Back

BackProducers in the Short Run: Production, Costs, and Profits

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Producers in the Short Run

Production, Costs, and Profits

This section explores how firms produce goods and services in the short run, the types of costs they incur, and how profits are calculated. Understanding these concepts is essential for analyzing firm behavior and market outcomes in microeconomics.

Production Inputs: Firms use four types of inputs:

Intermediate products (outputs from other firms)

Inputs provided directly by nature

Services of labour

Services of physical capital

Production Function: Shows the maximum output from a combination of inputs. It is expressed as , where Q is output, L is labour, and K is capital.

Production is a flow concept: It measures output per unit of time.

Costs and Profits

Firms face explicit and implicit costs, which affect their profit calculations. Understanding the distinction between accounting and economic profit is crucial for decision-making.

Explicit Costs: Direct purchases of goods/services (e.g., wages, rent, intermediate inputs, interest, depreciation).

Implicit Costs: Opportunity costs for which there is no market transaction (e.g., owner's time, owner's capital).

Accounting Profit:

Economic Profit: Or,

Economic Loss: Negative economic profit.

Table: Accounting vs Economic Profit Example

Item | Amount ($) |

|---|---|

Total Revenues | 2000 |

Total Explicit Costs | 1160 |

Accounting Profit | 840 |

Total Implicit Costs | 265 |

Economic Profit | 575 |

Profit-Maximizing Output

Firms aim to maximize economic profit, defined as the difference between total revenue and total cost:

Profit Formula:

Time Horizons for Decision Making

Firms make decisions based on different time horizons, affecting which inputs can be varied.

Short Run: Some inputs (fixed factors) cannot be changed; others (variable factors) can.

Long Run: All factors of production can be varied, but technology is fixed.

Very Long Run: Both factors of production and technology can be varied.

Production in the Short Run

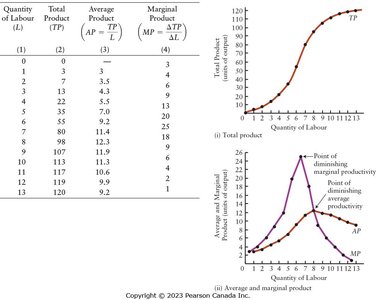

Total, Average, and Marginal Products

In the short run, firms analyze how output changes as they vary the amount of a single input, typically labour.

Total Product (TP): Total output produced in a given period.

Average Product (AP): Output per unit of variable input.

Marginal Product (MP): Additional output from one more unit of input.

Diminishing Marginal Product

The law of diminishing returns states that as more units of a variable factor are added to a fixed factor, the additional output from each new unit eventually decreases.

Each successive unit of the variable factor has less of the fixed factor to work with.

Equal increases in input add less and less to total output.

The Average-Marginal Relationship

The relationship between average and marginal product is fundamental in production analysis.

When MP > AP, AP rises.

When MP < AP, AP falls.

MP intersects AP at AP's maximum point.

Examples of Diminishing Returns

Sport Fishing: More fishers lead to fewer fish per person.

Pollution Control: More filters yield diminishing returns in pollution reduction.

Portfolio Diversification: Adding more stocks reduces risk at a decreasing rate.

Costs in the Short Run

Defining Short-Run Costs

Short-run costs are divided into fixed and variable components, which together determine total and average costs.

Total Cost (TC):

Average Total Cost (ATC):

Marginal Cost (MC):

Marginal costs are always marginal variable costs, as fixed costs do not change with output.

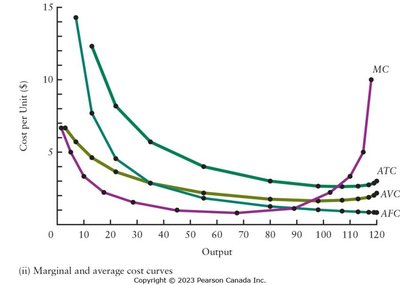

Short-Run Cost Curves

Cost curves illustrate how costs change with output. The MC curve intersects the ATC and AVC curves at their minimum points.

ATC Curve: Derived by vertically adding AFC and AVC curves. It is U-shaped, declining initially, reaching a minimum, then rising.

Why U-Shaped MC and AVC Curves?

The U-shape arises because each additional worker adds the same amount to total cost but a different amount to total output. Diminishing average and marginal product of the variable factor leads to rising AVC and MC.

AVC is at its minimum when AP is at its maximum.

MC is at its minimum when MP is at its maximum.

Capacity

Capacity is the output level at which ATC is minimized. Producing below this level means the firm has excess capacity.

Capacity: Largest output without rising average costs per unit.

Excess Capacity: Output less than minimum ATC.

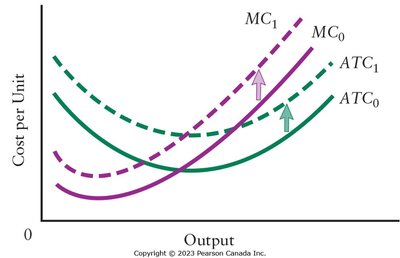

Shifts in Short-Run Cost Curves

Changes in input prices shift cost curves. Variable factor price increases shift ATC and MC upward; fixed factor price increases shift only ATC upward.

ATC and MC shift upward with higher variable factor prices.

ATC shifts upward with higher fixed factor prices; MC unchanged.

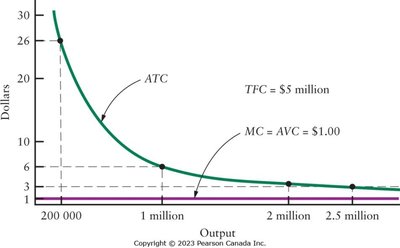

Digital Products and Diminishing Returns

For many digital products, marginal costs are near zero and the law of diminishing returns does not apply. ATC declines as fixed costs are spread over more units.

MC curve is flat at a low value; AVC = MC.

ATC declines with increased output.