Back

BackMonopolistic Competition: The Competitive Model in a More Realistic Setting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Monopolistic Competition: The Competitive Model in a More Realistic Setting

Overview of Monopolistic Competition

Monopolistic competition is a market structure characterized by many firms selling similar but not identical products, with low barriers to entry. This chapter explores how firms in such markets determine prices and output, maximize profits, and differentiate their products, as well as how their performance compares to perfectly competitive firms.

13.1 Demand and Marginal Revenue for a Firm in a Monopolistically Competitive Market

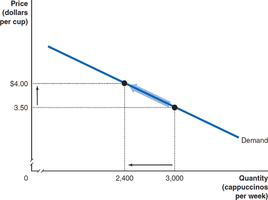

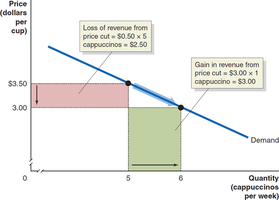

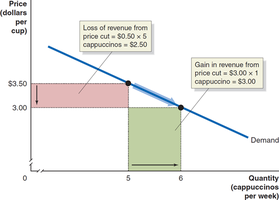

Downward-Sloping Demand and Marginal Revenue Curves

Firms in monopolistically competitive markets face downward-sloping demand curves because their products are differentiated. This means that if a firm raises its price, some customers will switch to competitors, but not all. The marginal revenue curve lies below the demand curve, reflecting the fact that to sell additional units, the firm must lower the price on all units sold.

Monopolistic Competition: Many firms, differentiated products, low barriers to entry.

Product Differentiation: Each firm’s product is unique in some way, leading to brand loyalty.

Marginal Revenue: The additional revenue from selling one more unit is less than the price due to the price reduction on all units.

Example: Blue Bottle Coffee is perceived as unique by some customers, so its demand curve is downward-sloping.

Output Effect vs. Price Effect

When a firm lowers its price, it gains revenue from selling more units (output effect) but loses revenue on units that could have been sold at a higher price (price effect). Marginal revenue is the net result of these two effects.

Output Effect: Increase in revenue from selling additional units.

Price Effect: Decrease in revenue from lowering the price on all units sold.

Marginal Revenue Formula:

Key Point: For downward-sloping demand, MR < Price.

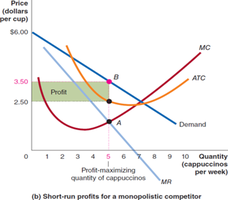

13.2 How a Monopolistically Competitive Firm Maximizes Profit in the Short Run

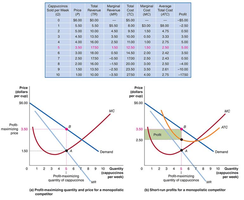

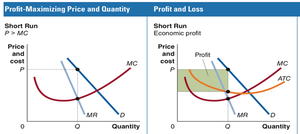

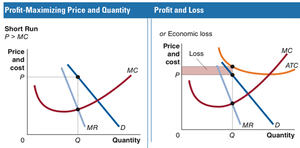

Profit Maximization Rule

Monopolistically competitive firms maximize profit by producing the quantity where marginal revenue equals marginal cost (). The price is then determined by the demand curve at that quantity, and average total cost (ATC) determines whether the firm earns a profit or loss.

Profit Maximization: Produce up to the point where .

Short-Run Outcomes: Firms may earn profits or losses depending on the relationship between price and ATC.

Graphical Analysis: The profit-maximizing quantity is where and intersect; price is found on the demand curve, and ATC is found on the ATC curve.

Profit Calculation: Profit per unit = Price - ATC; Total profit = (Price - ATC) × Quantity.

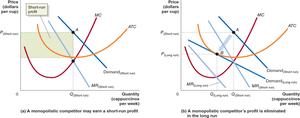

13.3 What Happens to Profits in the Long Run?

Entry and Zero Economic Profit

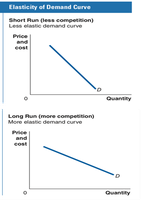

Economic profits in the short run attract new entrants, increasing competition and reducing demand for existing firms. In the long run, firms break even as demand becomes more elastic and the ATC curve is tangent to the demand curve at the profit-maximizing quantity.

Short Run: Firms may earn economic profits or losses.

Long Run: Entry of new firms reduces demand, leading to zero economic profit.

Elasticity: Demand becomes more elastic in the long run as consumers have more choices.

Graphical Analysis: ATC curve is tangent to the demand curve; no profit is possible.

Is Zero Economic Profit Inevitable?

Firms can avoid zero economic profit in the long run by innovating to lower costs or by differentiating their products through marketing and brand management. However, unless these efforts are sustained, competition will eventually erode profits.

Innovation: Lowering costs or improving products can sustain profits.

Brand Management: Maintaining product differentiation through marketing and advertising.

Example: Third wave coffeehouses differentiate through quality and sourcing, but these methods can be copied by competitors.

13.4 Comparing Monopolistic Competition and Perfect Competition

Efficiency Comparison

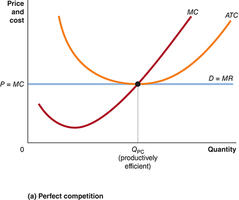

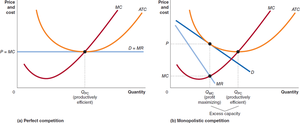

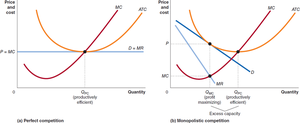

Perfect competition achieves both productive and allocative efficiency, while monopolistic competition does not. Monopolistically competitive firms have excess capacity and do not produce at the lowest possible cost or at the point where marginal benefit equals marginal cost.

Productive Efficiency: Producing at the lowest possible cost ( at minimum).

Allocative Efficiency: Producing where marginal benefit equals marginal cost ().

Monopolistic Competition: Firms produce less than the efficient quantity and at higher average costs.

Excess Capacity: Firms could lower average costs by increasing output.

Consumer Benefits from Monopolistic Competition

Despite inefficiency, consumers may benefit from product differentiation, which allows them to choose products better suited to their preferences, even at higher prices.

Product Differentiation: Offers variety and customization to consumers.

Consumer Choice: Willingness to pay higher prices for products that better match their tastes.

Example: Sweetgreen offers plant-forward meals targeting younger consumers, but faces challenges in achieving profitability.

13.5 How Marketing Differentiates Products

Marketing and Brand Management

Marketing encompasses all activities necessary to sell a product, including advertising and brand management. Effective marketing can increase demand and make it more inelastic, allowing firms to charge higher prices and earn greater profits.

Marketing: Activities to sell and differentiate products.

Brand Management: Actions to maintain product differentiation over time.

Advertising: Increases demand and differentiates products, making demand more inelastic.

Brand Name: Helps maintain differentiation and delay competition.

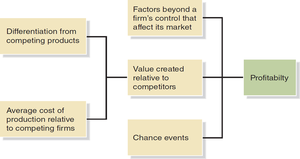

13.6 What Makes a Firm Successful?

Key Factors Determining Success

A firm’s success depends on its ability to differentiate its product and produce at lower costs than competitors, as well as factors beyond its control such as market conditions and chance events. Value creation relative to competitors is central to profitability.

Differentiation: Unique product features or branding.

Cost Advantage: Lower average costs than competitors.

External Factors: Market conditions and chance events.

Value Creation: The combination of differentiation and cost advantage relative to competitors.

First-Mover Advantage

Being the first firm in a market can provide an initial advantage, but long-term success depends on providing good products at low prices and earning customer trust. Later entrants can often surpass first movers by improving on their offerings.

First-Mover Advantage: Initial association with a product, but not always lasting.

Examples: Apple, HP, and Google succeeded despite not being first in their markets.

Key Point: Sustained success requires continuous value creation and customer trust.