Back

BackMicroeconomics Short Answer Guidance: Profit Calculations and Market Equilibrium

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Q1. Sweet Treats Bakery operates in a perfectly competitive market. Last year, the bakery earned $60,000 in total revenue. The following costs were incurred:

$20,000 for ingredients and supplies

$10,000 for wages

$5,000 for rent

$2,000 for utilities

$1,000 for advertising

The owner quit a job that paid $8,000 per year

The owner took $100,000 out of a savings account that was earning $4,000 in interest per year to invest in the bakery

Background

Topic: Profit Calculations in Microeconomics

This question tests your understanding of accounting profit, normal profit, and economic profit, as well as the distinction between explicit and implicit costs.

Key Terms and Formulas

Explicit Costs: Direct, out-of-pocket payments for resources (e.g., wages, rent, supplies).

Implicit Costs: Opportunity costs of using resources owned by the firm (e.g., foregone salary, foregone interest).

Accounting Profit:

Normal Profit:

Economic Profit:

Step-by-Step Guidance

List all explicit costs and add them together to find the total explicit costs.

List all implicit costs and add them together to find the total implicit costs.

Calculate accounting profit by subtracting explicit costs from total revenue.

Identify normal profit as the total implicit costs.

Set up the formula for economic profit by subtracting normal profit from accounting profit.

Try solving on your own before revealing the answer!

Q2. What signal does the economic profit provide to businesses outside the industry?

Background

Topic: Market Entry and Economic Profit

This question tests your understanding of how economic profit acts as a signal in perfectly competitive markets.

Key Terms

Economic Profit: Profit above normal profit, indicating that resources are earning more than their opportunity cost.

Market Entry: The process by which new firms enter an industry in response to profit opportunities.

Step-by-Step Guidance

Recall that positive economic profit means firms are earning more than their opportunity cost.

Think about how this profit attracts new firms to the industry.

Consider the effect of new entry on market supply and price.

Try answering before revealing the explanation!

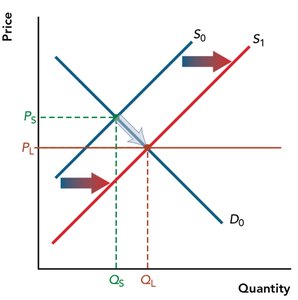

Q3. Suppose that other bakeries in the industry are earning similar profits to Sweet Treats Bakery. Draw a graph that shows both the short-run and long-run equilibrium for the industry.

Background

Topic: Short-Run and Long-Run Equilibrium in Perfect Competition

This question tests your ability to illustrate and interpret market equilibrium changes as firms enter or exit the industry.

Key Terms

Short-Run Equilibrium: Where firms may earn economic profit or loss.

Long-Run Equilibrium: Where firms earn zero economic profit (normal profit).

Supply Curve Shift: Entry of new firms increases supply, shifting the supply curve right.

Step-by-Step Guidance

Draw the initial supply () and demand () curves, showing the short-run equilibrium price () and quantity ().

Show the entry of new firms by shifting the supply curve right to (), resulting in a new long-run equilibrium price () and quantity ().

Label the axes, curves, and equilibrium points clearly.

Try sketching the graph before checking the answer!

Q4. Describe in words how the market moves from short-run to long-run equilibrium.

Background

Topic: Market Adjustment Process in Perfect Competition

This question tests your understanding of how entry and exit of firms drive the market toward long-run equilibrium.

Key Terms

Short-Run Economic Profit: Temporary profit that attracts new firms.

Supply Curve Shift: Entry increases supply, lowering price.

Long-Run Equilibrium: Zero economic profit, no incentive for entry or exit.

Step-by-Step Guidance

Explain that economic profit in the short run attracts new firms to the industry.

Describe how increased supply shifts the supply curve right, reducing market price.

Discuss how the process continues until economic profit is eliminated and firms earn only normal profit.

Try writing your own explanation before checking the answer!