Back

BackPrinciples of Microeconomics: Introduction and Fundamental Concepts

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Economic Issues and Concepts

What is Economics?

Economics is the study of how individuals, firms, and governments allocate scarce resources among competing ends. It examines the behavior and interactions of various economic agents to provide for needs and wants, focusing on optimal choices in the face of scarcity.

Scarcity: Resources are limited, but human wants are unlimited. This fundamental problem drives economic activity.

Allocation: Economics analyzes how resources such as labor, land, and capital are distributed to maximize utility, profit, and social welfare.

Key Decision Makers: Households (consumers), firms (producers), and governments (regulators and providers of public goods).

Pressing Economic Issues

Modern economies face several critical challenges, including:

Productivity Growth

Population Aging

Climate Change

Accelerating Technological Change

Rising Protectionism

Growing Income Inequality

Unemployment

Inflation

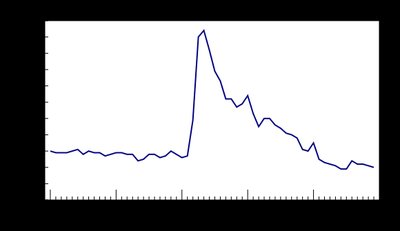

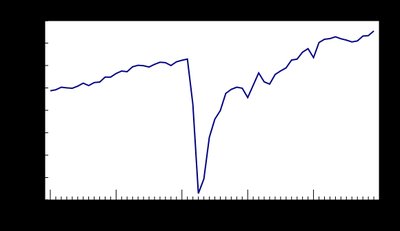

Unemployment and Labour Force Trends

Unemployment and labor force participation are key indicators of economic health. The unemployment rate reflects the proportion of the labor force that is actively seeking work but unable to find employment.

Unemployment Rate: Indicates economic cycles and shocks, such as those caused by the COVID-19 pandemic.

Labour Force: The total number of people employed or actively seeking employment.

The Economic Problem

Resources and Wants

The economic problem arises because resources are scarce and wants are unlimited. Resources include:

Labour: Human capital and physical strength.

Land: Natural resources such as minerals, water, oil, and gas.

Physical Capital: Infrastructure, machines, equipment.

Wants range from basic necessities (food, shelter) to luxury items (cars, entertainment).

Scarcity and Economic Activity

Scarcity necessitates economic activity, which involves making choices about how to use limited resources. Economic systems (money, private property, government) help manage scarcity.

Marginal Analysis and Opportunity Cost

Marginal Cost and Marginal Benefit

Economic decisions are made by comparing marginal costs and marginal benefits:

Marginal Cost: The additional cost incurred from consuming or producing one more unit.

Sunk Cost: Costs that have already been incurred and cannot be recovered.

Marginal Benefit: The additional benefit received from consuming or producing one more unit.

Opportunity Cost

Opportunity cost is the value of the next best alternative forgone when a choice is made. It is a central concept in economics, guiding rational decision-making.

Definition: The opportunity cost of using resources in one activity is the value of those resources in their next best alternative.

Example: The opportunity cost of attending an economics class is the value of what you could have done instead (e.g., working, leisure).

Economic Decision Makers

Households, Firms, and Government

Three main groups make economic decisions:

Households: Consumers aim to maximize utility or satisfaction.

Firms: Businesses acquire factors of production and seek to maximize profits.

Government: Provides infrastructure and public goods, regulates markets.

Economic Models and Rational Choice

Economic Models

Economic models are simplified representations of reality, focusing on essential elements of behavior. They help economists make predictions and analyze outcomes.

Assumptions: Models often assume rational choice, where individuals act in their own self-interest.

Applications: Businesses act to maximize profits; consumers act to maximize happiness and satisfaction.

Additional info:

These notes cover foundational concepts from Chapter 1: Economic Issues and Concepts, including scarcity, opportunity cost, and economic decision makers. The included images directly illustrate labor market trends and unemployment rates, which are central to understanding economic issues and concepts.