. Social Interest

Economic decisions are often motivated by self-interest (personal benefit), but economists also consider the social interest (overall societal well-being). Efficiency (maximizing output from resources) and equity (fairness in distribution) are key criteria for evaluating economic outcomes.

Efficiency: Achieved when resources are used to produce the maximum possible output.

Equity: Concerned with the fairness of resource and income distribution.

Practice and Application

Sample Multiple Choice Questions

What is the basic economic problem all societies face? Scarcity

Which of the following is NOT an economic resource? Money

What does the production possibilities curve (PPC) illustrate? The maximum output combinations of two goods given resources and technology

What is opportunity cost? The value of the next best alternative forgone

What is marginal analysis? Comparing additional benefits and additional costs

Key Formulas and Concepts

Opportunity Cost: $Opportunity\ Cost = \frac{Loss\ in\ Good\ Y}{Gain\ in\ Good\ X}$

Net Benefit: $Net\ Benefit = Total\ Benefit - Total\ Cost$

Marginal Analysis: $If\ Marginal\ Benefit > Marginal\ Cost,\ undertake\ the\ action$

Summary Table: Factors of Production and Their Incomes

Factor of Production | Definition | Income Earned |

|---|---|---|

Land | Natural resources used in production | Rent |

Labor | Human effort (physical and mental) | Wages |

Capital | Man-made resources (tools, machinery) | Interest |

Entrepreneurship | Organization and risk-taking | Profit |

Additional info: This guide covers the foundational concepts of microeconomics, including scarcity, opportunity cost, resource allocation, and the structure of economic systems. It is suitable for introductory college-level microeconomics courses and aligns with the first chapters of standard textbooks.