Back

BackProducers in the Long Run: Cost, Efficiency, and Technological Change

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Producers in the Long Run

The Long Run: No Fixed Factors

In the long run, all factors of production are variable, allowing firms to adjust all inputs to find the most efficient production method. Unlike the short run, where at least one input is fixed, the long run provides flexibility in choosing among various technically efficient production processes.

Technical efficiency: Achieved when a given set of inputs produces the maximum possible output.

Profit maximization: Requires not only technical efficiency but also cost minimization—choosing the lowest-cost combination of inputs for a given output.

Firms seek the least-cost method of production for each output level.

Profit Maximization and Cost Minimization

Profit-maximizing firms must minimize costs for each output level. If inputs can be substituted for one another, firms will adjust their input mix to reduce costs while maintaining output. This leads to the principle of substitution, where firms use more of the cheaper input and less of the more expensive one as relative prices change.

Cost minimization condition (for two inputs, capital K and labour L):

Where and are the marginal products of labour and capital, and and are their respective prices.

If this equality does not hold, the firm can reduce costs by substituting one input for another.

Principle of substitution: Firms respond to changes in input prices by using relatively more of the cheaper input.

Long-Run Cost Curves

Long-Run Average Cost (LRAC) Curve

The long-run average cost (LRAC) curve shows the lowest possible cost per unit of output when all inputs are variable. It represents the boundary between attainable and unattainable cost levels for a given technology and input prices.

Unlike the short run, there is no distinction between average variable cost (AVC), average fixed cost (AFC), and average total cost (ATC) in the long run.

There is only one LRAC for a given set of input prices.

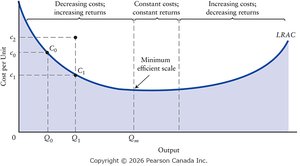

A "Saucer-Shaped" Long-Run Average Cost Curve

The LRAC curve typically has a "saucer" shape, reflecting economies and diseconomies of scale as output changes.

Economies of scale: LRAC falls as output increases (increasing returns to scale).

Minimum efficient scale (MES): The smallest output at which LRAC reaches its minimum; all economies of scale are realized at this point.

Constant returns to scale: Output increases in proportion to inputs; LRAC is flat.

Diseconomies of scale: LRAC rises as output increases (decreasing returns to scale).

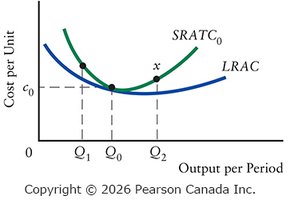

The Relationship Between LRAC and SRATC Curves

The short-run average total cost (SRATC) curve shows the lowest cost of producing any output when one or more factors are fixed. The LRAC curve is the envelope of all possible SRATC curves, representing the lowest attainable cost for each output level when all inputs are variable.

No SRATC curve can fall below the LRAC curve.

Each SRATC curve is tangent to the LRAC curve at the output level where the quantity of the fixed factor is optimal.

Lessons from History: The Lower Envelope Curve

Jacob Viner's historical contribution clarified that the LRAC curve is the lower envelope of all SRATC curves, not simply the connection of their minimum points. This means the LRAC is tangent to each SRATC at the optimal output for that plant size.

The Very Long Run: Changes in Technology

Technological Change and Productivity

In the very long run, technological change can shift the LRAC curve, allowing firms to produce at lower costs or with new products. Technological change is considered endogenous to the economic system, driven by firms' pursuit of profit through invention and innovation.

Technological change: Any change in available production techniques.

Productivity: Output produced per unit of input (e.g., per worker or per hour).

Three aspects of technological change:

New techniques

Improved inputs

New products

Firms’ Choices in the Very Long Run

When input prices rise, firms may substitute away from the expensive input or innovate to reduce reliance on it. Invention and innovation are uncertain but can yield large profits, incentivizing firms to invest in new technologies.

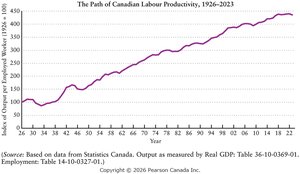

Applying Economic Concepts: The Significance of Productivity Growth

Historical predictions of economic stagnation, such as those by Thomas Malthus, were proven wrong due to slower-than-expected population growth and significant technological advancements that increased output. Productivity growth is a key driver of rising living standards over time.

Thomaslogical progress shifts the LRAC curve downward, enabling more output with the same or fewer resources.

Thomaslogical progress shifts the LRAC curve downward, enabling more output with the same or fewer resources.