Back

BackMicroeconomics Study Guide: Costs, Supply, Surplus, and Externalities

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Firms and Production

Production Functions and Inputs

In microeconomics, firms transform inputs into outputs using technology. The production function describes this relationship mathematically.

Production Function: , where q is output, L is labor, and K is capital.

Isoquant Curve: A set of input bundles that produce the same output.

Isoquant Map: Collection of isoquant curves for different output levels.

Short Run: Some inputs (e.g., labor) are adjustable, others (e.g., capital) are fixed.

Long Run: All inputs are adjustable.

Example: A factory may adjust labor daily but can only change machinery over years.

Costs

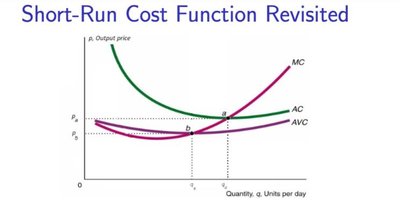

Short-Run Cost Functions

Short-run costs are divided into fixed and variable components. The cost functions help firms decide how much to produce.

Fixed Cost (FC): Costs that do not change with output (e.g., rent).

Variable Cost (VC): Costs that change with output (e.g., wages).

Total Cost (TC):

Marginal Cost (MC):

Average Cost (AC):

Average Variable Cost (AVC):

Average Fixed Cost (AFC):

Typical Properties: AC and AVC are U-shaped. MC intersects AC and AVC at their minimum points.

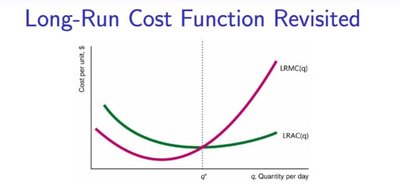

Long-Run Cost Functions

In the long run, all inputs are variable. The long-run average cost (LRAC) and long-run marginal cost (LRMC) are key concepts.

Long-Run Cost Function:

Long-Run Average Cost:

Long-Run Marginal Cost:

LRAC is U-shaped: Decreases due to economies of scale, then increases due to diseconomies.

Relationship:

When :

When :

When :

Supply Curves

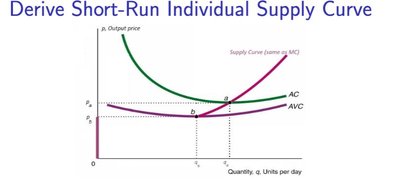

Short-Run Individual Supply Curve

The short-run supply curve is the portion of the MC curve above AVC. Producers supply output where price is greater than or equal to AVC.

Shut-down Price (): If , supply is zero.

Break-even Price (): If , producer earns zero profit.

Supply Decision: If , produce where .

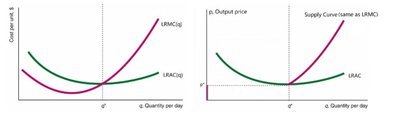

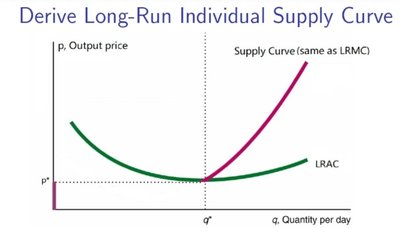

Long-Run Individual Supply Curve

The long-run supply curve is the portion of the LRMC curve above LRAC. In the long run, producers can enter or exit freely.

Long-Run Shut-down Price (): If , supply is zero.

Break-even Price: is both shut-down and break-even price in the long run.

Supply Decision: If , produce where .

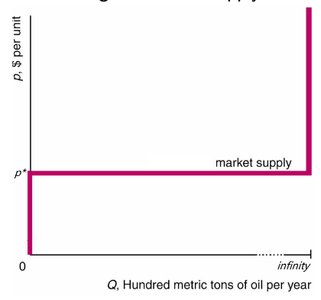

Market Supply Curve

The market supply curve aggregates individual supply curves. In the long run, the supply curve is horizontal at the break-even price if there are infinitely many identical producers.

Short Run: Sum individual supply curves for given producers.

Long Run: Entry and exit lead to a horizontal supply curve at .

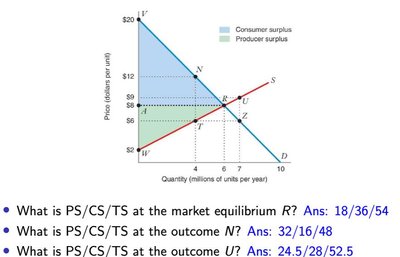

Economic Surplus

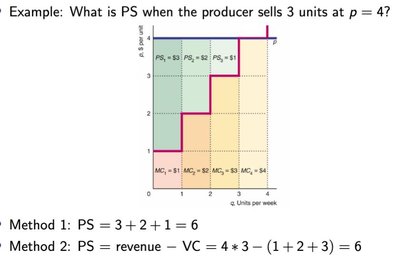

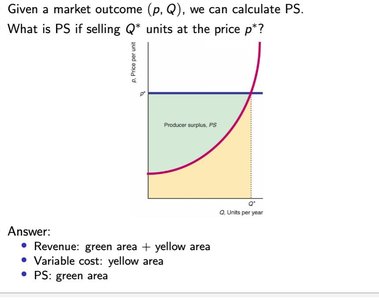

Producer Surplus (PS)

Producer surplus is the gain from trade for producers, calculated as revenue minus variable cost.

PS Calculation: Two methods:

Sum marginal gains unit by unit.

PS = Revenue - VC

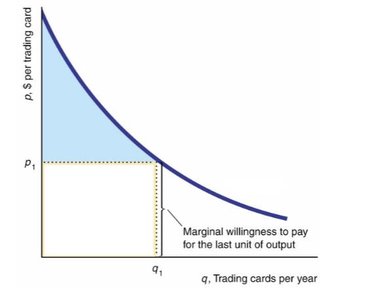

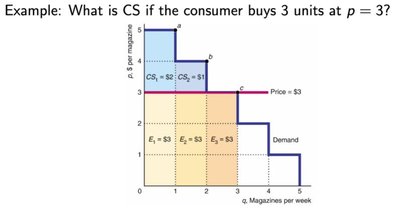

Consumer Surplus (CS)

Consumer surplus is the gain from trade for consumers, calculated as willingness to pay minus expenditure.

Marginal Willingness to Pay (MWTP): The demand curve represents MWTP.

CS Calculation: Two methods:

Sum marginal gains unit by unit.

CS = WTP - Expenditure

Total Surplus (TS)

Total surplus is the sum of producer and consumer surplus, representing social welfare.

TS Formula:

Market Equilibrium: Maximizes total surplus when MWTP = MC.

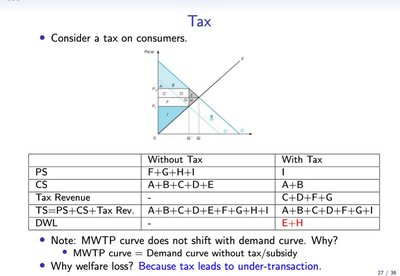

Market Interventions

Tax

A tax reduces the quantity traded, leading to deadweight loss and lower total surplus.

Tax Revenue: Collected by government.

Deadweight Loss (DWL): Lost surplus due to under-transaction.

Without Tax | With Tax | |

|---|---|---|

PS | F+G+H+I | I |

CS | A+B+C+D+E | A+B |

Tax Revenue | - | C+D+F+G |

TS | PS+CS+Tax Rev | PS+CS+Tax Rev |

DWL | - | E+H |

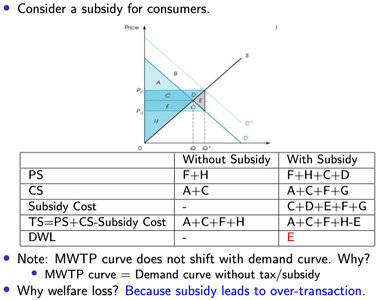

Subsidy

A subsidy increases the quantity traded, leading to deadweight loss from over-transaction.

Subsidy Cost: Paid by government.

Deadweight Loss (DWL): Lost surplus due to over-transaction.

Without Subsidy | With Subsidy | |

|---|---|---|

PS | F+H | F+H+C+D |

CS | A+C | A+C+F+G |

Subsidy Cost | - | C+D+F+G |

TS | PS+CS-Subsidy Cost | PS+CS-Subsidy Cost |

DWL | - | E |

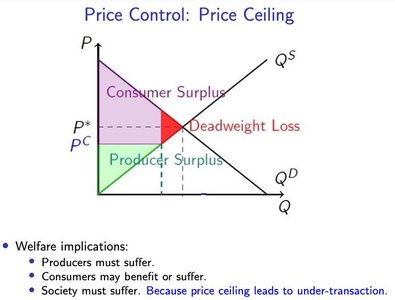

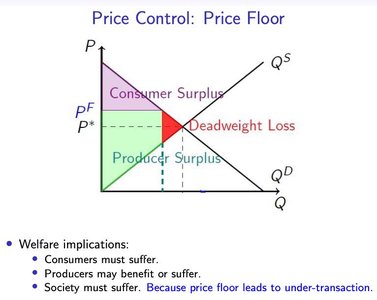

Price Controls

Price ceilings and floors cause deadweight loss by restricting market transactions.

Price Ceiling: Maximum price allowed; leads to under-transaction.

Price Floor: Minimum price allowed; also leads to under-transaction.

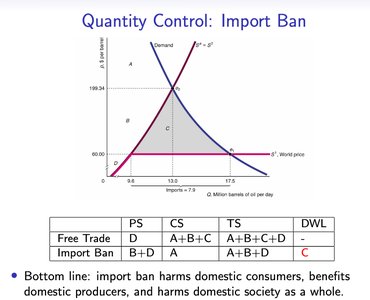

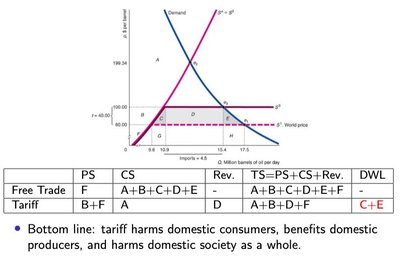

Import Ban and Tariff

Import bans and tariffs restrict trade, harming consumers and society overall, but benefiting domestic producers.

Free Trade | Import Ban | |

|---|---|---|

PS | D | B+D |

CS | A+B+C | A |

TS | A+B+C+D | A+B+D |

DWL | - | C |

Free Trade | Tariff | |

|---|---|---|

PS | F | B+F |

CS | A+B+C+D+E | A |

Rev. | - | D |

TS | A+B+C+D+E+F | A+B+D+F |

DWL | - | C+E |

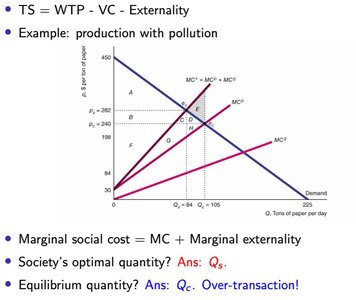

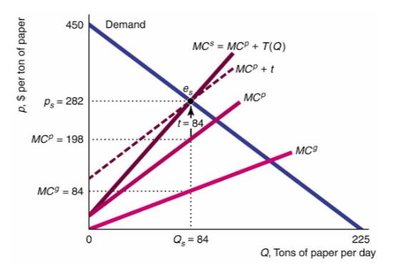

Externalities

Negative Externalities

Negative externalities occur when a producer or consumer's actions harm others. The market equilibrium typically results in over-transaction compared to the social optimum.

Marginal Social Cost: Marginal externality

Remedies: Property rights (market approach), taxes, or quantity controls (regulation approach).

Positive Externalities

Positive externalities occur when actions benefit others. The market equilibrium results in under-transaction compared to the social optimum.

Marginal Social Benefit: Marginal externality

Remedies: Property rights (market approach), subsidies, government provision, or mandates (regulation approach).

Summary Table: Key Formulas

Average Product of Labor:

Profit:

Short-Run Total Cost:

Long-Run Average Cost:

Producer Surplus:

Consumer Surplus:

Total Surplus:

Additional info: All diagrams and tables included are directly relevant to the explanation of the adjacent paragraphs, visually reinforcing key microeconomic concepts.