Back

BackInternational Trade and Production Costs: Microeconomics Exam Review

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

International Trade

Key Definitions

Tariffs: A tax imposed by a government on imports of goods into a country.

Imports: Goods and services bought domestically but produced in other countries.

Exports: Goods and services produced domestically but sold in other countries.

Globalization: The process of countries becoming more open to foreign trade and investment.

Protectionism: The use of trade barriers to shield domestic firms from foreign competition.

Growth of International Trade

International trade has expanded significantly over the past 50 years due to:

Decreasing costs of shipping and international travel

Spread of inexpensive and reliable communications

Changes in government policies

Trade constitutes a smaller share of GDP in large economies like the U.S. compared to smaller countries, primarily due to the relative size of their economies.

The U.S. and International Trade

Since 1970, U.S. exports and imports have increased as a fraction of GDP (from less than 6% to over 12% by 2022).

The U.S. is the second largest exporter globally, but trade is less central to its economy than in smaller countries.

Benefits of Eliminating Tariffs

Eliminating tariffs or trade restrictions generally benefits consumers by reducing prices.

Other effects (e.g., on jobs or wages) may benefit firms, not necessarily consumers.

Comparative and Absolute Advantage

Key Definitions

Opportunity Cost: The highest-valued alternative that must be given up to engage in an activity.

Comparative Advantage: The ability to produce a good or service at a lower opportunity cost than competitors.

Absolute Advantage: The ability to produce more of a good or service than competitors using the same amount of resources.

Autarky: A situation in which a country does not trade with other countries.

Specialization and Trade

Countries specialize in goods where they have a comparative advantage.

Both countries can consume more through trade than in autarky.

Exam Review Example

Absolute advantage: Producing more with the same resources.

Comparative advantage: Lower opportunity cost in production.

Terms of Trade

Terms of Trade: The ratio at which a country can trade its exports for imports from other countries.

No country will accept terms worse than its opportunity cost.

Winners and Losers from Trade

Winners: Overall, countries gain from trade (higher standard of living).

Losers: Some firms and workers in import-competing industries may lose and seek protectionist policies.

Government Policies Restricting Trade

Key Definitions

Quotas: Quantity limits on imports, imposed unilaterally.

Voluntary Export Restraints (VERs): Mutually agreed quantity limits between countries.

Tariff: A tax on imported goods.

Free Trade: Trade without government restrictions.

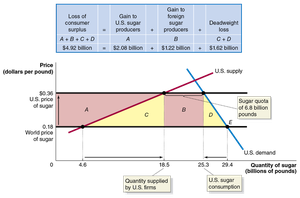

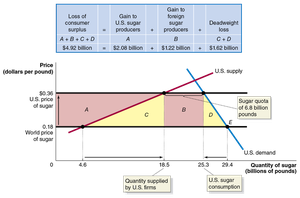

Economic Effects of Quotas

Quotas restrict imports, raise domestic prices, and increase producer surplus for domestic firms.

Consumer surplus falls, and deadweight loss occurs due to inefficiency.

Unilateral Elimination of Tariffs and Quotas

Economists argue that removing trade barriers benefits the economy, even if other countries do not reciprocate.

Exam Review Questions

Main purpose of tariffs and quotas: Reduce foreign competition for domestic firms.

Tariffs make domestic consumers worse off by raising prices.

Quotas benefit domestic producers but harm consumers.

The Debate over Trade Policies and Globalization

Arguments for and Against Free Trade

Free trade generally increases national welfare, but some oppose it due to concerns about job losses, wage reductions, and cultural changes.

Protectionism is often justified by arguments about saving jobs, protecting infant industries, and national security.

Dumping

Dumping: Selling a product below its cost of production, often targeted by trade policy.

It is difficult to determine true dumping due to varying production costs and pricing strategies.

Technology, Production, and Costs

Technology in Economics

Technology: The processes a firm uses to turn inputs into outputs.

Technological Change: Improvements that allow more output from the same inputs.

Short Run vs. Long Run

Short Run: At least one input is fixed; firms have both fixed and variable costs.

Long Run: All inputs can be varied; all costs are variable.

Types of Costs

Variable Costs (VC): Change with output.

Fixed Costs (FC): Remain constant as output changes.

Total Cost (TC):

Average Total Cost (ATC):

Average Fixed Cost (AFC):

Average Variable Cost (AVC):

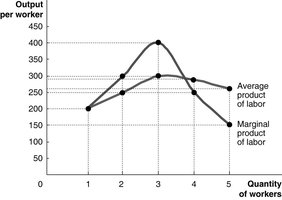

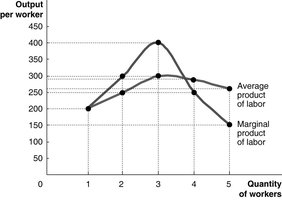

Production Function

Production Function: Relationship between inputs and maximum output.

Shows how output changes as more inputs (e.g., labor) are added.

Marginal Product of Labor and Law of Diminishing Returns

Marginal Product of Labor (MPL): Additional output from hiring one more worker.

Law of Diminishing Returns: Adding more of a variable input to a fixed input eventually causes the marginal product to decline.

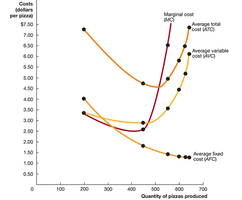

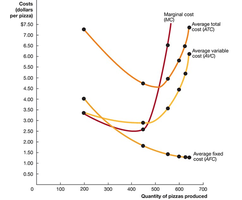

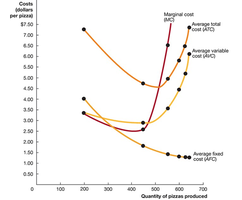

Short-Run Cost Curves

Marginal Cost (MC): The change in total cost from producing one more unit:

MC curve is typically U-shaped due to the law of diminishing returns.

ATC and AVC curves are also U-shaped; AFC declines as output increases.

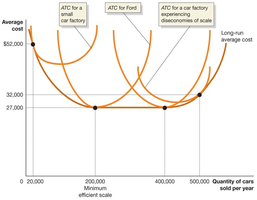

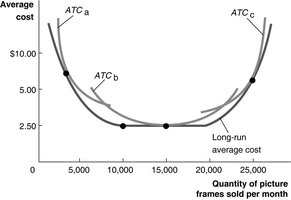

Long-Run Costs and Economies of Scale

Long-Run Average Cost Curve (LRAC): Shows the lowest cost at which a firm can produce any given output when all inputs are variable.

Economies of Scale: LRAC falls as output increases (downward sloping).

Constant Returns to Scale: LRAC remains unchanged as output increases (flat).

Diseconomies of Scale: LRAC rises as output increases (upward sloping).

Concept | Definition | Formula |

|---|---|---|

Total Cost (TC) | Sum of all costs (fixed + variable) | |

Average Total Cost (ATC) | Total cost per unit of output | |

Average Fixed Cost (AFC) | Fixed cost per unit of output | |

Average Variable Cost (AVC) | Variable cost per unit of output | |

Marginal Cost (MC) | Change in total cost from producing one more unit |

Example: If a firm produces 30 units at a total cost of ATC = AFC + AVCATC = 900/30 = 30$).

Additional info: These notes cover core concepts from Chapters 9 and 11 of a typical microeconomics course, focusing on international trade, comparative advantage, protectionism, and the theory of production and costs.