Back

BackMicroeconomics: The Invisible Hand, Market Equilibrium, and Surplus

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Market Equilibrium and Social Surplus

Market Equilibrium

Market equilibrium occurs where the quantity supplied equals the quantity demanded, resulting in a stable market price and quantity. At this point, the market 'clears,' meaning there are no shortages or surpluses.

Equilibrium Price (Peq): The price at which supply equals demand.

Equilibrium Quantity (Qeq): The quantity bought and sold at the equilibrium price.

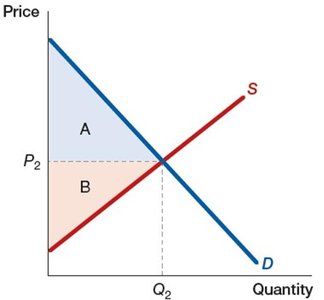

Social Surplus

Social surplus is the sum of consumer surplus and producer surplus. It measures the total net benefit to society from the production and consumption of goods and services.

Consumer Surplus: The difference between what consumers are willing to pay and what they actually pay.

Producer Surplus: The difference between the price producers receive and the minimum they are willing to accept.

Social surplus is maximized at market equilibrium.

The Invisible Hand

The invisible hand is a concept introduced by Adam Smith, describing how self-interested individuals, acting without external guidance, are led to maximize the total well-being of society. In competitive markets, this process results in efficient allocation of resources and maximization of social surplus.

At equilibrium, P = MR = MC for each firm.

Resources are allocated efficiently both within and across industries.

The Invisible Hand in Industry and Across Industries

Within an Industry

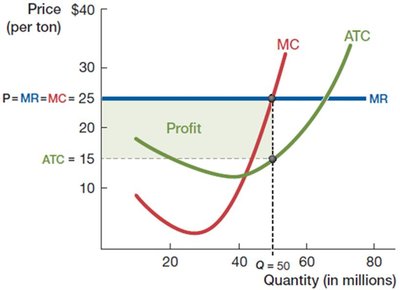

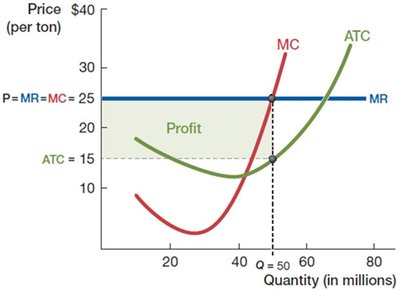

Firms in a perfectly competitive industry produce where price equals marginal cost (P = MC). Some firms may earn zero profit, while others may earn positive profit due to differences in cost structures.

If a firm earns zero profit, it is still covering all its costs, including opportunity costs.

If another firm earns positive profit, resources may shift toward that firm or similar firms.

Across Industries: Long-Run Market Dynamics

In the long run, the invisible hand reallocates resources across industries based on profitability:

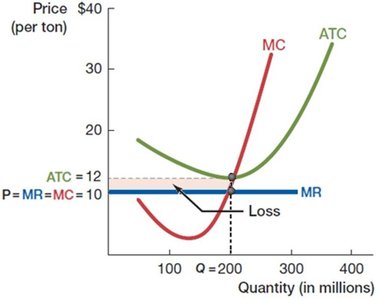

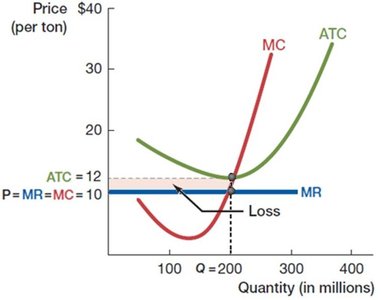

Negative profit leads to firms exiting the market, reducing supply and increasing price until losses are eliminated (P = min ATC).

Positive profit attracts new firms, increasing supply and reducing price until profits are eliminated (P = min ATC).

This process ensures resources flow to industries most valued by society.

Equilibrium Pricing and Resource Allocation

The invisible hand uses prices to efficiently allocate:

Goods between buyers and sellers

Resources within an industry

Resources across industries

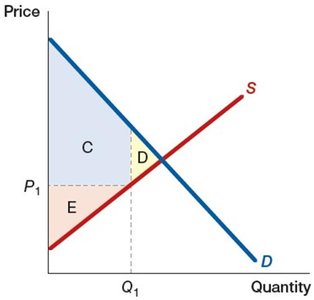

Deadweight Loss and Market Intervention

Deadweight Loss

Deadweight loss is the reduction in social surplus that results from market interventions such as price controls, taxes, or subsidies. It represents the value of trades that do not occur due to these interventions.

Government-Controlled Prices

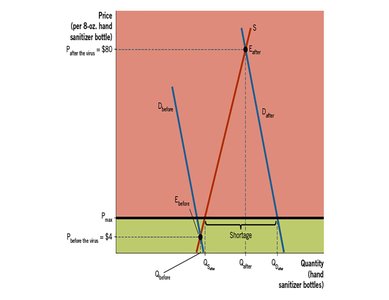

When the government sets a price ceiling (e.g., rent control), the market may not reach equilibrium, resulting in shortages and deadweight loss. The areas representing consumer surplus, producer surplus, and deadweight loss can be identified on a supply and demand graph.

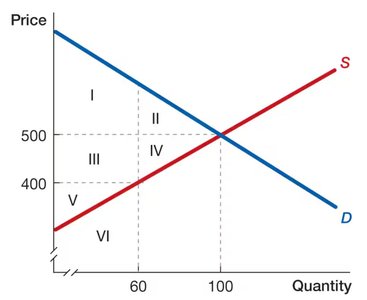

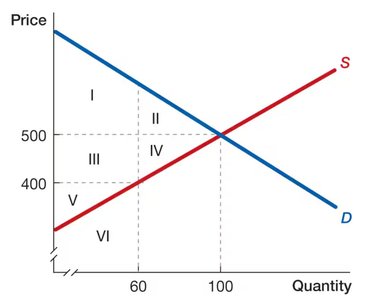

Example: Surging Demand and Price Controls

When demand for a good (e.g., hand sanitizer during a virus outbreak) suddenly increases, the equilibrium price rises. If the government imposes a price ceiling below the new equilibrium, a shortage results.

New equilibrium price is much higher than the old price.

Price ceiling creates excess demand (shortage).

Review: The Buyers' Problem (Chapter 5)

Key Questions for Buyers

How much do you like the product? (Utility from consumption)

What are the prices of goods and services?

How much money do you have to spend? (Budget constraint)

Budget Constraints and Indifference Curves

Budget constraint: The set of all possible bundles of goods a consumer can afford.

Indifference curve: A curve showing all combinations of goods that provide the same utility to the consumer.

Buyers' Equilibrium Condition

Marginal utility per dollar spent is equal across all goods:

All of the budget is used up.

If the price of one good increases, consumers will substitute away from that good toward others, rebalancing their consumption to restore equilibrium.

Review: The Sellers' Problem (Chapter 6)

Key Questions for Sellers

How to make products? (Production function, total and marginal product, variable and fixed inputs)

How much does it cost to make products? (Short-run and long-run costs)

At what price to sell? (Profit maximization condition)

Cost Structures

Short-run cost: (Total Cost = Fixed Cost + Variable Cost)

Long-run cost: All inputs are variable, so only.

Profit Maximization

Firms maximize profit by producing the quantity where marginal cost equals marginal revenue:

Perfect Competition

Many buyers and sellers; goods are identical.

Firms are price-takers:

Free entry and exit in the long run.

Long-run equilibrium:

Positive profit attracts entry (drives price down); negative profit causes exit (drives price up).

Additional info: The notes above synthesize and expand on the provided recitation content, integrating textbook-level explanations and relevant diagrams to reinforce key microeconomic concepts.