Back

BackTrade and the Production Possibilities Curve in Microeconomics

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Trade and the Production Possibilities Curve

Introduction to Trade

Trade is a fundamental concept in microeconomics, allowing individuals and countries to specialize in the production of goods and services in which they have an advantage, and to exchange these for other goods and services. This process increases overall economic welfare and efficiency.

Free trade refers to the absence of government-imposed barriers to the exchange of goods and services across borders.

Trade can benefit all parties involved, but may also create winners and losers within each country.

Key issues include comparative advantage, opportunity cost, and the effects of tariffs.

The Production Possibilities Curve (PPC)

Definition and Interpretation

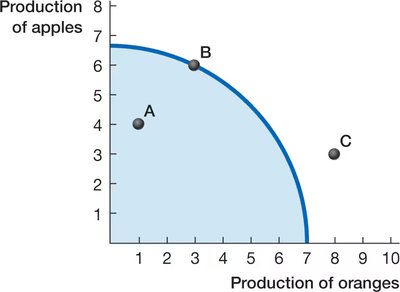

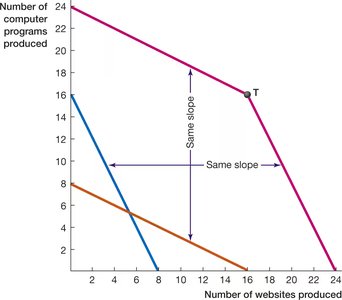

The Production Possibilities Curve (PPC), also known as the Production Possibilities Frontier (PPF), illustrates the maximum feasible combinations of two goods that an economy can produce given its resources and technology.

The PPC is typically downward sloping, reflecting the trade-off between the production of different goods.

The slope of the PPC represents the opportunity cost of one good in terms of the other.

Opportunity Cost

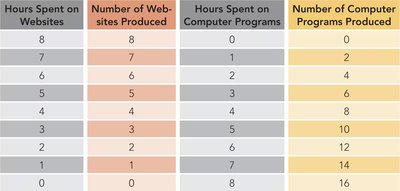

Opportunity cost is the value of the next best alternative foregone when making a choice. On the PPC, it is measured by the amount of one good that must be given up to produce more of the other good.

For example, if moving from producing 2 to 3 websites requires giving up 4 computer programs, the opportunity cost of one website is 4 programs.

Mathematically:

Linear vs. Nonlinear PPC

A linear PPC indicates constant opportunity costs, while a bowed-out (concave) PPC reflects increasing opportunity costs as resources are specialized.

Increasing opportunity cost arises because resources are not equally efficient in all uses.

Comparative and Absolute Advantage

Comparative Advantage

Comparative advantage exists when an individual or country can produce a good at a lower opportunity cost than another. This forms the basis for mutually beneficial trade.

Even if one party is less efficient in producing all goods, trade can still be beneficial if opportunity costs differ.

Specialization according to comparative advantage increases total output.

Absolute Advantage

Absolute advantage occurs when an individual or country can produce more of a good with the same resources than another.

Having an absolute advantage in both goods does not preclude gains from trade; comparative advantage is the key determinant.

Specialization and Gains from Trade

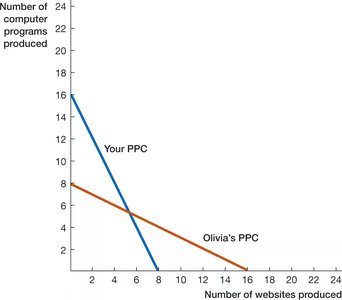

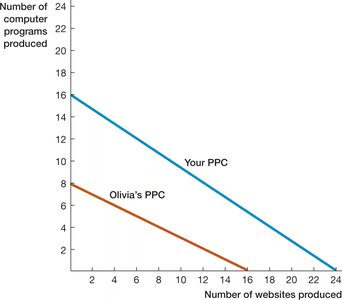

When each party specializes in the good for which they have a comparative advantage and trades, both can achieve consumption bundles outside their individual PPCs.

Example: If Olivia specializes in websites and you specialize in programs, and you trade, both can finish their tasks faster than working alone.

Terms of Trade

Definition and Determination

The terms of trade refer to the rate at which one good is exchanged for another between trading partners. For trade to be mutually beneficial, the terms must fall between the opportunity costs of the two parties.

If your opportunity cost of a website is 2/3 of a program and Olivia's is 1/2, the terms of trade for websites must be between 1/2 and 2/3 programs per website.

Mathematically:

Trade Between Countries

International Trade and the Open Economy

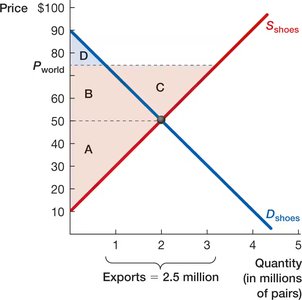

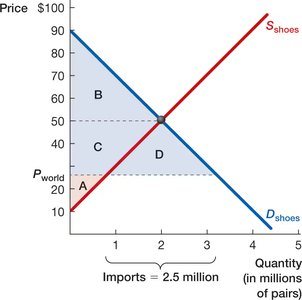

Countries engage in international trade to exploit comparative advantages, leading to increased overall welfare. The world price is the prevailing price of a good on the global market, which small economies take as given.

If the world price is above the domestic price, a country exports the good; if below, it imports.

Winners and Losers from Trade

Exporting raises producer surplus but may reduce consumer surplus.

Importing raises consumer surplus but may reduce producer surplus.

Overall, total welfare increases, but redistribution effects can create opposition to trade.

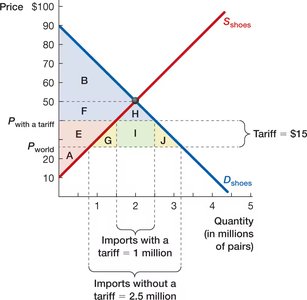

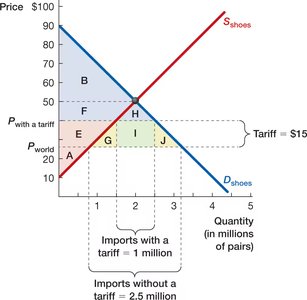

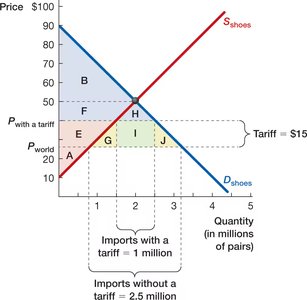

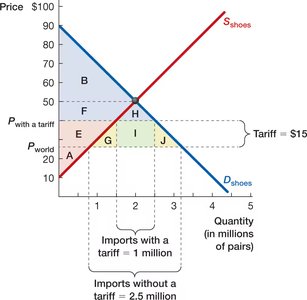

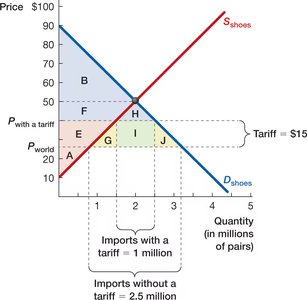

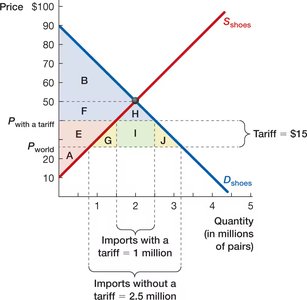

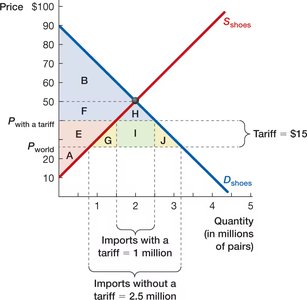

Tariffs and Their Effects

Definition and Purpose

Tariffs are taxes imposed on imported goods, raising their price in the domestic market. Governments may use tariffs to protect domestic industries, raise revenue, or address other concerns.

Tariffs distort market equilibrium, reducing total social surplus.

Economic Effects of Tariffs

Consumer Surplus decreases due to higher prices and reduced consumption.

Producer Surplus increases as domestic producers sell more at higher prices.

Government Revenue increases from tariff collections.

Deadweight Loss arises from inefficient production and reduced consumption, representing lost welfare to society.

Additional Considerations

Tariffs on intermediate goods can further distort production by raising input costs for domestic industries, compounding deadweight loss.

Arguments for tariffs include national security, protecting infant industries, and preserving domestic culture, but these must be weighed against efficiency losses.

Summary Table: Effects of Trade and Tariffs

Policy | Winners | Losers | Total Welfare Effect |

|---|---|---|---|

Free Trade (Exports) | Producers | Consumers | Increases |

Free Trade (Imports) | Consumers | Producers | Increases |

Tariffs | Producers, Government | Consumers | Decreases (Deadweight Loss) |

Key Terms and Formulas

Production Possibilities Curve (PPC): Shows all possible combinations of two goods that can be produced with given resources and technology.

Opportunity Cost:

Comparative Advantage: Lower opportunity cost in producing a good.

Absolute Advantage: Ability to produce more of a good with the same resources.

Terms of Trade: The rate at which goods are exchanged between parties, must fall between their opportunity costs.

Tariff: Tax on imports, raises domestic price to